Brace yourself, the following is not happy reading.

About working horses & people

‘There was a type of employee at the beginning of the industrial revolution whose job and livelihood largely vanished in the early 20th century. This was the horse. The population of working horses actually peaked long after the industrial revolution… there was always a wage at which these horses could have remained employed. But that wage was so low that it did not pay for their feed’, Brynjolfsson & McCaffe

It has become fashionable to blame demographics for a myriad of ills that seem to be inflicting various global economies. In some cases, it is a preferred explanation for declining labour participation rates. In other cases it is the preferred cause for lagging productivity and yet in others, it is blamed for slow pace of wage growth. While, there is no doubt that demographics has a role to play, we maintain that current global structural changes are so deep and profound that ‘industrial age’ understanding of importance of ‘demographics’ is rapidly becoming largely irrelevant.

As discussed in our prior notes, the combination of technological change and overfinancialization are redefining the relationship between labour and capital as well as between labour inputs and the value of ‘social and intellectual capital’. As highlighted by academics and commentators like Paul Romer, Peter Thiel, Jeremy Rifkin, Martin Ford and many others, we are residing in a world where return on labour is declining while returns on ‘superior brain, social capital and connectivity’ are rapidly rising. This is unlike the First and Second Industrial revolutions when labour inputs combined with physical capital played the key role in driving growth and productivity. Whereas in the 19th and 20th centuries, capital was scarce and most activities were highly capital intensive and humans were the key productivity conduits, the current period (21st century) is shaping up as the age when capital is plentiful (indeed excessive) and most new private sector activities are not capital intensive, while technology is increasingly replacing rather than augmenting humans and this is occurring in an increasingly higher value-added cognitive functions. In past notes, we have described it as an ‘age of declining returns on humans and capital’.

While some of our clients believe that the above changes are long-term in nature, we continue to insist that it is no longer the future but is the current reality. Information Age or the Third Industrial revolution can be dated quite precisely. 1971 marked the beginning of computer and processing power (first Intel chip, PC, wireless and public internet networks and first bio-engineering attempts) and financialization (the end of Bretton Woods) revolutions. Initially the pace of change was slow, but by the 1990s it started to impact the most routine (clerical jobs) and by the late 1990s it spread to retail and over the last decade to other services (including financial sector). Robotics, automation, internet of things and AI is already responsible for 80%+ of global trading of financial instruments while rapidly destroying professions (ranging from paralegals to accountants) and starting to dominate the retail and wholesale sectors. The revolution is also now rapidly moving into manufacturing. Robotic factories, 3D printing and a decline in moving parts is starting to impact supply and value chains. Just several examples would suffice. GE is planning to print as many as 100,000 parts of their aircraft engines; Divergent 3D is now able to print a super car in a garage in California whilst Apis Corp has recently 3D printed an entire house for $10,000 and within 24 hours. This is not to mention, robotic (or ‘dark’) factories that are springing up from the US to China. The Fujitsu (2016) survey projects that around 90% of manufacturing companies expect a significant change in their business model within a decade or less.

Although economists argue that as in the First and Second Industrial revolutions, new jobs would be created (and undoubtedly this is true), at least initially the new jobs are not much more than ‘warehousing’ labour pending their final disposal in some form. Also, this time around, degree of disruption is far more profound than in previous cycles. Technology is creating a world of almost no scarcity, unlimited scalability and where value of conventional labour inputs is rapidly eroding. Essentially, AI is replacing IQ while automation and robotics are replacing ‘muscle power’. This places a great deal of value on EQ and ability to think ‘outside of the box’. However, as Maslow as well as Myers Briggs (MB) framework and other studies showed, most people (70%-80%) are what MB calls ‘sensing’ individuals (or in other words, people who tend to follow procedures and respect orders, authority and hierarchy). However these people have limited ability to innovate or think ‘outside the box’. They were ‘salt of the earth’: honest, reliable and hardworking base of the middle class in the First and Second Industrial revolutions but their value is currently rapidly eroding.

In our view, these fundamental technological forces are altering the nature of economies and labour markets. In developed countries, most mechanically repetitive and low value added manual labour has already been automated. Many other professions are likely to follow, as computing power continues to grow at an exponential pace. As highlighted by Frey and Osborne of Oxford University, up to 50% of the US jobs are likely to be automated in the next decade or two, including telemarketers, legal secretaries, tax preparers, real estate brokers, couriers and messengers, accountants and a large chunk of economists, doctors, insurance underwriters etc. Increasingly extinctions are occurring in the higher cognitive functions. Again, while some would argue that it is a far too long timeframe, it should be remembered that a given occupation does not need to go completely extinct for the labour force to start losing considerable economic and pricing power.

Most of the new jobs thus far were created in what we would describe as lower value added but high human touch occupations (such as nursing, waiters or bar attendants), however, even these jobs are likely to go. Just as most people would no longer pay anything extra to have a human at the super market check-out counter, it is unlikely that ultimately there would be much value in ensuring that humans check whether patients have taken their medication at the hospital while increasingly (particularly in Japan) one can already witness restaurants with minimum human involvement or robotic hotel check-ins. AI and robotics are also already revolutionizing health diagnostic industry. On the other hand, as the US Economic Census highlights, innovation in information and robotics tend to create far fewer than conventionally expected new jobs. As at 2016, less than 0.5% of the US employment was in the industries which did not exist prior to 1999/2000.

In other words, in a somewhat callous fashion, the quote above by Brynjolfsson & McCaffe implies that humans today, are the equivalent of extinct working horses of late 19th – early 20th centuries. It is likely that within a decade or two, value would gravitate so strongly towards what Peter Thiel called ‘zero to one’, that only people with strong empathy and EQ (i.e. entertainment, priests, psychiatrists) as well as technocratic and some managerial elite, would continue to play a significant role. This also promises to be the world of even sharper income and wealth inequalities and quite likely a world of extreme political reaction against the trend of declining importance of human inputs, potentially rivalling a modern equivalent of 1789 French revolution.

However, if these issues were not enough, the world also needs to deal with the legacy of past over financialization (in turn largely caused by societal demand for growth, against the background of stagnant productivity). The process of financialization or effectively bringing future consumption to the present commenced in 1971 but significantly accelerated after collapse of Berlin Wall in 1989. As discussed (here), as a result, the global economy has become addicted to an ongoing leveraging and financialization, which simultaneously support consumption while threatening global stability. As Adair Turner perceptibly asked, why over the last three decades did global economies need an ever-increasing level of debt to maintain acceptable levels of growth, which threatens the stability of the global economy? Our answer is that it is a political response to low productivity, which commenced in the US in the mid-tolate 1970s but accelerated on a global basis in 1980s-90s. We estimate that the ‘fire ball’ of financial instruments (holistically defined to include most financial instruments, ranging from debt to bonds, shadow banking to equities), is now anywhere between US$400–800 trillion (or around 5x-10x global GDP) and this ‘cloud of finance’ needs to continue expanding; otherwise it would collapse on itself, causing potentially massive dislocations on the ‘ground’.

We maintain that labour markets and the global economy are currently caught in a pincer movement between rapidly dissolving labour markets and over financialization, which is likely to preclude conventional wage and inflationary signals. Essentially labour markets are currently changing at a much faster pace than the ability of politics, societies or central banks to catch up. We are facing a potentially dramatic abolition of supply and demand analysis for labour, even as the Fed continues to emphasize the outdated labour market slack models. It is almost like the Emperor Nero fiddling as Rome burnt.

Broken demand supply = no wages

We believe that demand for and supply of labour is now irretrievably broken. While we can debate the extent to which demographics and labour market was in the past driving growth and productivity, it seems that now this relationship no longer exists.

As discussed above, advances in artificial intelligence and robotics are powering a new and much stronger than previously experienced wave of automation and replacement of human cognitive skills. While the Trump administration is focused on the impact of trade, it increasingly looks like technology is the key driver of job losses as well as decline in labour bargaining power. The most recent study by Daron Acemoglu and Pascual Restrepo (‘Robots and Jobs: Evidence from the US labour market’) found that proliferation of robotics and artificial intelligence is driving both lower employment as well as declining wage outcomes. Based on mathematical simulation, these academics concluded that AI and robots probably cost around 400,000 US jobs per annum between 1990 and 2007, and an increasing portion was in the middle class and middle income jobs, regardless of their education or skills. The activities that are most susceptible over the next five to ten years are more routine cognitive tasks (such as data collection and processing) and more routine mental and physical activities. According to estimates by Laura Tyson, these represent more than half of the US wages. The latest McKinsey review goes beyond these levels, and estimates that over the next decade or two at least 60% of occupations would be impacted. While outright extinctions would be rare, it is likely that at least 30%-50% of constituent tasks would be automated. Loss of some of the functionality leads to lower wage bargaining power.

It is clear that technology-based changes are skill based. However, unlike the First or Second Industrial revolutions, when technology was complementing humans and was enhancing muscle power, the Third Industrial revolution or Information age is aiming at replacing humans altogether. It is aimed at replacing increasingly sophisticated cognitive functions (ranging from editors and paralegals to accountants and draughtsmen, from traders to analysts). These are professions that usually require college or higher educational attainment. Thus, this time around, it is not just merely about skills, but rather the need for very specific skill-sets. It is no longer about earning a four year college degree or even some degree of computer or IT literacy (though both are useful), but it is about EQ rather than IQ as well as ability to add value to rapidly proliferating machine learning. It is no longer about physical strength (young males) or college training or even IQ. Hence, it is not surprising that older generations can now easily compete with younger cohorts and that increasingly the traditional view of 35y-49y cohort being the most productive is becoming an anachronism of the by-gone industrial era.

We therefore maintain that even at exceptionally low levels of unemployment it is unlikely that economies would deliver any meaningful rise in wages, commensurate with the reported unemployment levels. The Philips curve has been broken for decades. Indeed it was almost twenty years ago that Douglas Staiger, James Stock and Mark Watson conclusively illustrated the difficulty in estimating the inflationary neutral level of employment. Since then the relationship between prices and wages has become even weaker and we suspect as the global economy evolves through the turbulence of the Information Age, the relationship between unemployment levels and prices as well as wages will further weaken. Indeed, as can be seen below, the US and the UK are already experiencing the lowest levels of unemployment since World War II, and nevertheless, there is absolutely no evidence of any significant pick-up in wages. There is also growing evidence of slowing wage growth in a number of emerging markets (such as China).

As technology and over-leveraging (and associated over-capacity) erodes corporate pricing and reduces marginal cost and the price of every product and service to zero, ability to pay higher wages is restrained, as the private sector battles to keep margins. At the same time, significant change in the production and distribution processes that were implemented over the last two decades, make the private sector far leaner and more flexible. Hence, it is unlikely that there will be a need for higher (and more expensive) labour inputs. At the same time, we believe that private sector visibility remains exceptionally constrained, as the public sector continues to expand its remit. As Peter Drucker once presciently remarked, the government is now increasingly in the business of not just ensuring that the climate is conducive to business, but instead it attempts to micro manage weather (i.e. not too cold; not too hot).

Thus, we believe that a combination of rapidly evolving technology, a high degree of operating flexibility and limited demand visibility, implies that even at exceptionally low levels of unemployment, there would be no break-out of wage pressures. We believe that it also implies that the global economy continues to reside in a deeply disinflationary climate.

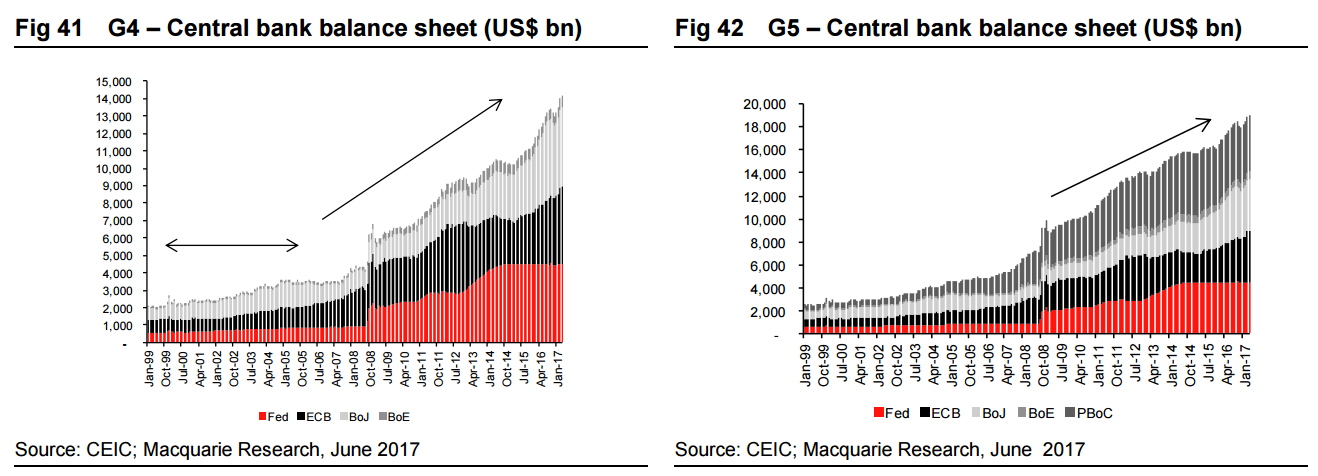

Despite a massive increase in central bank assets, from a run rate of around US$2 trillion to more than US$14 trillion, there is absolutely no evidence that the global economy is in danger of seeing any meaningful acceleration of core inflation and despite tight labour markets in a number of key economies (US, UK, Germany, Japan), there is no evidence of overheating.

This goes to the heart of the debate where interest rates should stabilize and discussion of any normalization of central bank balance sheets. Despite several rounds of tightening, global monetary and financial conditions have become even looser than they were 12 months ago. Whether we look at the St Louis Fed Financial Stress Index or high yield indices or overnight and TED spreads, there is absolutely no evidence of any tightening or stress. It seems that the more the Fed tightens, the more liquidity conditions ease.

It clearly reminds one of Greenspan’s ‘conundrum’ of 2004-05, when tightening by the Fed led to a significant easing in US financial conditions, and in turn a ballooning property bubble that ultimately burst in 2008. Bernanke’s explanation of a ‘savings glut’ in emerging markets was disingenuous, as it was domestic US policies which were largely responsible for excessive savings in Asia, nevertheless, something similar is currently occurring. We believe that it is the same need to continuously inflate financial assets to support wealth and consumption that led to the savings glut a decade ago is still working.

As discussed in our recent reviews (here), we believe that the world’s biggest industry is now manufacturing of capital from capital for the sake of capital. This leads to a consistent (and growing) oversupply of capital (in its various forms) when compared to far more moderate (and generally declining) demand for capital. Hence, our argument is that the cost of capital can never go up, irrespective of what the Fed, ECB or BoJ would like to achieve. Long-term rates react to different forces that short-term and so long as we continue to reside in the world where technology and over financialization continue to drive marginal cost to zero, it is hard to see how the cost of capital would ever rise. The danger however is one of policy errors and underestimation of the extent to which yield curves could flatten and potentially invert, as a result of persistent attempts to raise rates and reduce the size of the balance sheet. Our base case scenario remains that investors will continue to dwell in the world characterized by weak productivity, strong disinflationary pressures, with the need to continue financializing at a rapid clip, preventing any rise in cost of capital. How does one invest in such a dystopian world?

Dystopian Portfolios for dystopian world

‘There is nothing so disastrous as a rational investment policy in an irrational world’, John Maynard Keynes

The above quote from John Maynard Keynes, who apart from being an economist was also an exceptionally savvy investor, encapsulates dilemma facing investors.

Current investment climate (and indeed for more than a decade) is the one of non-existent business and capital market cycles. This implies that any trading and investment strategies based on conventional tools and variables (such as sector rotation, mean-reversion) are bound to fail. In our view this explains consistent investor under-performance. As described (here), the above dystopian business and capital market cycles are further complicated by deadly interactions between modern technology, computer trading, AI and passive fund management. It makes life particularly difficult for macro funds, hence explaining gradual disappearance of ‘human’ macro funds.

We believe that dystopian business and capital markets require equally dystopian and non-mean reversion investment styles. We therefore continue to recommend avoiding conventional mean reversion and rotation strategies. In our view the ‘normal or conventional’ world is not coming back, and this should be reflected in investment thinking. Over the last four-to-five years, we have recommended two complementary strategies – ‘Quality Sustainable Growth’ and ‘Thematics’ (see methodology, here). We particularly like Thematics, as these directly invest into dystopian trends of ‘declining returns on humans and capital’. The only proviso is that we prefer to play Thematics on a global basis, as there are very few themes in either Asia ex Japan or EMs in general. In the EM universe, we prefer to rely on ‘Quality Sustainable Growth’.

I more or less agree except still think that the line about “no more mean reversion” is wrong. This world is one in which risk has been shifted from the financial to the political thus cycles may be lengthened but they are also more prone exogenous disruption. Capital will not be able to so dispense with labour without major, global class-based violence of all kinds.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.