The Australian Coal Seam Gas (CSG)-to-Liquid-Natural-Gas (LNG) industry began auspiciously, with its champions promising export revenue, royalties and jobs.

The three plants at Gladstone were built during one of the great resource booms of the past 100 years. Demand out of Asia for LNG appeared almost limitless at the beginning of this decade.

However, demand by the world’s largest LNG importer, Japan, has been shrinking, and growth in China and other emerging markets has failed to keep up with the boom in supply. Nominal global liquefaction capacity closed 2016 significantly oversupplied—29% above demand, and the gap between supply and demand widened over the year despite very low prices.

Even with growth in some emerging markets, and growth in some developed markets like South Korean and Taiwan, the global LNG market remains significantly over supplied.

This glut in global supply will very likely deepen, until 2020 at least, by which time supply will have increased by 34% to 456 MTPA. Global demand will simply not take up the slack.

IEEFA expects that the expanding glut will put relentless downward pressure on prices and lead to many contract defaults and renegotiations.

It is a truism in the LNG supply industry that the product is expensive to store, so the glut we describe in this paper can only be resolved by LNG processing capacity being curtailed.

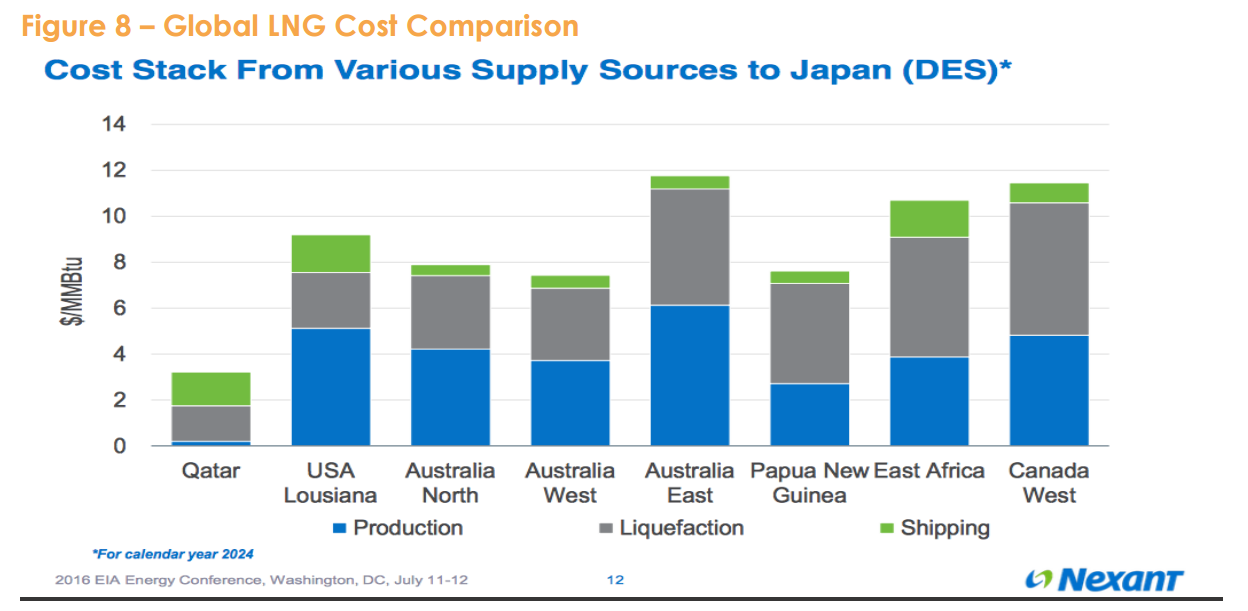

In all resource markets, highest-cost producers have to curtail production first.

The three Gladstone plants sit at the very apex of the global cost curve, so these plants that will feel the pressure to shut in capacity most acutely. IEEFA expects some liquefaction trains at Gladstone to cease production altogether over the next two years.

The LNG industry in Eastern Australia is fundamentally weak because its elements were developed in the wrong order.

Export contracts were secured, plants were approved with no consideration of the domestic market, plants were built and finally gas fields were developed. Along the way, the gas industry failed to contain the cost of building three plants concurrently, a misstep that led to globally uncompetitive capital costs. The industry found that when it went to drill for gas— after having secured gas contracts and built the plants—that the CSG fields that were expected to supply the plaints failed to produce the gas expected.

Capital costs of the plants at Gladstone, and operating costs of the gas fields that supply Gladstone, are globally uncompetitive.

What is particularly worrying for the industry in this case is that the very best CSG fields have been drilled, and costs will rise further from here.

IEEFA estimates that if Santos were to write down the value of its Gladstone investment, GLNG, to global comparatives it would amount to a write off up to $3.3 billion. Origin Energy would face write downs of a similar magnitude on its investment in APLNG.

As a direct result of a massive overbuild of LNG capacity, Australian East Coast domestic gas markets are undersupplied, leading to globally uncompetitive, record high gas prices. We are seeing prices in Australia for both contract and spot gas well in excess of what customers pay in North Asia.

After five decades of least-cost domestic gas supply, industry is showing an inability to now supply gas at even export price parity, putting the government under ever-increasing pressure to intervene and secure remotely affordable energy supplies for both residential and industrial consumers.

The various solutions proposed by the industry—producing more gas at Narrabri, fracking in the Northern Territory, opening an LNG import facility in NSW or even supplying the East Coast with a prohibitively long and expensive pipeline from Western Australia—are all uneconomic. The gas supplied under such proposals would be at a price above the world’s most expensive market, Japan. Producing expensive wellhead gas and then adding expensive pipeline charges is no way to bring down the domestic price of gas.

Accounts of the market published by the oil and gas industry in Australia lack integrity. Oil price forecasts, currency and discount rate assumptions all vary significantly, leading to asset values that are inconsistent. IEEFA estimates that if official forecasts for oil prices from the Office of the Chief Economist were used, the value of GLNG, according to Santos’s latest accounts, could be overstated by in excess of US$1billion.

IEEFA recommends that Australia adopt U.S. standards that require that reserves be calculated using the same oil price. We also recommend adoption of U.S. disclosure rules that mandate reporting by field, of average sales prices for oil and gas produced, and average production costs.

Such consistent and comprehensive disclosure would support the formulation of sensible government policy on energy.

The companies involved in LNG production on the East Coast of Australia will continue to produce at a net loss for as long as their shareholders will allow them—in the hope that some geopolitical event will send LNG prices up. To date, despite massive drops share price and large and continuing write-offs, investors appear to be willing to commit more equity capital.

However, as the glut deepens and balance sheets continue to deteriorate, investor patience will be severely tested. Australian governments would do well now to make a clear and unequivocal choice. Either they continue to back the gas industry (the architects of this problem) at the expense of all Australians, or they can choose—as every other sovereign nation on earth does—to ensure that Australia’s natural resources are used at the very least to provide domestic energy at a reasonable cost.

This report examines where the three East Coast CSG-to-LNG export plants at Gladstone fit into the global landscape for natural gas.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.