Fortescue breaks as Dalian weighs

Dalian is soft today:

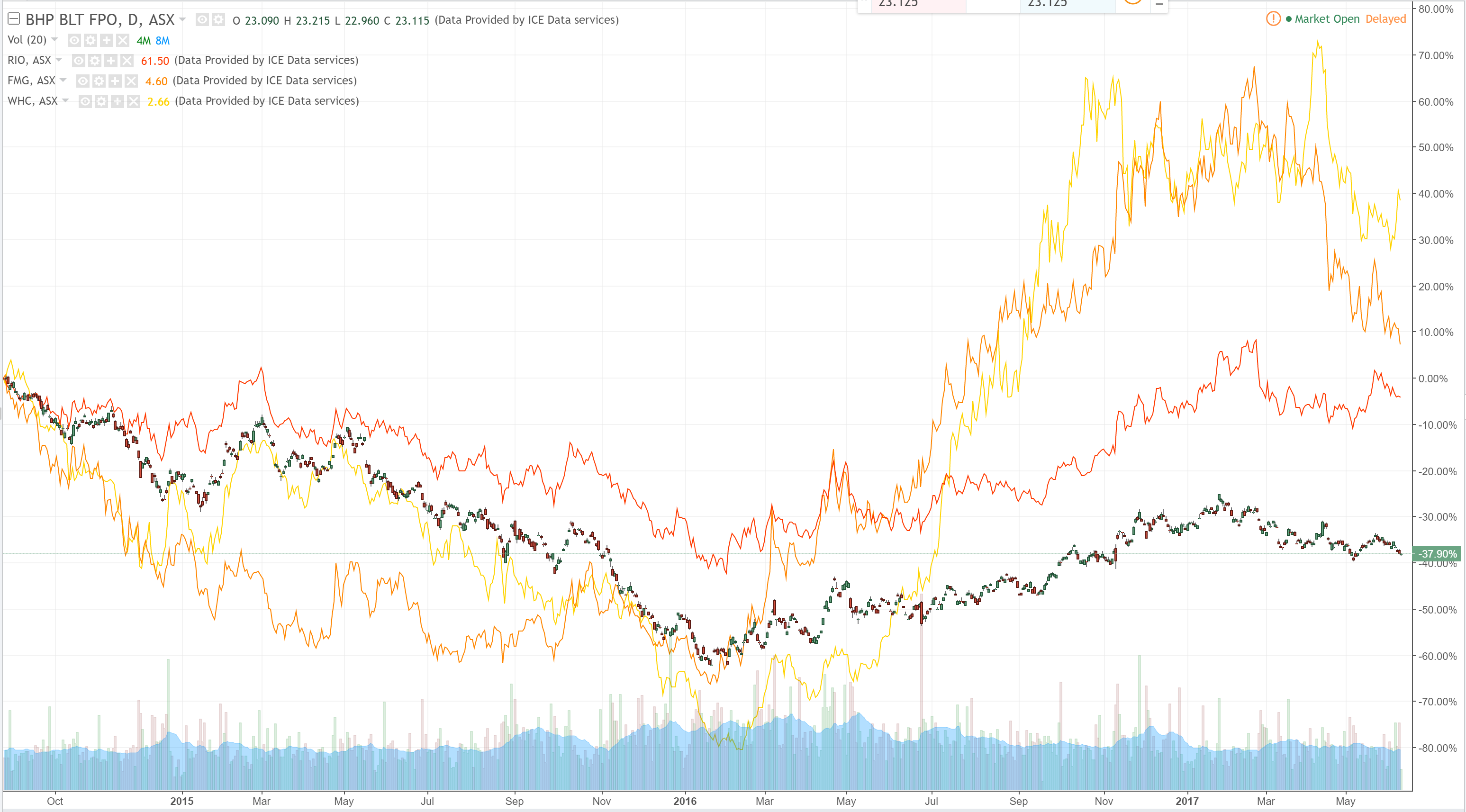

Big Iron is down:

FMG has broken to new lows. Here’s the monthly chart:

How low does it go? All the way in my view. Although it has deleveraged, it is now confronting a potential structural shift in the steel market in which abundant lower quality ore becomes the fulcrum for the nest stage of the shakeout as less is wanted in China to lower pollution and more is available from India. FMG’s 62% break even has already rocketed on its ore discounts to above $45 per tonne so as of today it’s EBITDA outlook is perhaps $1.5bn but shrinking fast. At a market cap of $15bn it’s way too pricey for what’s coming. I see new post-GFC boom lows for 62% before the year is out, let alone for 58%.

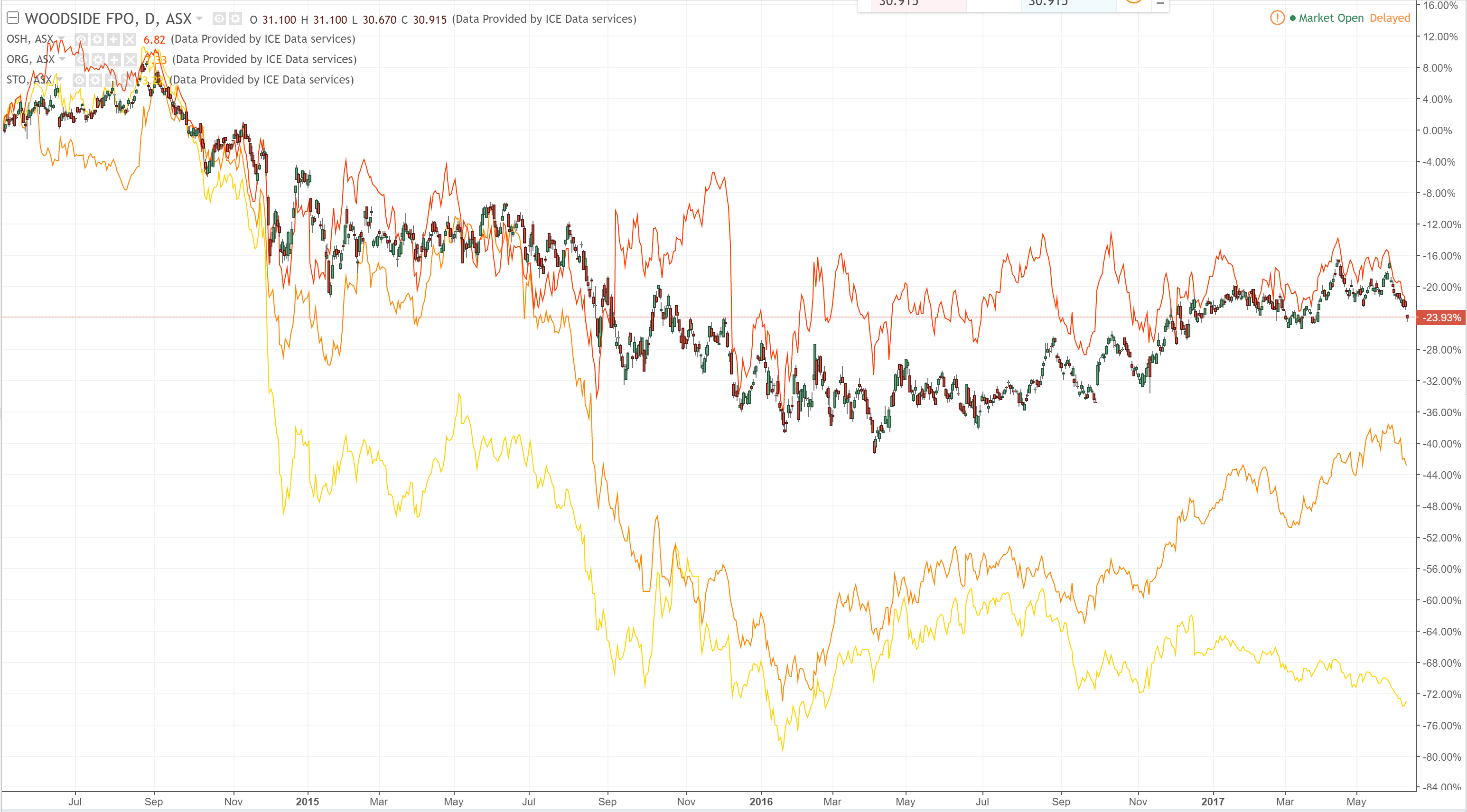

Big Gas is on the nose too though STO is getting some relief:

It will be brief. A vague reservation mechanism is no comfort…

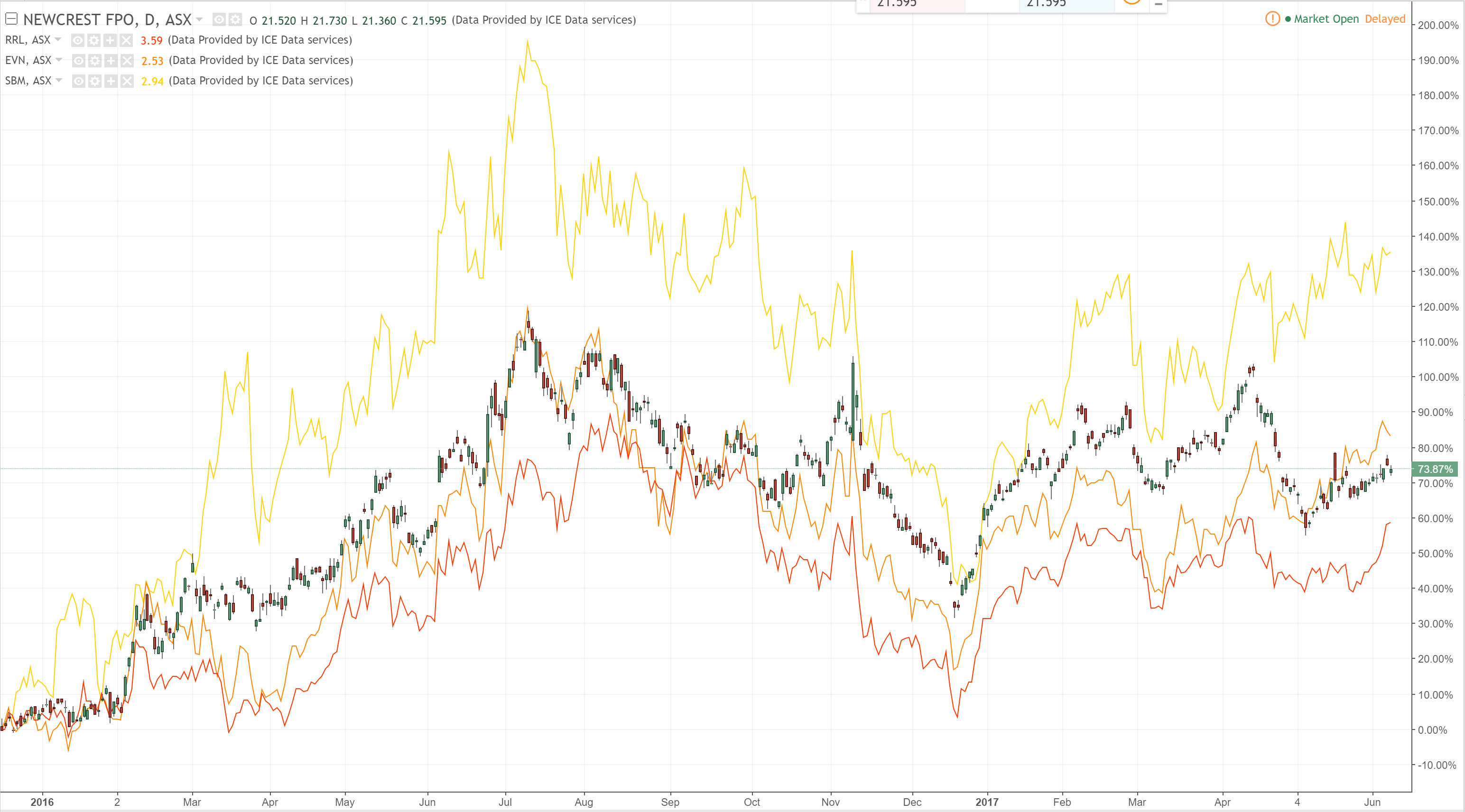

Big Gold is mixed:

Big Debt is trying bottom:

The divi is now pretty tempting grossed up at these levels. However, the next round of discounting may well pivot off iron ore and fading economic prospects.

Big Liar is fading:

MEA down. Once again the market tells McGrathmaggeddon to shut his spruikhole.