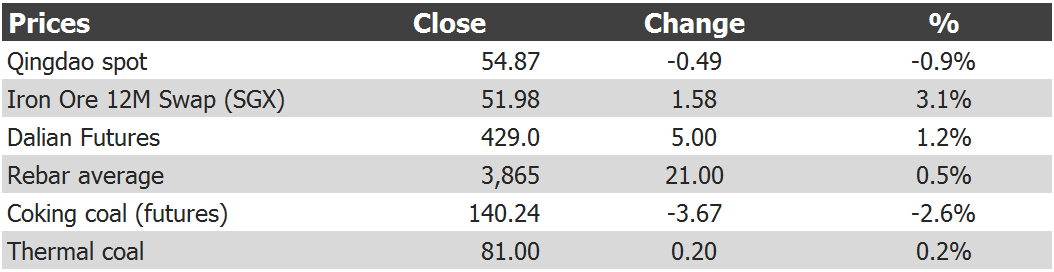

Iron ore price charts for June 12, 2017:

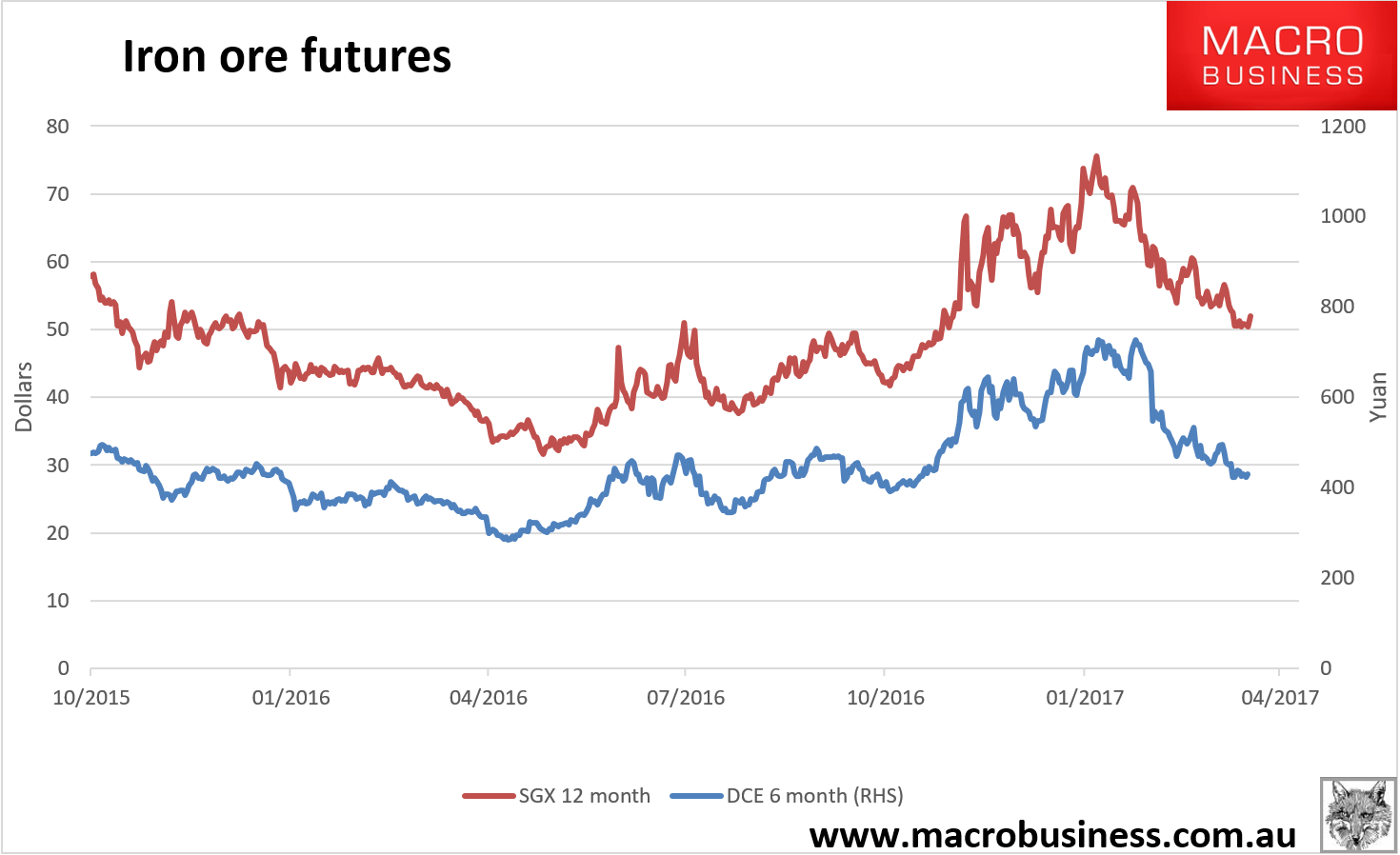

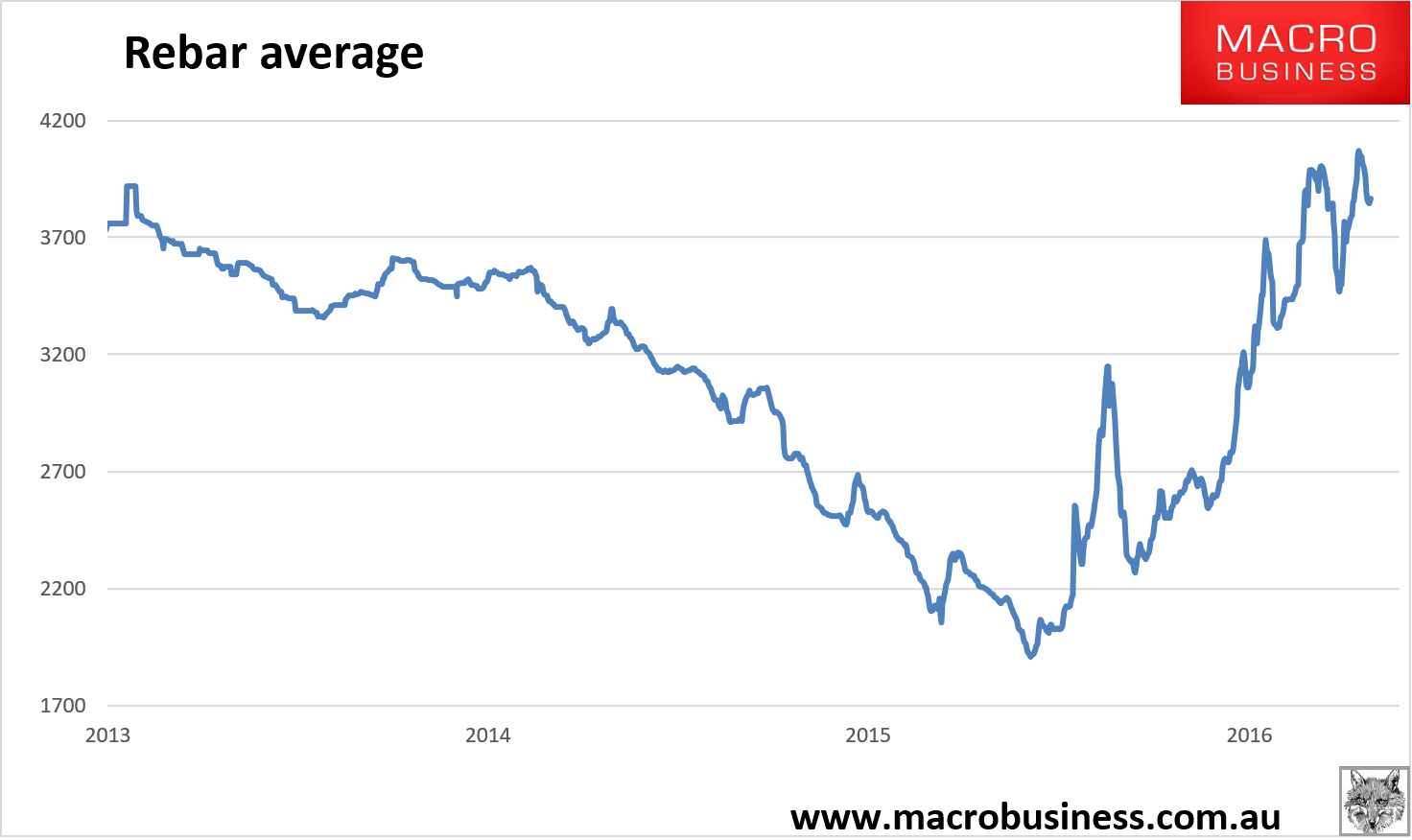

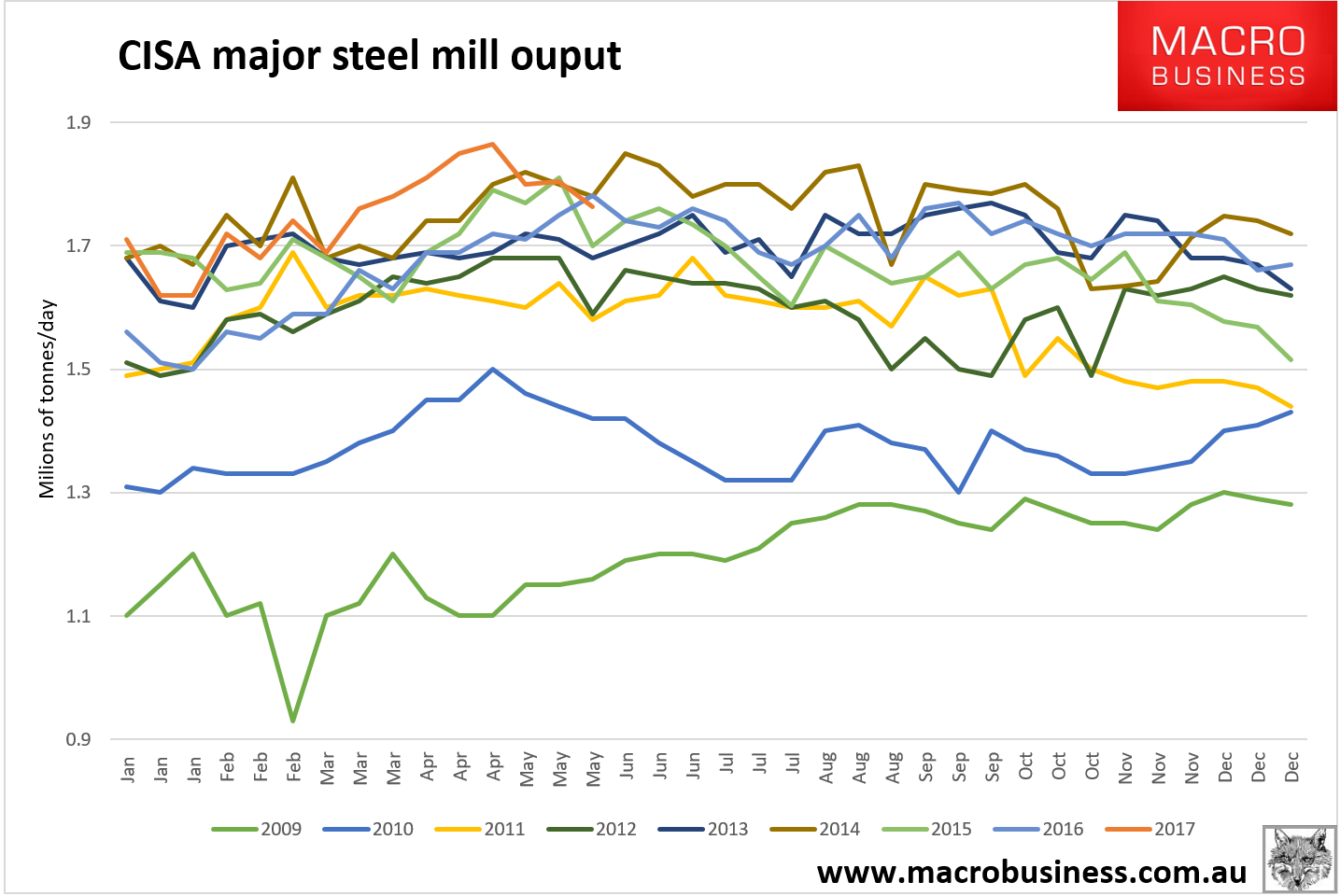

Tianjin benchmark was down 20 cents over the long weekend to $54.40 (down 80 then back up 60). Paper is trying and failing rally. Steel is only correcting slowly. Coking coal remains under pressure. CISA steel output for late May fell -3% to 1.79mt and is back in reasonable ranges.

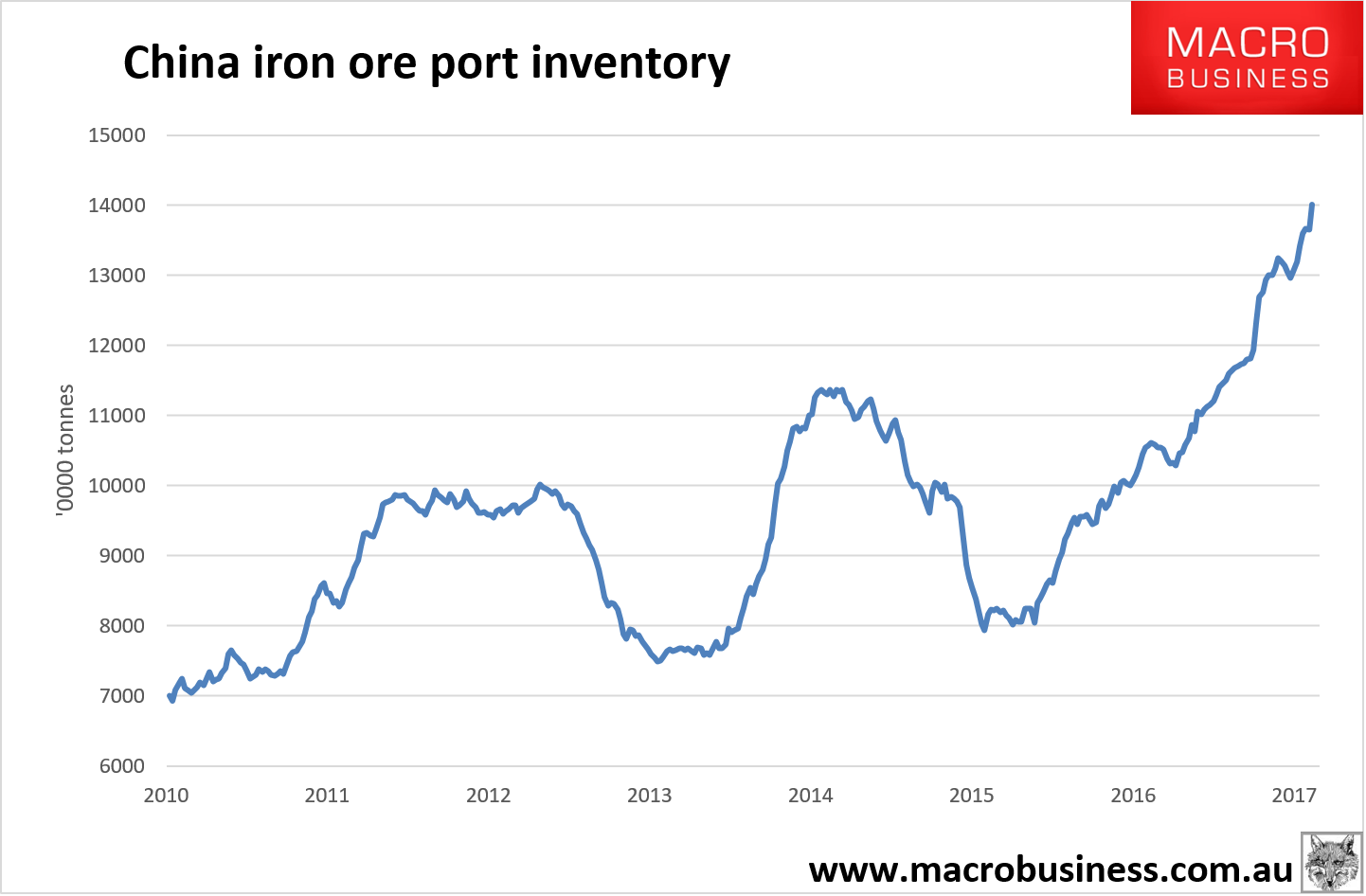

The big one today is port stocks which poured on another 3.6mt last week to 140.1mt and are now mounting towards Everest peaks. Those arguing that this OK because steel output is so high so the “days of use” measure is reasonable are missing the point. Steel output is being inflated by the closure of induction furnaces and the shifting use of scrap into blast furnaces. The main point to take from climbing port stocks is that, for time being at least and maybe permanently, underlying iron ore demand is just not there despite high steel output.