The MacroBusiness moniker, Reynard the Fox, represents why the blog exists. Reynard is an archetype of the “trickster”, the joker or court jester who cuts through the hypocrisy of the day to tell the plain truth. Crucially, it is done from the inside. Reynard is not a rebel or revolutionary, he is a satirist, an inside outsider that describes the world the way it should be to expose the world we have for what it is.

That spirit drives MB. We didn’t set out to turn Australia on its head, or tear down its institutions. We are reformers not revolutionaries. We may not exactly get inside the tent but we certainly turn up at the circus to piss on it from the outside.

Thus, we didn’t set about becoming a chronicle of Australian corruption. We just did our jobs and that’s what’s been exposed by the Reynard ethos. We knew the corruption and degeneracy was there but it’s depth and breadth has astounded. And in truth it has worsened dramatically as the irresistible truth of its own existence has been revealed and thus threatened.

From Parliament House it extends right through state and local bureaucracies. It dominates an over-concentrated business sector which now dedicates huge resources to manipulating policy to preserve economic rents. It extends right through the media, which is now hooked to a life-preserving drip of real estate advertising.

It exists in myriad forms but perhaps most pervasively and deeply as an idea, an identity almost, that Australia is exceptional, that nothing can stop it, and that all of the very obvious imbalances that are destroying it are nothing more than the dark imaginings of disgruntled lunatic fringe.

That idea was captured beautifully yesterday when one of the High Priests of Australian Exceptionalism, the Governor the Reserve Bank of Australia, ostensibly spoke earnestly in defense of workers:

When any of us feel like there is more competition out there you’re less inclined to put your price up. People value security and one way you can get a bit more security is not to demand a wage rise. Firms act like that and workers act like that.

Productivity growth tends to come in waves, and in the optimistic interpretation we’ll see another wave some time not too far down the track.

A second factor is that workers feel like there are more competitors out there, they’re worried about the foreigners and the robots.

Hopefully running for a few years now with quite tight labour markets [will be] re-energising workers to get more of the labour share.

At some point, one imagines that’s going to lead to workers being prepared to ask for larger wage rises.

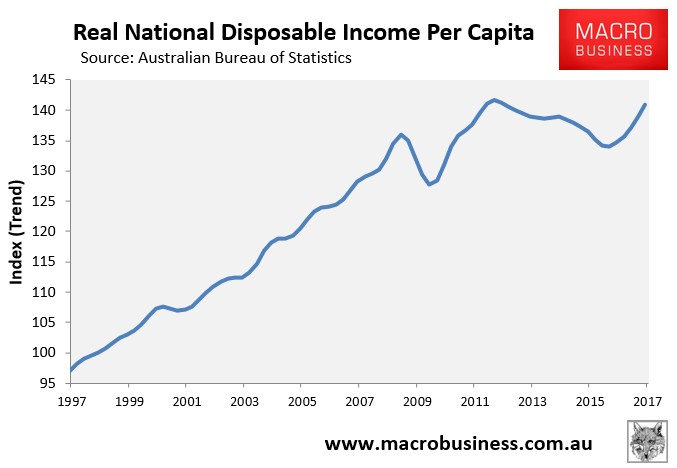

Here is what Phil Lowe is discussing, disappearing living standards. No income gains for six years:

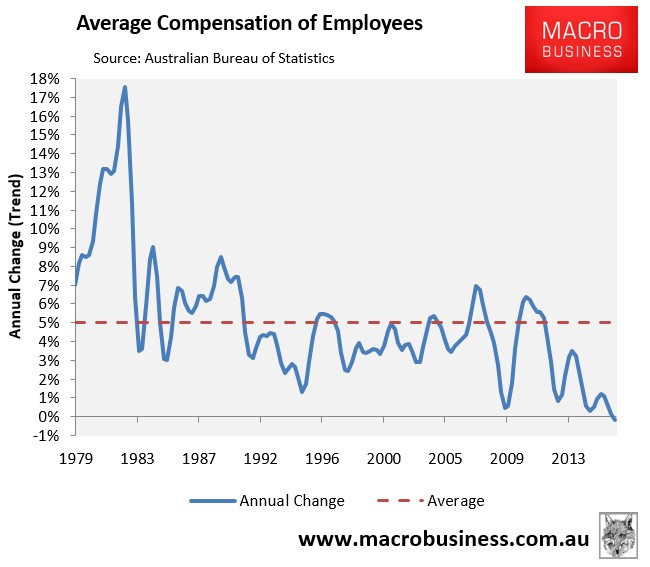

Falling wages for the first time in modern history:

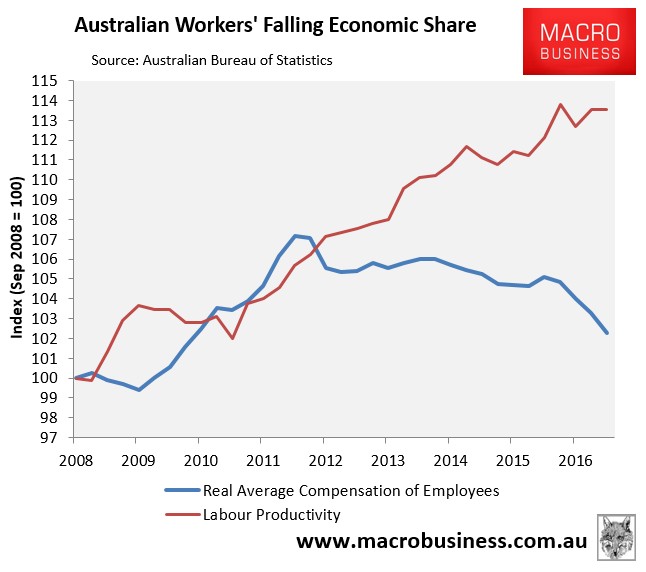

Despite good productivity gains:

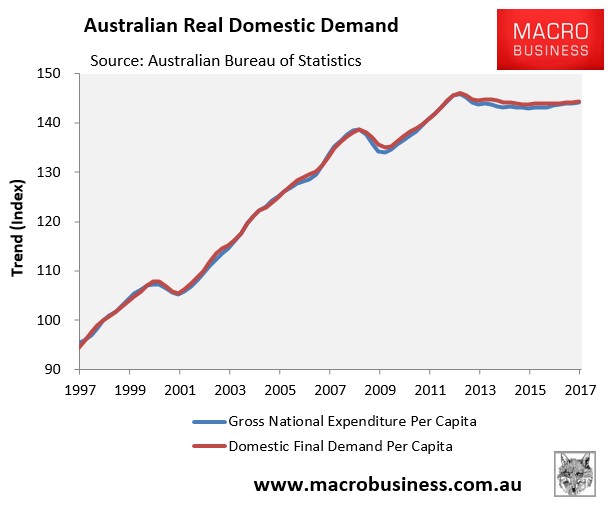

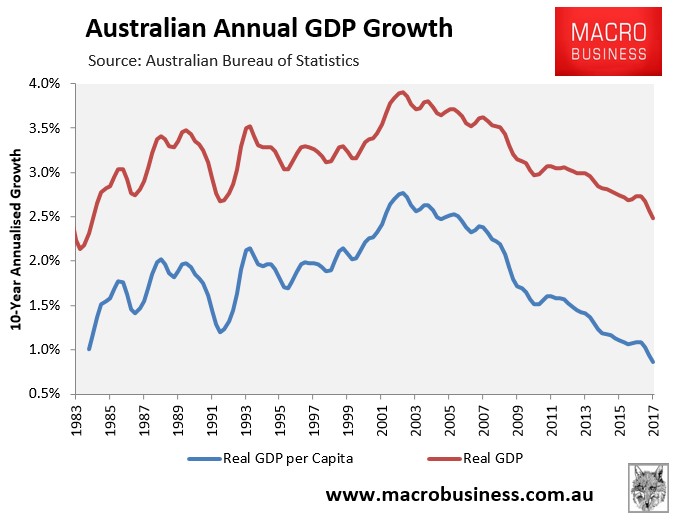

An unprecedented stall in per capita demand:

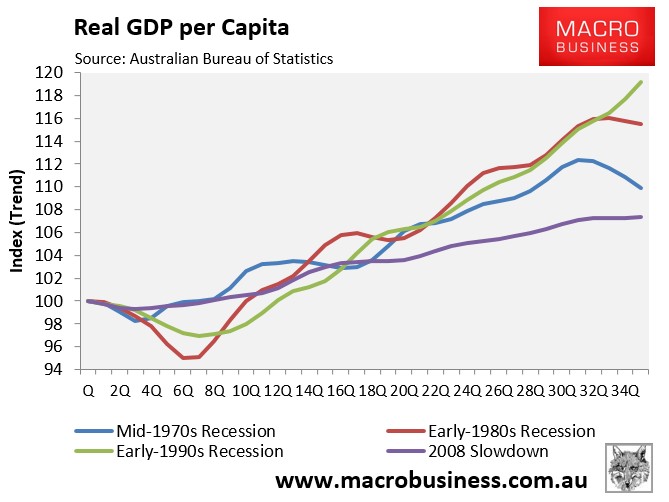

A far worse growth performance than any previous recession:

And output growth per head:

Are these problems the result of workers not having the gumption to front up for pay rises, I ask you?

No, they’re not. The charts above are the result of broken economic structure and policy that is only making it worse and worse. That structure is obvious. It has been described over and again at MB year after year:

- an over-reliance upon commodity export income;

- an over-reliance upon leveraging that wildly volatile income in global markets to feed the housing bubble which supports demand, and

- an over-reliance upon the Federal Budget to guarantee everything when either the income dries up or debt gets more costly.

All of the traditional building blocks of sound economic structure are missing from this model. The entire thing is singularly designed to destroy productivity growth as labour efficiency is outweighed by capital mis-allocation. It implicitly offshores ownership of assets. It has a chronic reliance upon high current account deficits. And it hollows out every non-mining tradable not bolted down, substituting export income with offshore debt.

It is now not so much an economy as it is a fiercely protected banking and resources rort that systematically denudes workers of income and rising living standards. It is a rampant class war that includes mass immigration, systematic visa rorting, hollowing out, wholesale support for property capital owners, de-unionisation, the rise of robots and media corruption. Yet somehow in the mind of the RBA head these structural features of the labour market are secondary to worker anxiety and timidity in the production of low income growth.

That is Australian exceptionalism gone mad.

At MB we remain committed to reform. Even today we believe that a swing to appropriate policy can mitigate the worst outcomes of the adjustment. We are rationalist liberals not Marxist apparatchiks. Yet it behooves me to note on behalf of both the rorted workers and their capital betters that if this gigantic scam persists for long enough then it may just be that it will need to be ripped out at the roots and burned.