10 years of economic blunders are coming to a head

There’s a lot of eminent macro managers with invisible egg on their faces today. It’s invisible because, as we know, there is no accountability in Dumbstralia outside of MB. Nonetheless, it’s there, in great dripping omelettes of failure.

It began during the post-GFC period when the then Labor Government refused to acknowledge the structural challenge confronting Australia’s externally-funded economic model. Having acted decisively and appropriately during the GFC, afterwards Labor refused to remove bank guarantees and to undertake much needed financial architecture reform.

That left the RBA in charge. It did a pretty good job post-crisis of explaining to Australians that household debt was dangerously high at just over 100% of GDP. It hiked interest rates into the commodities boom and forced banks to raise deposits over offshore debt.

But, it also covered its own arse. Rather than admit Australia was lucky during the GFC, it inflamed a narrative of Australian exceptionalism, and fell madly in love with the China boom, extrapolating it 30 years into the future.

Thus it overcooked its rate rises and egged on a charging Australian dollar to “structurally adjust” Australia to “mining-led growth”. This afflicted the economy with a paralytic dose of Dutch disease that threw every non-mining tradable not bolted down into the sea, culminating in the collapse of the car industry.

What a fateful mistake it was. The RBA’s thirty year boom instead lasted for three. As the mining boom turned to mining bust in 2012, the RBA and Treasury panicked, suddenly forgot that they’d told households they had enough debt and instead instructed everyone to gamble on house prices, literally told them to do it.

Any first year economics student can tell you what you have to do to fix a boom that has priced-out an economy’s competitiveness. You have to deflate your input costs and currency plus improve productivity. Over time, improving competitiveness works its magic and investment picks up. That drives jobs and demand and a virtuous cycle forms. It’s called a real exchange rate adjustment.

We did the opposite. It took a lot of rate cuts and an unexpected influx if Chinese buyers, but eventually the RBA succeeded in forcing households to go property mad again. The new boom across 2013-15 took the form of wildly risky lending for investment loans, including crazy levels of interest-only schlock. It kept enough consumption running to partially offset the mining crash, drove input costs mad and prevented the currency from falling.

Meanwhile, governments changed. A revitalised Coalition set about Budget repair which it needed to do given that the Budget’s AAA rating still guaranteed the foreign borrowing now fueling the re-blowing housing bubble. Sadly, the Abbott Government did not understand the economy it was running. It brought class war to the job instead of structural reform targeting productivity and threatened to rip the away the very middle class welfare that supported all of that household debt. Needless to say, its polling collapsed.

And so, public borrowing mushroomed instead. Not usefully spent on infrastructure, nor made more efficient, just frittered away mostly on supporting demand. Governments changed again and we saw more waste. Throughout, all governments kept the foot on the immigration accelerator ensuring that the debt and house price frenzy could not stop.

Finally in 2015, as wages kept falling along with inflation and a chronically weak economy, monetary authorities realised they’d buggered it all up. They began begging markets for a lower currency and installing the very macroprudential tools to control household debt that they had scornfully dismissed just a year earlier.

But their bubble had taken on a life of its own now. A new Turnbull Government egged it on as well. They were forced to tighten again in 2017.

The final blundering arrived with the Turnbull Government’s first Budget. Rather than undertake productivity reform to repair the numbers it turned to fantasy growth assumptions to do it, ensuring that the sovereign rating will be stripped in due course as the numbers collapse.

Which brings us to today. Here we are barely one third of the way through the inevitable real exchange rate adjustment and our :

- household debt imbalance is now nearly one third higher than when we were told it was dangerously high;

- public balance sheet increasingly awash with red ink and on track for downgrade later this year raising external interest rates on the same great debt pile and

- the economy barely has a pulse.

All of this just as we’re entering the final great washout of the commodities bust as iron ore and coking coal crash.

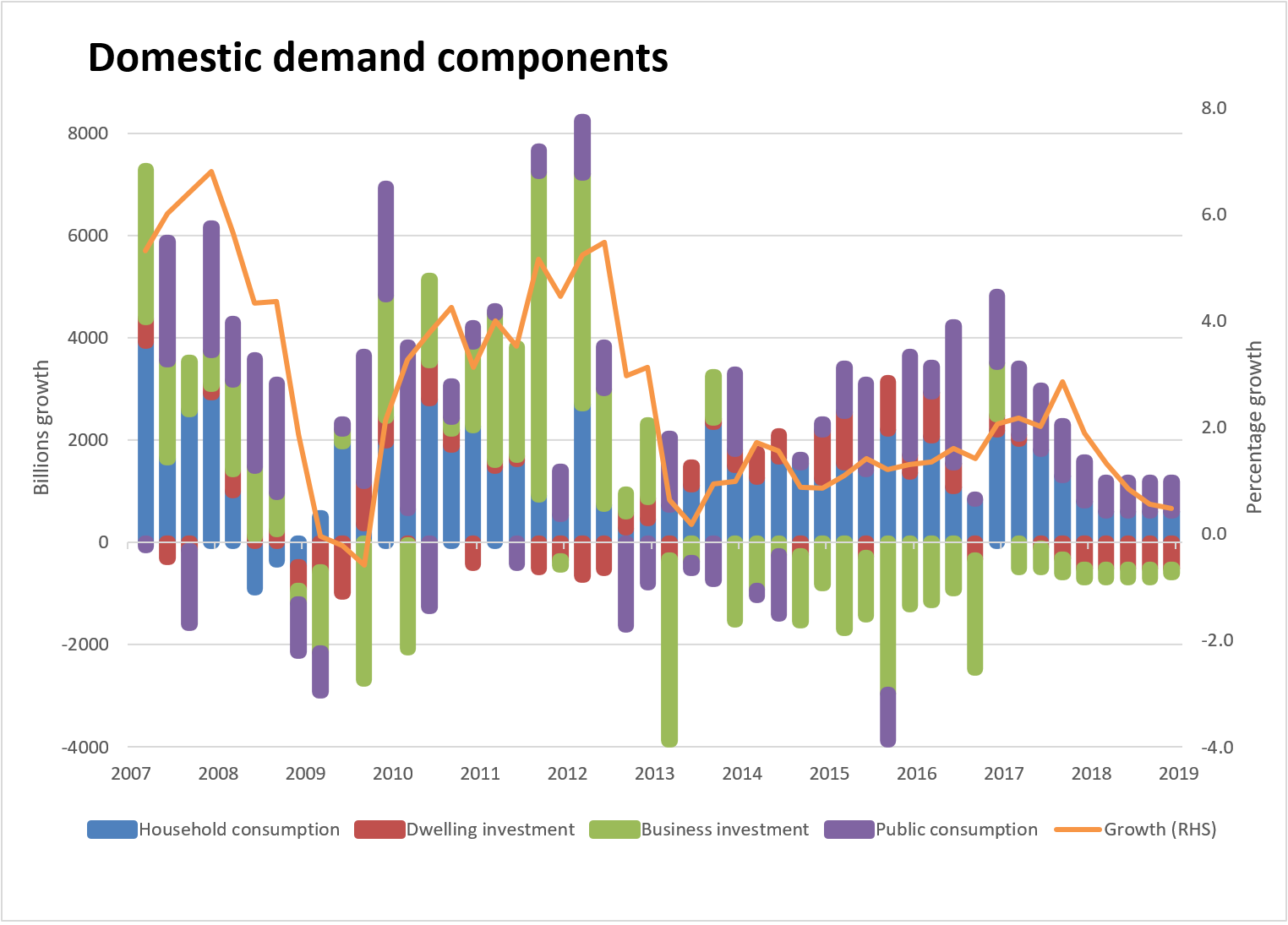

Let’s make no bones about it, 10 years of economic blunders are coming to a head. The five major drivers of GDP are stalling:

- household consumption;

- public consumption;

- dwelling investment

- business investment, and

- net exports.

On the first, we’ve all seen retail’s woes. But it’s worse. Weak income and reliance on a gigantic bubble for savings is retarding household spending. Leading indicators are suggesting a first quarter annualised spend at 2%, well down on Q4. Moreover, as house prices stall, spending will slow even more. In 2011/12 when house prices were falling mildly, national household consumption fell under 1% for five quarters. We’re going back there. It will add roughly 0.3% to GDP over the next year.

On the second, federal and state budgets are going to inject some demand this year through infrastructure and simple spending adding 1% to GDP.

On the third, the dwelling construction boom has peaked or is about to and will begin to draw down at roughly -7% per annum and pulling roughly -0.3% out of GDP.

On the fourth, investment is still falling fast as it traces the mining bust and services are to slow too as broader demand wavers. It’s going to withdraw roughly 1% of GDP.

Last, net exports are going to subtract big from Q1 and Q2 this year but add strongly thereafter, adding a net 1% to GDP.

That all adds up to a stall speed economy, limping along along government largesse and net exports that add no local activity.

Now add the primary driver of income in the economy: the terms of trade. As iron ore and coking coal literally collapse so too do the terms of trade, withdrawing income and exacerbating all of the above. The collapse is destroying the Budget and the sovereign rating will be stripped this year.

Thus already weak domestic conditions are going to get much weaker:

Unemployment is going to rise, probably sharply. Rates are going to be cut. The ASX and Australia dollar are going to fall. All of this and no global shock. Quite a feat of economic mismanagement.

If you do not already have your dough parked offshore then do it. If you are long Aussie equity, get long bonds instead. If you are long property then visit your priest.

Australia is about to decouple completely from the global reflation. Get your money out.

We can help you with all of the above with the MB Fund launching July 1 2017 (it has passed compliance). Those pre-registered will be invited in a little earlier. Register your interest today (if you have not already):