Credit Suisse:

In our view, retail faces seismic change. We highlighted previously (link) the high cost structure of retail in Australia. With Amazon’s disruption potential, it is important for retailers and investors to think strategically about the retail value chain.

■ An alternative paradigm. An alternative way of thinking about the retail proposition is to view the retailer as selling an entry ticket. Goods are then supplied at ex warehouse cost, once the customer enters the store and ‘buys’ a ticket.

■ The cost of a ticket. Take the example of a A$200 purchase – a pair of sports shoes at Rebel, an entry level tablet or pair of speakers at JB Hi-Fi or Harvey Norman, or an item of clothing or beauty products at Myer. At JB Hi-Fi, a customer would be paying, on average, A$45 to enter the store and buy the product at ex warehouse cost. At Harvey Norman, we think the cost would be higher than JB Hi-Fi (not disclosed), but we assume A$50. At Rebel, a customer would be paying A$90 on average. At Myer, a customer would be paying A$70 on average. The question for the retailer and investor is whether there is enough value to sustain the ticket price. Is there a defense in big and bulky? Maybe not. The proposition is potentially worse for higher priced items. Think of the ‘cost of the ticket’ for that A$5,000 television.

■ Store-based home delivery models currently offer low value. A storebased delivery model encompasses the full cost of a store and an additional delivery cost. Perplexingly, in many cases, there is no additional value compared with a centralised delivery model. The prevalent delivery model by store-based retailers is to put goods back into a centralised distribution system (such as a postal service). Yet, in many cases, a retailer’s store would be within 20 minutes travel time of most of its customers. The retailer has incurred the cost of being proximate to its customers and could potentially add value to the ‘ticket’ with a significantly shorter delivery time

frame.

■ Alternative channels, alternative value propositions. We have little doubt that many customers would travel a reasonable distance to save A$50. That is the warehouse club proposition, which has been reasonably successful. In many cases, a centralised distribution and delivery would provide a lower cost ‘ticket’ and in other cases ‘delivery to the door’ would provide a high value proposition. Alternative value propositions invariably take some share from incumbents. The challenge for incumbents is to add value to the ticket and/or reduce the cost of a ticket.

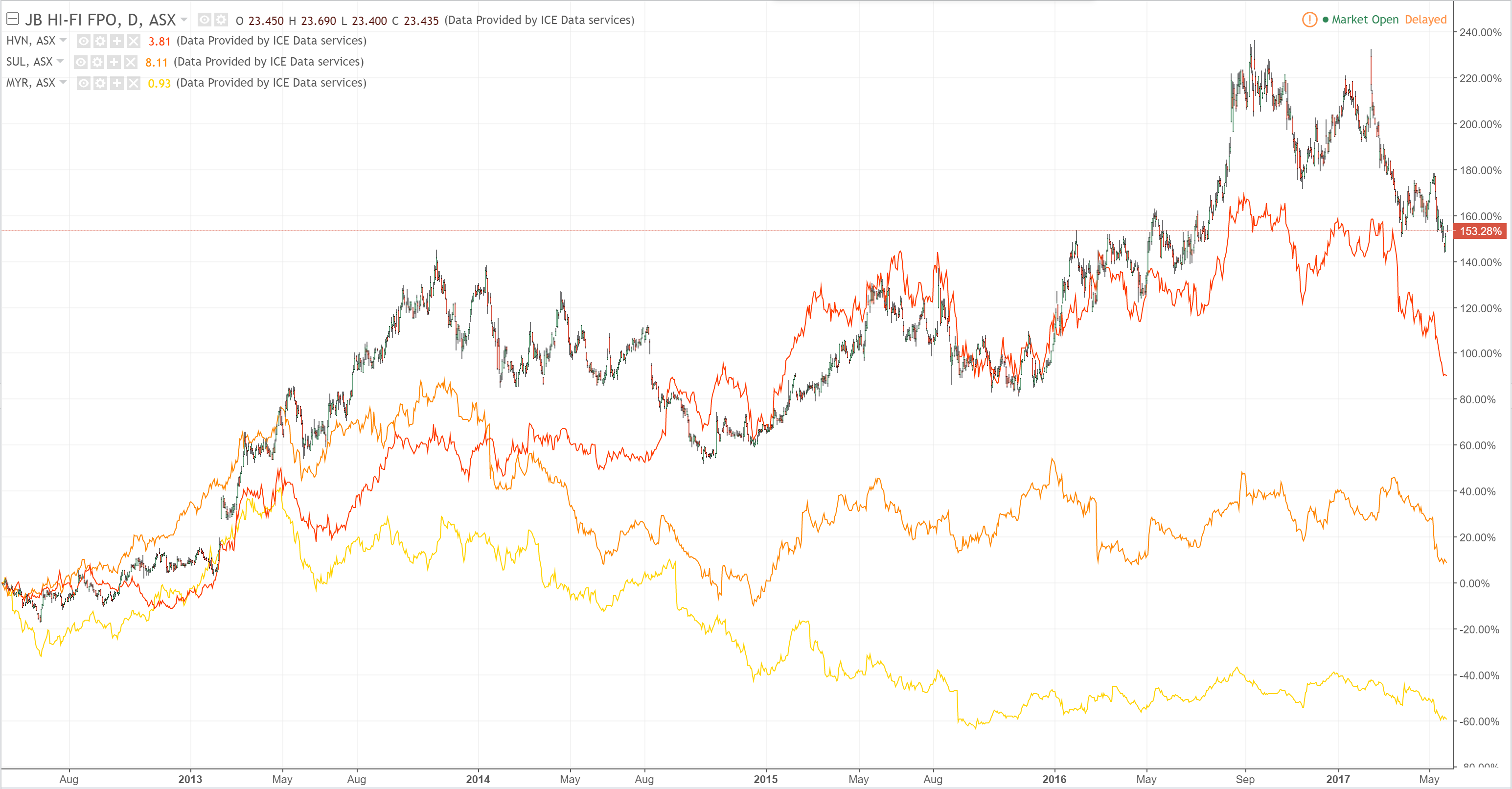

■ In our view, SUL and MYR are vulnerable to disruption because of their high cost structures and the relatively low value delivered by the store experience. HVN appears to operate a higher cost model than JBH. JBH operates a relatively low cost structure, to its advantage, but the value of the ticket is relatively low.

Share prices:

Add the tapped out consumer…