Three takes today that run from the ridiculous to the sublime around buying miners. Ridiculous is Credit Suisse:

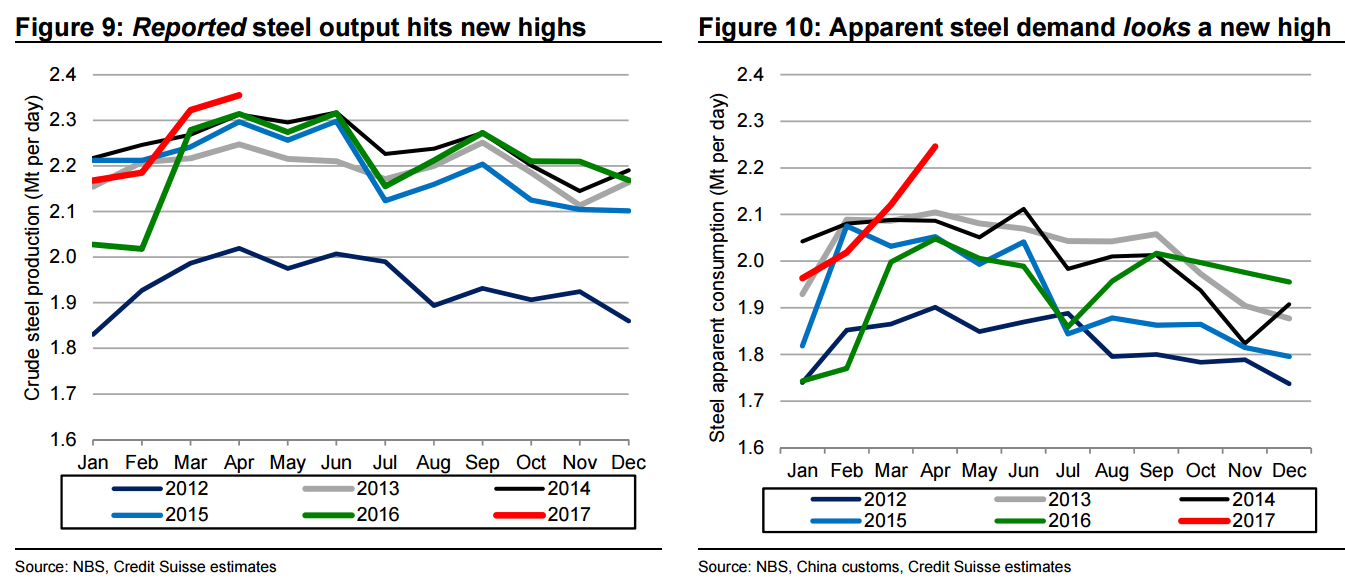

April stats of record production really point to record iron ore consumption China’s reported steel production and apparent consumption for April hit record levels. However, as we discussed in our Iron Ore Forecast note of 17 May, we doubt production or consumption really is a record. Rather, we think it is steel production becoming visible as it migrates to integrated steel mills, following the closures of the illegal Induction Furnaces. It is highly likely that output from that “secret capacity” was never previously reported. The Government says that so far it has closed 500 substandard quality production facilities for 119Mtpa of capacity. All are due to be closed by 30 June. The production from the Induction Furnaces is uncertain as it was never recorded. Platts estimates 30-50Mtpa, Mysteel thinks it was 60Mt, others suggest 70Mtpa. If we use a range of 40-70Mtpa, that would equate to 0.1-0.19Mt per day missing from steel output statistics in previous years. Mysteel think the output was occurring in 2015, but how far back in time it extends is also uncertain. What we can assume is that China’s steel output was not really ~800Mtpa in recent years. It was probably ~840 – 870Mt.

The major implication we see from the production statistics is that iron ore consumption must be at a record. If we assume that previous years iron ore production was understated, then steel output this year may be similar to previously. But the big change is that the hidden capacity in previous years was all derived from scrap. The lift in steel production now that has become visible is dominantly blast furnace-based steel production, using iron ore. Therefore it seems almost certain that iron ore consumption in China has hit a new record, to generate that reported record steel production. The importance of that conclusion is what it means for port stocks. There has for some time been a conflict between iron ore stocks assessed as absolute tonnes, which are a record 138Mt (Figure 11) and a Mysteel survey of imported stocks held by 65 steel mills ( in the mill yard, at ports and inbound ships) which look low at 23 days of consumption (Figure 12). Part of the discrepancy may be that steel mills have chosen to hold more of their stocks at port since mid-2016, but another part is that the iron ore consumption rate is the highest ever since the crackdown on Induction furnaces started late last year, and therefore stocks measured as days of consumption remains stable. A higher call on iron ore needs to be supported by higher stocks. Viewed in that light, the worry over high port stocks seems overdone. Port stocks will really only look excessive when iron ore consumption rates reduce – which we expect late in the year in line with seasonal norms. That’s when we would expect steel mills to destock, putting pressure on seaborne iron ore prices in 4Q.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.