• In our opinion, economic imbalances in Australia have increased due to strong growth in private sector debt and residential property prices in the past four years, notwithstanding some signs of moderation in growth in recent weeks. Consequently, we believe financial institutions operating in Australia now face an increased risk of a sharp correction in property prices and, if that were to occur, a significant rise in credit losses.

• Despite increased downside risks, in our base case we expect that recent and possible further actions by the Australian authorities should aid in an unwinding of the imbalances in an orderly fashion.

• To reflect the increased risk, we have lowered our assessment of the stand-alone credit profiles (SACPs) of almost all financial institutions operating in Australia.

• We are lowering our long-term issuer credit ratings on 23 financial institutions in Australia by one notch each.

• We are affirming our issuer credit ratings on the four major Australian banks reflecting our expectation of likely timely financial support from the Australian government, if needed–which in our view offsets the deterioration in these banks’ SACPs. Nevertheless, these banks remain on negative outlooks, reflecting potential pressures on government support.

• We are also affirming our ratings on Macquarie Bank and Macquarie Group. The outlook on Macquarie Bank remains negative and we have revised the outlook on Macquarie Group to stable.

• Our ratings on five foreign-owned financial institutions, three entities owned by larger domestic financial groups, and one Australian government-owned financial institution remain unchanged because our ratings on these institutions primarily reflect our unchanged assessment of the likelihood of financial support from their parents, if needed.

MELBOURNE (S&P Global Ratings) May 22, 2017–S&P Global Ratings today said that it has lowered its long-term issuer credit ratings on 23 financial institutions operating in Australia. At the same time, we have revised our

outlooks on most of these financial institutions to stable. Our outlooks on seven financial institutions remain negative (see ratings list below).

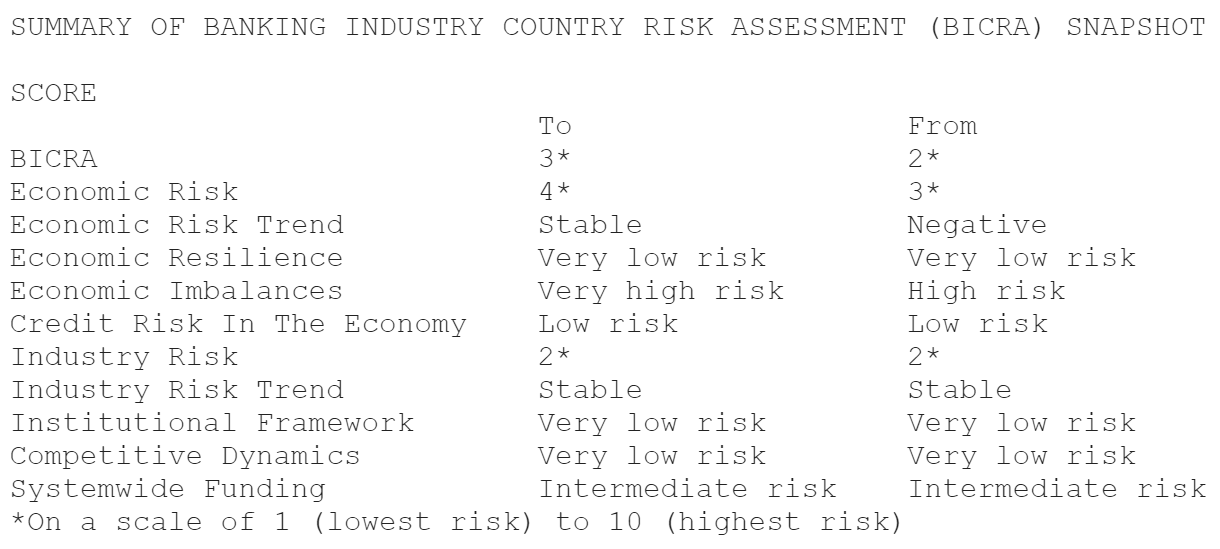

The rating actions reflect our view that continued buildup of economic imbalances in the country over the past few years due to a rapid rise in private sector debt and house prices–particularly in two of the most populous cities of Sydney and Melbourne–has exposed Australian financial institutions to greater economic risks (see our Banking Industry Country Risk Assessment (BICRA) snapshot, below). To reflect the increased risk, we have lowered our assessment of the stand-alone credit profiles (SACPs) of almost all financial institutions operating in Australia.

Strong growth in private sector debt (which we estimate will increase to about 136% of GDP in June 2017 from 117% in 2013, or an annual average increase of 4.6 percentage points) coupled with an increase in property prices nationally (our estimated average inflation-adjusted increase for the four years to June 2017 is 6.4% nationally) have driven the buildup in imbalances in the economy, in our view. We note that the strong growth in property prices continued within Melbourne and Sydney contrary to our base-case expectation that we articulated in October 2016, when we revised the outlooks on our ratings on most Australian banks to negative.

Consequently, we believe the risk of a sharp correction in property prices has increased. We consider that if this downside scenario were to occur, all financial institutions operating in Australia are likely to incur significantly greater credit losses than at present. In addition, with residential home loans securing about two-thirds of banks’ lending assets, the impact of such a scenario on financial institutions would be amplified by the Australian economy’s external weaknesses, in particular its persistent current account deficits and high level of external debt.

Despite our view that the risk of a downside scenario and its impact have increased, we consider the outlook for the Australian banks remains relatively benign by global standards. We consider that recent and possible further actions by the Australian authorities should aid in an unwinding of the imbalances in an orderly fashion, as has generally been the case in the past several cycles in Australia–and may have already started in Sydney and Melbourne. This is most likely to occur through slower growth–or even a mild drop–in property prices over the next two years, without causing any significant increase in credit losses incurred by the Australian banks. Nevertheless, we consider that until the imbalances have materially unwound, the banking system in Australia remains exposed to elevated risks of a sharp correction in property prices and its consequences; our rating actions announced today reflect these heightened risks.

AUSTRALIAN MAJOR BANKS

Our issuer credit ratings on the four major Australian banks–Australia and New Zealand Banking Group Ltd., Commonwealth Bank of Australia, National Australia Bank Ltd., and Westpac Banking Corp.–remain unchanged and on negative outlook. Similar to most other financial institutions operating in Australia, we have lowered our assessment of the SACPs of the Australian major banks by one notch, reflecting increased economic risks. In addition, we have lowered our ratings on the hybrid and nondeferrable subordinated debt instruments issued by these banks and their banking subsidiaries by one notch. This reflects our view that government support for these banking groups is unlikely to be extended to their hybrid and subordinated debt instruments. Nevertheless, we have affirmed our long-term issuer credit ratings on these banks reflecting our expectation of likely timely financial support from the Australian government, if needed–which in our view offsets the deterioration in these banks’ SACPs.

Our outlooks on the long-term issuer credit ratings on the four major Australian banks remain negative reflecting our view that pressure remains on the Australian government’s likely support for these banks. We expect to lower our issuer credit ratings on these major banks and their core subsidiaries if we lowered our long-term local currency sovereign rating on the Commonwealth of Australia (AAA/Negative/A-1+) or if we reclassified our assessment of the Australian government’s supportiveness toward systemically important private sector banks to supportive from highly supportive.

MACQUARIE BANK AND CUSCAL

Our ratings on Macquarie Bank Ltd. and Cuscal Ltd. currently benefit from our expectation that the Australian government is likely to provide timely financial to support to these institutions, if needed. Consequently, our outlook on both these institutions remains negative reflecting our view of continued pressures on likely support from the Australian government. Our outlook on Macquarie Group Ltd. is stable because our rating on the nonoperating holding company does not incorporate any uplift due to potential government support.

We are affirming our rating on Macquarie Bank reflecting our view that the bank’s stronger capital position offsets the increase in systemwide risks such that the group credit profile remains unchanged–we now expect that the bank will maintain its risk-adjusted capital ratio at a stronger level compared with our previous expectation. We have lowered our assessment of the SACP of Cuscal, but we have affirmed our long-term issuer credit rating on the company reflecting our expectation of likely timely financial support from the Australian government, which in our view offsets the deterioration in Cuscal’s SACP.

FOREIGN-OWNED BANKS, EFIC, BIG SKY, QTMB, AND SUNCORP-METWAY

Our ratings on the following nine institutions also remain unchanged: five foreign-owned financial institutions, namely Citigroup Pty Ltd. (A/Stable/A-1), Goldman Sachs Financial Markets Pty Ltd. (A+/Stable/A-1), HSBC Bank Australia Ltd., ING Bank (Australia) Ltd., and JPMorgan Australia Ltd. (A+/Stable/A-1); and four domestically owned institutions, Export Finance & Insurance Corp. (EFIC; AAA/Negative/A-1+), Suncorp-Metway Ltd., Big Sky Building Society Ltd., and QT Mutual Bank Ltd. Our ratings on these entities incorporate our assessment of likely financial support from their parents. We have lowered our SACPs on HSBC Bank Australia, ING Bank Australia, Big Sky, QTMB, and Suncorp-Metway (we do not currently assess SACPs on EFIC and the above-mentioned rated Australian subsidiaries of Citigroup, Goldman Sachs, and JPMorgan). Nevertheless, we consider that such an increase in risks for the Australian banking system would have no significant impact on the capacity for these entities’ parents to support them, or the likelihood of such parent support being made available, if needed. Our outlook on EFIC remains negative, reflecting the negative outlook on its parent and guarantor, the Commonwealth of Australia.

FPFL

We have lowered our issuer credit rating on New Zealand-based Fisher & Paykel Finance Ltd. (FPFL) by one notch reflecting our opinion that the group credit profile of its Australia-based parent FlexiGroup Ltd. has weakened due to increased economic risks–similar to those faced by other Australian financial institutions. We equalize our issuer credit rating on FPFL with our assessment of the group credit profile of its parent, FlexiGroup, reflecting our view that FPFL is a core subsidiary of the group and that the parent is therefore highly likely to provide timely financial support to FPFL, if needed.

MYSTATE AND AUSWIDE

In addition to one-notch rating downgrades, our outlook on MyState Bank Ltd. remains negative and we have placed our ratings on Auswide Bank Ltd. on CreditWatch with negative implications. This is because in our capital analysis for all banks, we now apply higher risk weights for bank loans to the Australian private sector, reflecting increased economic risks. Consequently, other things remaining equal, our forecast capital ratios for all financial institutions would weaken. In the case of MyState and Auswide, we consider that their weakening capital ratios may become significant enough to cause a further rating downgrade by one notch. The negative outlook on MyState reflects our assessment that the bank may face challenges maintaining its capital ratio commensurate with the revised rating–although in our base case we expect it would do so. We need further information to form a view on the

likelihood of Auswide maintaining a capital level commensurate with the revised rating. In the next three months, we expect to assess Auswide’s capital strategy and capacity to determine whether we should lower the ratings further.

POLICE & NURSES LTD.

We have affirmed our ratings on Police & Nurses Ltd. (trading as P&N Bank) reflecting our view that the bank’s strengthening risk position–as it continues to make progress in exiting the group’s riskier property lending and equity exposures–offsets the increase in systemwide risks such that the group credit profile remains unchanged. We consider risks related to delays in the P&N group’s planned exit from its property sector exposures are now adequately captured within the assumptions underlying our risk-adjusted capital analysis. Nevertheless, the emergence of significant losses from this sector would pressure the rating on the bank.

QUDOS MUTUAL

We have lowered our SACP–and consequently our issuer credit rating on–Qudos Mutual Bank Ltd. reflecting the rise in systemwide risk. Nevertheless, we have revised our outlook to positive reflecting our opinion that there remains a one-in-three chance that over the next two years the mutual bank’s risk position would improve if it is able to successfully implement and leverage its technology investments on time and within budget.

WEBCAST

S&P Global Ratings will host a webcast and Q&A at 2:00pm Melbourne time on Wednesday, May 24, 2017, to discuss today’s ratings actions and our insights on the Australian banking sector. If you would like to attend the webcast, please contact Richard Noonan at richard.noonan@spglobal.com.

SUMMARY OF BANKING INDUSTRY COUNTRY RISK ASSESSMENT (BICRA) SNAPSHOT

S&P clearly requires considerable re-education that Australia is different. Stocks of MB’s Spruikbot Telephunken U-47 are still available and can be delivered within 24 hours:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.