The Australian went into full whinge mode over the weekend attacking the 0.06% levy on the big 5 banks’ liabilities, which are projected to raise $6.2 billion over the Budget forward estimates.

First up, here’s Henry Ergas, who howled ‘inefficiency’:

In essence, these levies are a tax on an input used in supplying banking services, namely wholesale deposits — they are, in other words, typically calculated as a percentage of the amounts the banks borrow, mainly from global capital markets, to fund their loans. Those borrowings are a substitute for the deposits banks obtain from retail customers, in the sense that banks can finance their operations from one or the other…

As a result, a tax on wholesale borrowings does not only increase banks’ costs in aggregate, it also skews their funding decisions, leading them to turn from what otherwise would be a lower-cost source of funds — loans from capital markets — to higher-cost sources of funds, such as retail deposits… making banking services costlier to produce…

Seen in those terms, the levy is positively perverse. In effect, the levy will induce banks to rely to a greater, rather than lesser, extent on retail deposits, as it makes them cheaper compared to wholesale borrowing.

And here’s my cousin, Peter van Onselen, who claims the policy is ‘populist’:

The handling of the announcement and future introduction of the new bank tax is a triumph of short-term politics over policy. Rather than do the hard work to get their finances in order, this government is arbitrarily taxing a section of the business community. First they came for the banks.

…once the legislation for the tax is enacted it will be easy for future governments under fiscal pressure to simply push the six basis points tax slightly higher to help bring in a few extra hundred million dollars of taxation revenue whenever politicking requires it. It will become an easy substitute to serious reform…

This tax is a failure of good policymaking, Liberal philosophy and it risks setting a precedent for similar ad hoc taxes when fiscal strains require it. The government doesn’t care because being at war with the banks is good short term politicking.

Neither arguments hold much weight.

Henry Ergas’ concern that the banks will turn away from wholesale funding towards retail deposits is non-nonsensical, since it is wholesale funding from offshore capital markets that has caused Australia’s banking system to be so risky in the first place. Here’s S&P’s comments on the matter last week:

We believe Australia’s high level of external indebtedness creates a high vulnerability to major shifts in foreign investors’ willingness to provide capital…

We believe Australia’s general government-sector fiscal outcomes need to be stronger than its peers’ and net debt needs to remain lower to remain consistent with the current ‘AAA’ rating. This is because Australia’s economy is highly vulnerable to any major shift in offshore capital flows. The economy carries a high level of external debt, exacerbated by typically high current account deficits, volatility in the country’s terms of trade, and a large stock of short-term external debt. Australia’s external debt net of the liquid assets of the public and financial sector (our preferred stock measure) is high, at about 250% of current account receipts. Australia’s short-term external debt, which is mostly bank debt, will also remain high, at 170% to 180% of current account receipts during the forecast period…

Australia’s international investment position remains a major weakness in the sovereign credit profile. At 246% of current account receipts, Australia’s net external liabilities are the second largest among all investment-grade rated sovereigns… This weak external position is a result of decades of sizeable current account deficits, financed by external borrowing. While highlighting the inherent vulnerabilities associated with Australia’s high stock of external debt and structural current account deficits, we also note that they are mostly generated by the private sector… However, a portion of Australia’s external debt has also funded a surge in unproductive household borrowing for housing during the 1990s and 2000s intermediated by the banking sector.

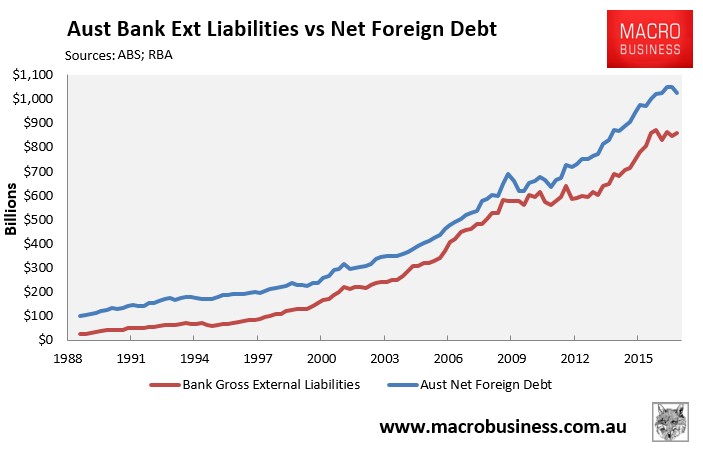

And here’s a chart showing how the banks’ heavy offshore borrowings have driven-up Australia’s external debt:

If the Coalition’s bank levy reduces reliance on offshore funding towards more stable deposit funding, this will be an excellent results, since it will effectively de-risk the banking sector.

Sourcing more of the banks’ funding domestically should also reduce capital inflows and put downward pressure on the Australian dollar, thus assisting trade-exposed industries – another excellent result.

The big banks are also unlike other companies in that they receive massive taxpayer support, which lowers their cost of funding and enables them to make super-sized profits – hence the rationale for the bank levy. These taxpayer supports, estimated to be worth $5 billion per year, include the Budget’s implicit guarantee over the banks (which provides a two-notch improvement in the banks’ credit ratings), the RBA’s Committed Liquidity Facility, and deposit insurance.

Do either Ergas or my cousin seriously suggest the banks should receive these subsidies free of charge? How is that an ‘efficient’ outcome?

No, the bank levy is efficient because it will help internalise part of the cost of the Government’s support of the banks. If anything, the levy should have been higher – roughly triple – to fully cover the cost of support provided on behalf of taxpayers to the banks.

unconventionaleconomist@hotmail.com