OVERVIEW

• The sovereign credit ratings on Australia benefit from the country’s strong institutional settings, its wealthy and resilient economy, monetary policy flexibility, and low government debt. The country’s high external indebtedness and vulnerability to weak commodity export demand moderate these strengths.

• We are affirming our ‘AAA’ long-term and ‘A-1+’ short-term sovereign credit ratings on Australia.

• The rating outlook remains negative, reflecting risks to the government’s fiscal consolidation plan and risks to the economic, fiscal, and financial stability outlook should the rapid growth of credit and house prices continue.

RATING ACTION

On May 17, 2017, S&P Global Ratings affirmed its ‘AAA’ long-term and ‘A-1+’ short-term unsolicited sovereign credit ratings on the Commonwealth of Australia. The outlook remains negative.

RATIONALE

The negative outlook on Australia reflects our view that if downside risks to government revenue materialize, then budget deficits could persist for several years, with little improvement, unless the parliament implements more forceful fiscal policy decisions. We believe Australia’s high level of external indebtedness creates a high vulnerability to major shifts in foreign investors’ willingness to provide capital, and we consider that strong fiscal performance and low government debt are important to help ameliorate this risk. Strong fiscal accounts are also a precondition for countercyclical policies to stabilize the economy if needed, such as in the case of a slump in the buoyant housing market.

Along with strong institutions, a credible monetary policy, and floating exchange-rate regime, Australia’s public finances traditionally have been a credit strength for the sovereign rating. More recently, however, they have weakened. Australia’s fiscal position has continued to weaken with successive governments since the global financial recession of 2008-2009 and the peak in export commodity prices in 2011, delaying an eventual return to budget surpluses. The central government’s current projection date for a balanced budget in fiscal 2021 (the year ending June 30, 2021) is eight years later than the previous government’s 2010 projection of fiscal 2013. If achieved, it would come more than 10 years after the global recession pushed the central government budget into deficit. This substantial delay in fiscal repair, and the risk of further delay, raises our doubt over the ability of the Australian government to meet its fiscal objectives.

The government’s fiscal 2018 budget, which it tabled on May 9, 2017, indicates a similar path of fiscal balances to its budget released in May 2016. The government continues to project, as it did a year ago, that the budget will be in surplus by fiscal 2021, though we believe this would require additional restrictive measures. While the government’s surplus target remains unchanged, its forecast fiscal deficits are slightly wider in the next couple of years than in its May 2016 forecasts, largely reflecting the negative effects of

weak wage growth and inflation on government revenues. We cited this as a risk when we revised the rating outlook to negative in July 2016, and believe that the potential for wage growth and inflation to remain low remains a downside risk to the government’s current projections.

Downside revenue risks from commodity prices have receded in the near term, though they persist. Indeed, our medium-term price forecasts remain a little lower than those in the government’s latest budget. Iron ore and coal prices have been much higher than we expected a year ago, though more recently they have lost much of their late 2016 gains; metallurgical coal prices recently spiked again due to disruptions in Australian supply. These price gains are likely to boost government revenue next fiscal year, but we expect export commodity prices to settle only a little higher than we projected a year ago and we do not expect a significant medium-term benefit to government revenues (see “S&P Global Ratings Updates Its Price Assumptions For Aluminum, Copper, And Iron Ore For 2017-2019,” published April 10, 2017).

Overall, we believe that the balance of risks to government revenues remains negative. On the policy front, enacting further savings or revenue policies could remain a challenge, given the Senate’s unwillingness in recent years to legislate many of the government’s fiscal policy measures or doing so after considerable delay. This dynamic, which could continue, presents further downside risk to the outlook for fiscal balances. We therefore continue to think that budget surpluses could remain elusive beyond fiscal 2021.

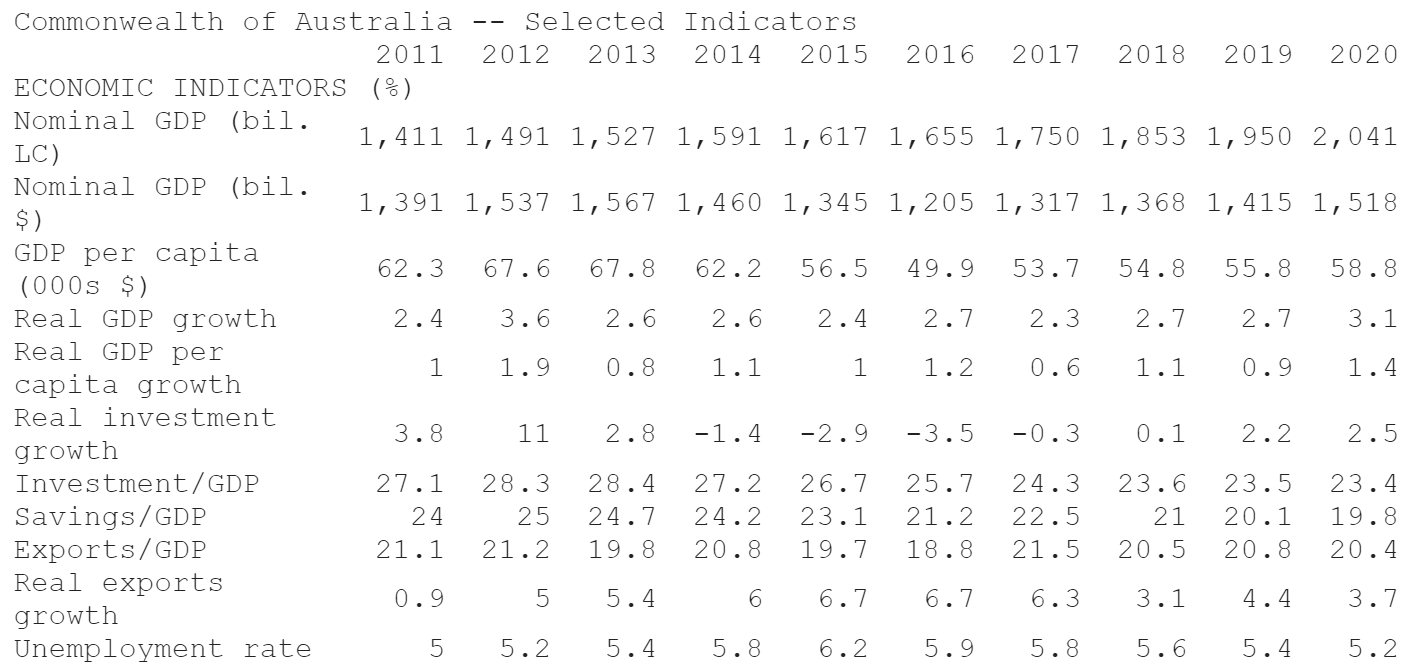

Our fiscal measures incorporate the federal, state, and local government levels. At the state government level, we expect fiscal deficits to widen again in the next couple of years, after narrowing in recent years, largely as states boost their infrastructure spending. This is weighing materially on the outlook for general government sector fiscal deficits, though the effect on debt likely will be tempered by state asset privatizations. We expect net general government debt to peak a little higher than we had thought, but to remain low, at about 27% of GDP. This reflects our revised fiscal outlook and some off-budget spending. The off-budget spending is mainly in the form of loans, though we do not consider these loans to be liquid assets and consequently do not subtract them from gross debt. Low interest rates are also helping keep the general government sector’s interest expense burden low, at less than 5% of revenues.

We believe Australia’s general government-sector fiscal outcomes need to be stronger than its peers’ and net debt needs to remain lower to remain consistent with the current ‘AAA’ rating. This is because Australia’s economy is highly vulnerable to any major shift in offshore capital flows. The economy carries a high level of external debt, exacerbated by typically high current account deficits, volatility in the country’s terms of trade, and a large stock of short-term external debt. Australia’s external debt net of the liquid assets of the public and financial sector (our preferred stock measure) is high, at about 250% of current account receipts. Australia’s short-term external debt, which is mostly bank debt, will also remain high, at 170% to 180% of current account receipts during the forecast period.

Fiscal accounts also need to be strong to offset risks from the multiyear domestic credit and housing boom. House prices have risen by over two-thirds nationwide since 2009, but our concern is most acutely focused on financial stability risks in Sydney and Melbourne, where median house prices have broadly doubled during the same period. At the same time, bank credit to private-sector residents has increased rapidly, rising to 175% of GDP in 2016 from 144% five years earlier. We currently forecast that the credit-to-GDP ratio will continue to rise, reaching 188% in 2020. Recent financial history in other developed markets reconfirms that such rapid credit growth can lead to vulnerabilities with regard to financial, fiscal, and economic stability if the dynamic expansion experiences a sudden and unexpected slowdown.

In terms of external performance, current account deficits have narrowed markedly during the past few quarters, and the annual deficit in fiscal 2017 is likely to be about 1.8% of GDP, down from 4.4% in fiscal 2016. We believe this stronger performance is likely to be temporary, however, in line with similar episodes in the past. We expect current account deficits to return to more than 3% of GDP in the next few years, partly driven by weaker export values as commodity prices decline further. We therefore expect current account deficits to remain above 10% of current account receipts, which we consider to be high, and the economy’s external debt stock to also remain high.

Australia’s international investment position remains a major weakness in the sovereign credit profile. At 246% of current account receipts, Australia’s net external liabilities are the second largest among all investment-grade rated sovereigns, just behind the U.S. (see “Sovereign Risk Indicators,” April 7, 2017; a free interactive version is available at http://spratings.com/sri). This weak external position is a result of decades of sizeable current account deficits, financed by external borrowing. While highlighting the inherent vulnerabilities associated with Australia’s high stock of external debt and structural current account deficits, we also note that they are mostly generated by the private sector and reflect the productive investment opportunities available in Australia, foreign investor confidence in Australia’s rule of law, the high creditworthiness of its banking system, and the positive yield available on highly rated debt. However, a portion of Australia’s external debt has also funded a surge in unproductive household borrowing for housing during the 1990s and 2000s intermediated by the banking sector.

We expect Australia’s external borrowers to maintain easy access to foreign funding. We note that the Reserve Bank of Australia (RBA, the central bank) has maintained a freely floating exchange-rate regime for more than three decades, the Australian dollar represents 1.8% of allocated international reserves as of Dec. 31, 2016, and the currency is represented in a comparable percentage of spot foreign-exchange transactions. Australia’s domestic bond market is deep, and although external borrowing is high, it is mostly denominated in the nation’s own currency or hedged. We consider Australia’s banking system to be one of the strongest globally. Along with the resilient and high-income Australian economy, this reflects the low risk appetites of the major banks, which dominate the industry, supported by conservative and proactive regulatory and governance frameworks. However, risks have increased as a result of the current extended period of high house price inflation and rising household indebtedness; household debt, including debt for unincorporated businesses, now stands at nearly 190% of household income.

We view Australia as possessing a high degree of monetary credibility. This key credit strength helps the country to attenuate major economic shocks, which could come, for example, from a slump in Australia’s property market or a sharp downturn in China’s economy. We believe the RBA’s success in anchoring inflation expectations would allow it to lower policy interest rates from their current level of 1.50% to support growth, even if the currency were to weaken further, given the historical low pass-through to inflation.

Australia is a wealthy, diversified, and resilient economy, with GDP per capita of an estimated US$54,000 in fiscal 2017. We believe the economy’s resilience and flexibility ultimately help cushion government finances from economic shocks and are a major support to Australia’s creditworthiness. Australia’s high level of wealth derives from strong institutional settings and decades of economic reform, which have facilitated the country’s flexible labor and product markets. Australian governments have demonstrated a willingness to implement reforms to sustain economic growth and ensure sustainable public finances, and have a strong track record from managing past economic and financial crises. Institutions are stable and provide checks and balances to power, there is strong respect for the rule of law, and a free flow of information and open public debate of policy issues.

Economic growth remains sound. We estimate headline GDP growth to be around 2.3% in fiscal 2017, and expect it to rise to around its potential growth rate in the following years. Low nominal interest rates, coupled with pent-up underlying demand, have been encouraging growth in dwelling investment for some time, and the negative effect of the declining mining investment pipeline is starting to wane. Significant currency depreciation is spurring services exports, particularly in education and tourism. And while resources investment continues to fall, resource export volumes keep rising as new capacity is brought on line. Household consumption growth has slowed, however, reflecting weak growth in incomes. We expect growth to remain firm during our forecast period, and project real per capita GDP growth to average about 1.0% per year during 2017 to 2020.

OUTLOOK

The outlook has been negative since July 2016. We could lower our ratings within the next two years if we were to lose confidence that the general government fiscal deficit will revert into surplus by the early 2020s. A strong fiscal position is required to offset Australia’s weak external position. It is also needed to allow for a strong buffer to absorb the fiscal consequences if the ongoing boom in the credit and housing market were to abruptly end. While our base case is for a soft landing, our ratings could come under pressure if an undiminished continuation of the unsustainable credit expansion were to continue. We believe the fast and sustained growth in credit and house prices will increase risks to fiscal accounts, real economic growth, and financial stability.

The ratings could stabilize if we were to see a significant and sustained improvement in the medium-term budget outlook, leading to a return to a general government surplus. A stabilization of the ratings would also require a meaningful moderation of the credit and house price boom.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.