Some intense millennial bashing from The Australian’s Grace Collier over the weekend:

Deary me, houses are expensive, are they? Oh snowflakes, cry me a river.

…Want to live in the inner city of Melbourne? There is a studio apartment opposite Flinders Street Station on the market for $169,000. Want a house? Try leafy upper Ferntree Gully, 32km east of the city, on a train line, where modest houses on big blocks can be purchased for under $600,000.

Perhaps you are in Sydney and truly, literally, cannot afford to buy a single thing, not even a one-bedroom dogbox out in Woop Woop. So sad, but too bad. Don’t ask the government to help and don’t agitate for measures that will punish everyone who doesn’t live in Sydney or who does but isn’t as unfortunate as you.

This affordability crisis is the construct of activist groups who have created a social campaign to assist federal Labor. This campaign is being given oxygen by a Sydney-centric media. Now we have commentators calling for national tax arrangements on investments, in place for a century, to be changed — all because precious types are bleating about the price of luxury housing in premium suburbs.

A “crackdown on negative gearing” will make it only harder for ordinary people to create their own wealth.

…Dear little snowflakes, KPMG recently revealed that the poorest 20 per cent of households have enjoyed growth in “investment income” of 8.5 per cent a year across the past decade. Since 2006, the number of low-income households with a second mortgage has doubled.

So, if houses are so unaffordable there is an affordability crisis, why is it that the working poor and people on welfare can afford to buy them? Here’s a tip: if you want advice on how to afford a house, look to the class of people who serve you daily as you go about your privileged existence.

Next time you summon a car to take you home from your favourite new restaurant, ask the person driving. Ask the person painting your nails, the bank teller who serves you, the person who cuts your hair or the person who mows your parent’s lawn. Many of these people will own a house and some will own several.

The article radiates bitterness for priced out youngsters.

Still, I agree that there is no “housing affordability crisis”. It is partly a construct of both sides of politics, the Baby Boomer generation, the media and other vested interests to excuse and confuse what’s really going on.

We don’t have a housing affordability problem, we have a house price bubble, and desperate rent-seeking by everyone in it (including Ms Collier) to keep it inflated.

A bubble is the extrapolation of favourable conditions for an asset class endlessly into the future leading to hysterical bidding and fantastic prices. Ms Collier is an outstanding example of such. No house is too expensive. No buyer beyond praise. No exposure too high. No debt too great. No fool outside of it too stupid.

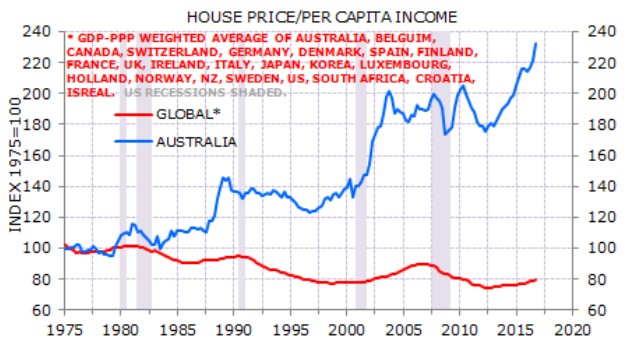

She might want to hose off her personal melt-up for long enough to examine broader circumstances. Prices are extreme:

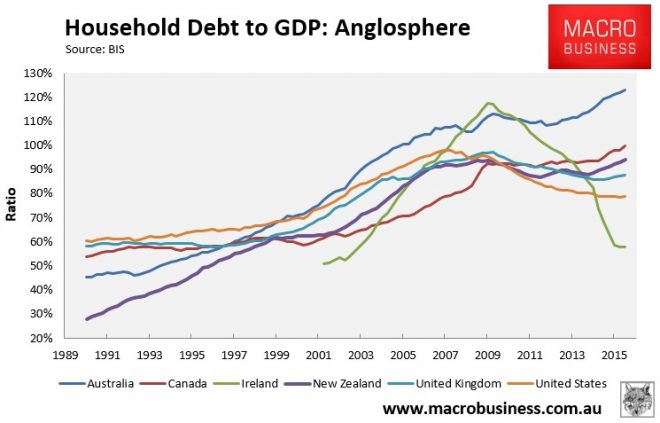

Household debt is extreme:

And with interest rates, fiscal policy and immigration all approaching exhaustion how does Ms Collier think it will all continue on upwards forever?

When the bubble pops it will not become harder for people to buy homes. The amount of proportional deposit required will rise as lending standards reset to something resembling prudent but stable or falling prices will make reaching targets much easier.

Moreover, first home buyers will not be bidding against existing equity positions leveraged by the government handout of negative gearing. Though housing rentiers like Ms Collier will no doubt still be able to count on other welfare like wall-to-wall bank guarantees, RMBS purchases, free money at the RBA etc.