April PMI data suggests the manufacturing recovery is slowing, with worse performance from China and the US. But the fall in the global PMI needs to be seen in context of its recent surge which had seemed an implausible guide to likely growth in the hard output data. We continue to expect a solid year for IP/manufacturing but with growth rates moderating from current levels.

Industry/manufacturing is a key sector for metals demand, and the PMIs are a timely indicator of its health. They do not lead official data but they are available much earlier. April’s manufacturing PMIs are all now out; the equivalent official data will only be released in one to two months’ time.

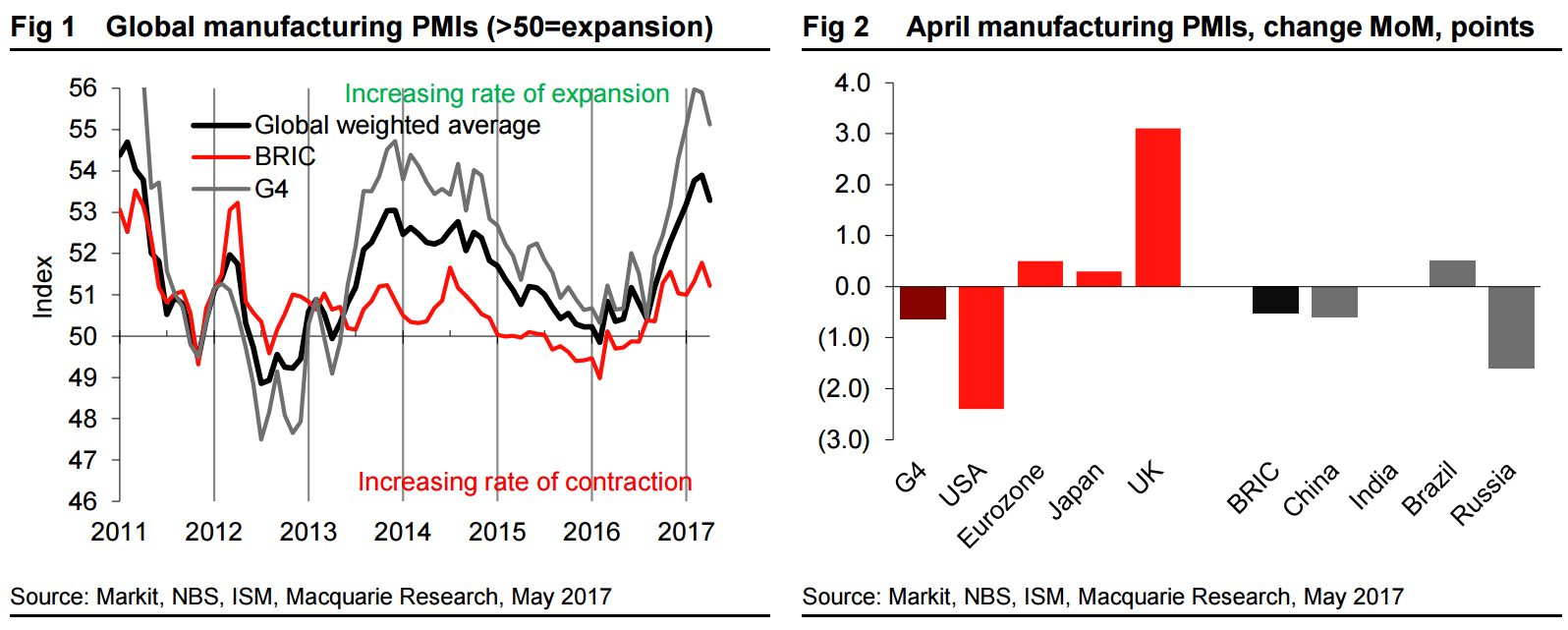

Taken at face value the April release could be a cause for concern. Aggregating the PMIs of 151 countries plus the 19 country Eurozone (weighted by share of global manufacturing output), we calculate globally the manufacturing PMI fell 0.5 points MoM to 53.4, its lowest since January (Fig 1). The biggest decline came in the USA, down nearly 2.5 points, but China also fell back, as did Russia, with the Eurozone and devaluation-assisted UK improving (Fig 2).

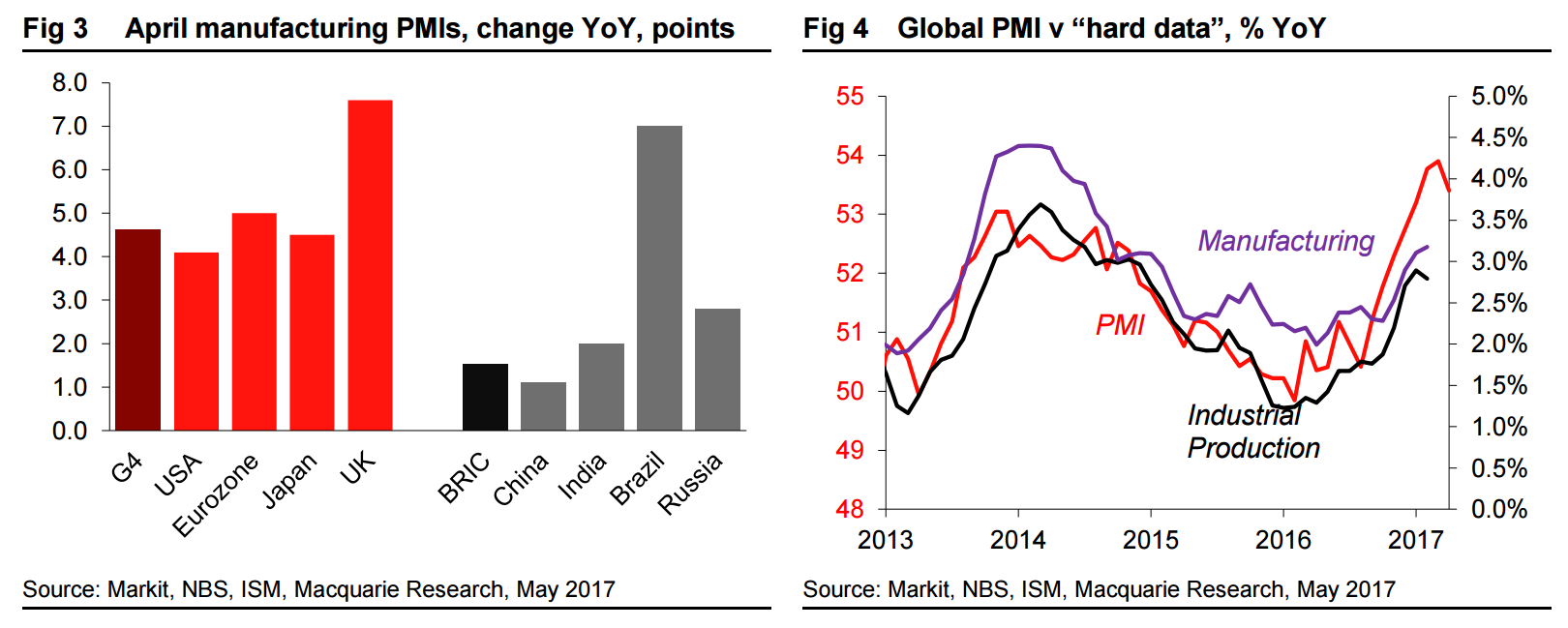

But while we do expect the sector to slow, April’s move must be kept in perspective. All the major country PMIs are far higher than they were a year ago (Fig 3). And a global aggregate of 53.4 still points to a robust expansion in the sector – just below 4% YoY given the relationship shown in Fig 4, from 4.2% on March’s numbers (Fig 4).

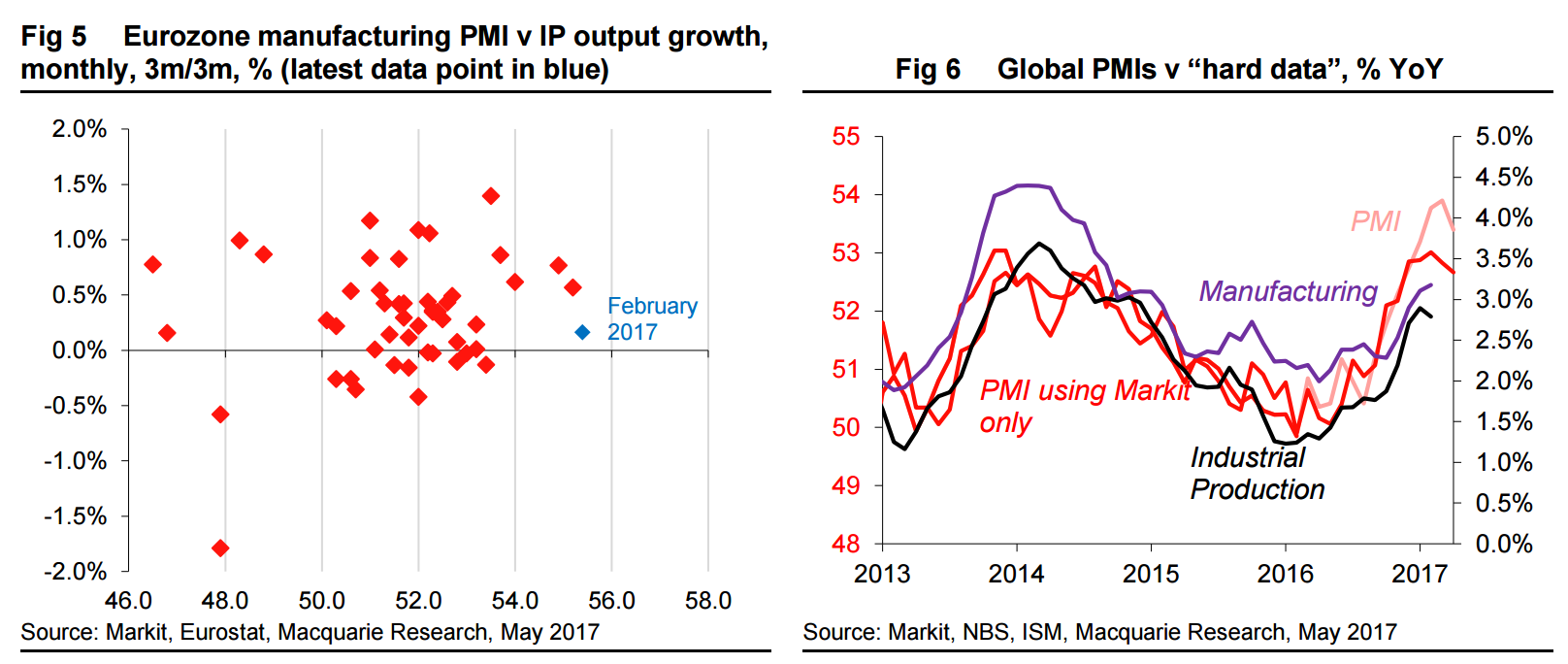

Indeed it is pertinent to note that global industrial production or even manufacturing is not expanding at 4.2% a year, but around 3%. This disparity between “soft” data – surveys – and “hard data” – output, is a widely discussed issue in global macro at the moment. PMIs are not the softest of soft data – they ask about output levels not sentiment – but in many countries/regions, particularly the US and Europe, they have outpaced the underlying government industrial production and manufacturing data (see Fig 5 for the Eurozone PMI v IP growth).

One possibility has always been that the hard data would catch-up with the soft data, and to some extent it has done that. However, we have kept a cautious forecast for IP/manufacturing growth in 2017 as a whole because we saw good reasons to believe the PMIs were overstating growth; for example, they seem to be overly-influenced by strong YoY gains in oil/commodity prices.

On this reading, April’s PMI fall might not signal a slowdown in the sector, or only a slowdown in the sector, but also reflect a more realistic reading of the sector’s underlying health (possibly because the YoY gains in input/output price gains have begun to moderate). Some support for this argument is shown by the darker red line in Fig 6, which is our global manufacturing PMI but reworked using Markit’s data for China and the US, rather than the NBS and ISM data we typically use. This adjusted total is not too different but it didn’t rise as high as our normal series at yearend and has turned down earlier and more gradually. Historically we have found a better ‘fit’ from the NBS and ISM PMIs, but not reliably so and this time the Markit data seems to have given a lead.

To conclude it looks like the sector is slowing, but the fall in the April’s PMIs almost certainly overstates its speed and severity. Overall the data remain consistent with our view this year will be a good one for industrial production – up 2.5% YoY – but not a spectacular one, with YoY growth rates moderating as the year progresses. Of course the PMIs could retrace further, and begin to point to a more severe downturn. But at present we see no evidence for that.

Hmmm, well, you should look at the Chinese credit impulse. My questions at this point are the following:

will the Chinese slowdown be sufficient to derail global markets hanging on a US fiscal hand-off?

given the delay in said hand-off, there’s a credibility gap in global growth over H2. Will the Fed be forced to slow as a result?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.