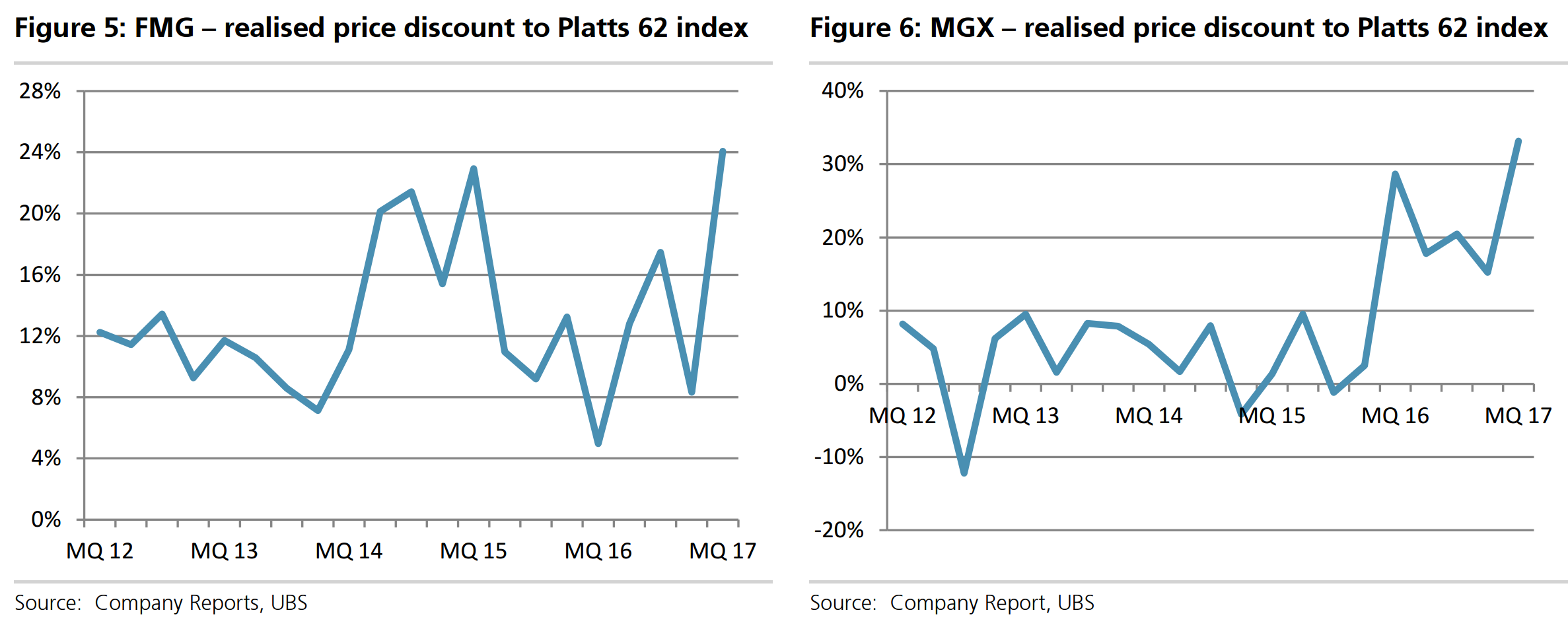

Readers will recall I’ve been musing recently about FMG’s break even is now on a 62% basis given its tragic 25% discounting. I mulled a lift to about $35 but no, from UBS:

Rising unit costs evident in the March 2017 quarter

The iron ore producers globally have reported Q1 17 results and with that some have updated their cash cost positions. On the whole producers reported higher costs sequentially driven by a weaker US$, rising strip ratios and consumable costs and lower volumes driven principally by seasonality (Q1 impacted by weather), although for the majors volume was flat y/y, but down >10% sequentially. Despite the rise in costs, the majors are still comfortably ensconced in the low to mid-teens on the cost curve (C1).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.