By Gareth Aird, Senior Economist at CBA

Key Points:

- Retail trade growth is soft primarily because demand for discretionary goods has slowed on weak household income growth.

- The slowdown in sales growth has been broad-based across Australia’s states and retail-related employment has declined.

- The fall in retail trade volumes growth suggests that disinflation in the retail sector is being driven by more than just competition.

Overview

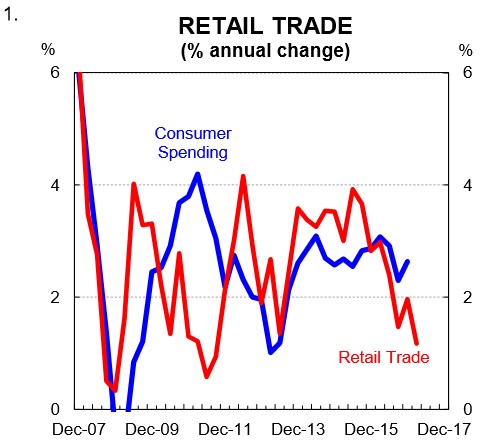

Retail trade growth in Australia has softened over the past two years. The latest figures indicate that retail trade volumes lifted by just 0.1% in QI 2017 while nominal sales rose by a lacklustre 0.3%. These numbers are weak. The news hasn’t been as gloomy for the consumer sector more generally (chart 1). But the evidence indicates that the Australian retail sector, as a collective, is doing it tough. There are a number of factors that have conspired against the retail sector in recent years. Some of those are related to the macroeconomic landscape while others are specific to the retail sector.

In this short note we take a look at what’s going on in the Australian retail industry. Our aim is to better understand the structural and cyclical forces at work that are weighing on sales growth.

Is it a price or volumes story?

Inflation in the retail sector is low. In the year to QI 2017, the retail implicit price deflator is estimated to have grown by 1.5% (below CPI inflation which was 2.1% over the same period). Put simply, price rises in the retail sector have been less than price increases for the consumer basket more generally. The RBA did some work on this last year and found that competition spurred by new foreign retailers has put downward pressure on inflation in the retail space1. We agree to an extent. But would add that it’s also slowing demand for retail goods that has put downward pressure on the rate of inflation and not just competition.

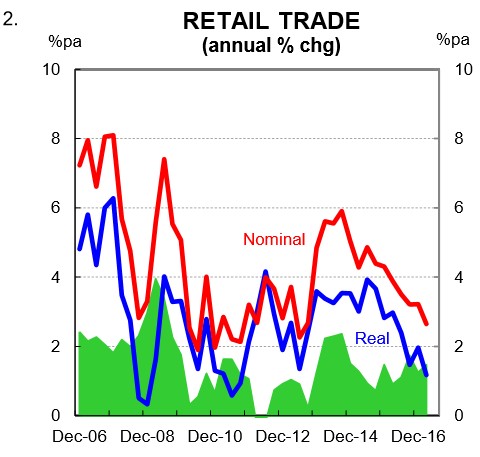

How do we know this? If the weakness in retail sales growth was purely reflecting price wars due to competition we would expect to see the gap between nominal retail sales and volumes compress. Instead, the spread has been relatively stable at around 1½% over the past two years (chart 2). In fact, the spread is higher now than it was during the mining investment boom when the AUD was elevated (import costs were falling). The simple reality is that despite increased competition in the retail sector, which should support sales volumes, real retail trade growth has softened. The evidence indicates that households have devoted a greater proportion of their wallet to spending on health, utilities and education in recent years. Consumers have a fine amount of disposable income and even with the assistance of a falling savings rate, record low wages growth has weighed significantly on the discretionary parts of retail trade.

What’s included in the retail survey?

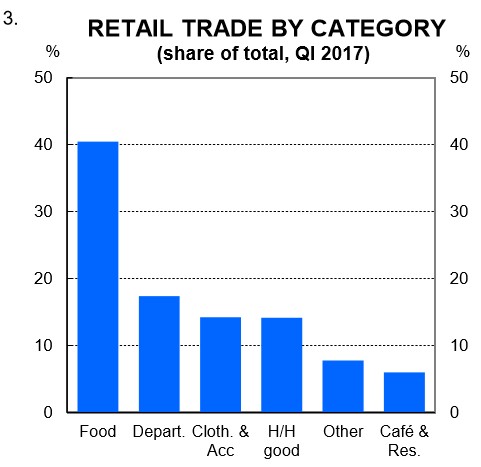

The starting point to unpacking retail trade weakness is to look at what’s actually included in the survey. Broadly speaking, the retail trade survey comprises six major groups: (i) food; (ii) household goods; (iii) clothing and footwear; (iv) department stores; (v) cafes & restaurants; and (vi) other. Their relative shares are shown in chart 3. Unlike in the US, motor vehicles are not includes in the retail trade survey.

Food retailing & eating out

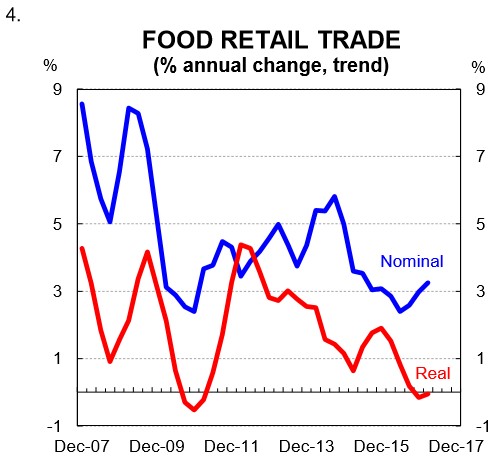

Food retailing, worth around 40% of total retail sales, comprises supermarket and grocery stores, alcohol and other specialised food retailing. It’s the single biggest component of retail trade. In the year to QI 2017, food retailing volumes were down by 0.1% (trend). But nominal sales growth had lifted to 3.3% (chart 4). The spread between nominal and real sales growth has actually widened which suggests that the much talked about ‘price wars’ occurring between grocery stores may be overdone. In fact, it looks like the big supermarket chains still maintain plenty of pricing power given the spread between nominal and real sales has increased. Inflation in the food retailing space was running at 3.4%pa in QI 2017.

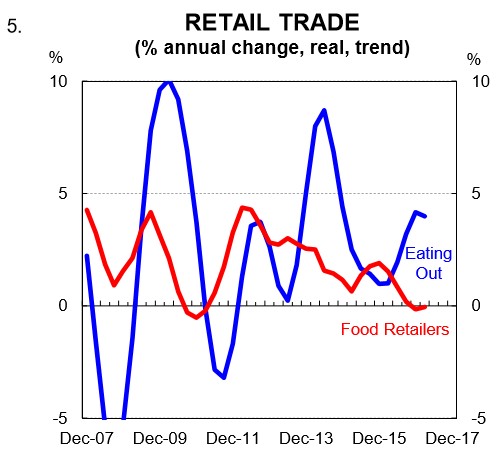

That said, it’s unusual to see food volumes decline through the year given strong population growth in Australia. The answer, it seems, is found in looking at what’s been happening in the eating out space. Nominal spending at cafes and restaurants was running at 5.2% through the year to QI (trend) while volumes were 4.0% higher. Some of the lift in spending eating out reflects a pickup in tourism. Notwithstanding, it does look like there’s been some substitution going on between supermarket spending and eating out (chart 5).

Verdict: The weakness in retail sales growth is not down to total spending on food (eating out + supermarket/grocery stores). The answer lies elsewhere.

Department stores, household goods, and clothing and soft goods.

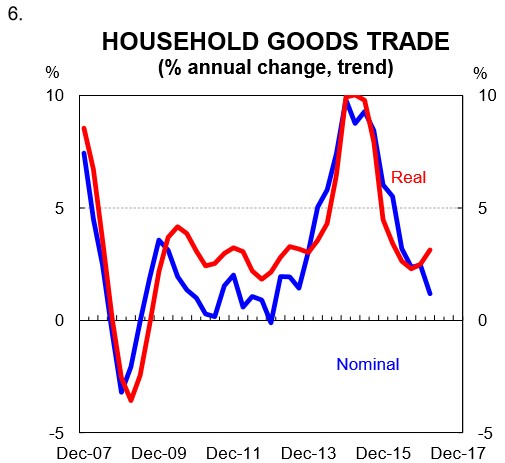

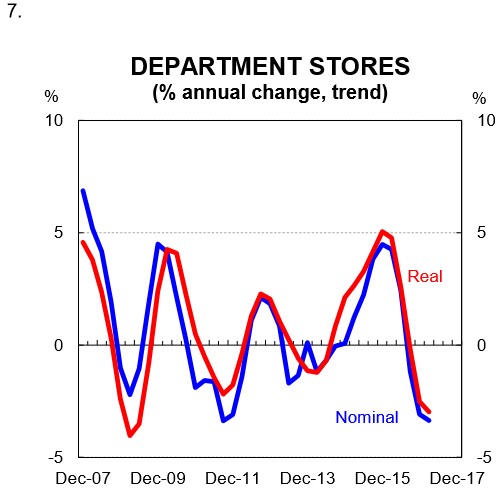

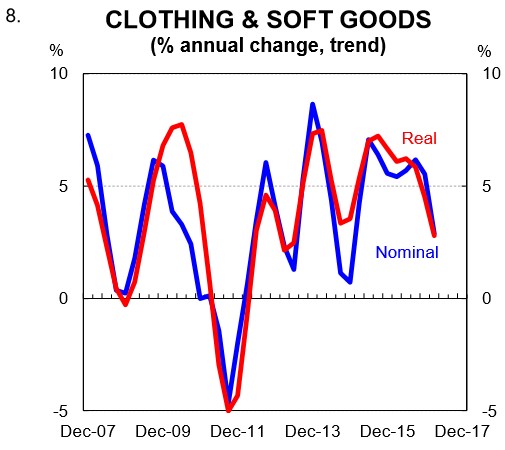

There has been a broad-based slowdown in both real and nominal retail trade growth on household goods, clothing and at department stores (charts 6 to 8). Indeed, sales in department stores have been falling. There is almost no inflation in these components of retail trade. In fact, there is deflation in department stores. Some of this can be put down to the increased competition that retailers face from online vendors. But in our view, the single biggest factor weighing on retail trade growth in these areas is very weak wages growth which is supressing demand growth.

There are a significant number of retailers operating in these spaces that have recently entered voluntary administration. Herringbone, Marcs, Pumpkin Patch, David Lawrence, Rhodes and Beckett, for example, are all household names that have recently fallen on their sword.

Verdict: Soft total retail trade growth is largely down to a lack of spending growth on consumer durables and clothing.

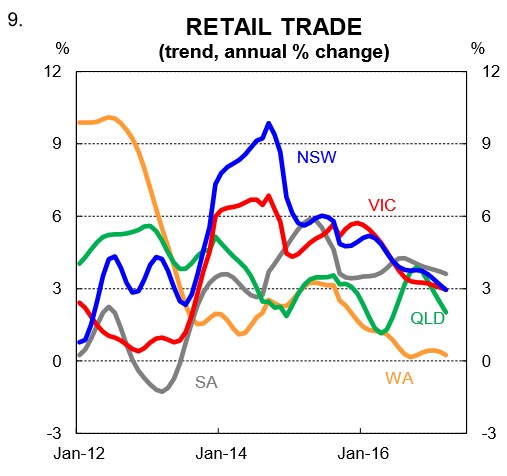

States

Looking at retail growth on a state basis shows that sales growth is soft in all jurisdictions. Retail trade growth has been weak in QLD and WA for several years. But national sales growth had been buoyant because of decent growth in NSW and Vic. Over the past two years, however, retail trade growth has slowed in Australia’s two biggest states which has dragged the national rate lower (chart 9). This has occurred despite dwelling price growth continuing to run hot in Sydney and Melbourne which would have traditionally supported household consumption growth and indeed consumer sentiment.

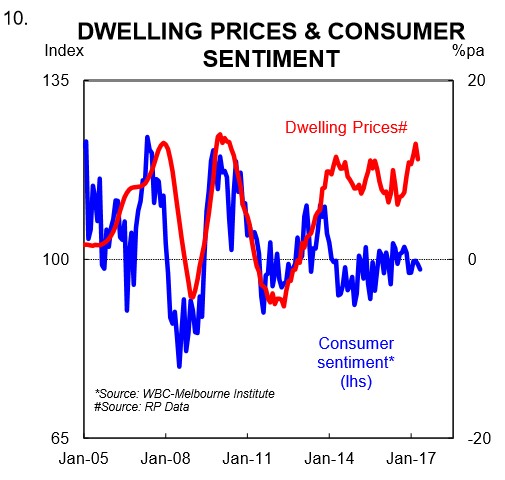

As we covered back in April, between 2005 and mid-2013 there was a very good correlation between dwelling prices and sentiment (chart 10). Price rises and falls tended to go hand in hand with consumer optimism and pessimism which had an impact on household consumption. But that relationship has since broken down. Since late-2013 the stunning rise in property prices has failed to generate any euphoria amongst consumers which means the boost to spending from higher asset prices has also eased. Of course there are a lot of things that go into the melting pot that determines how households feel. But at the risk of oversimplifying things, it looks like strongly rising dwelling prices have done little to generate optimism amongst consumers. We suspect that is because the lift in dwelling prices has not been driven by higher wages growth but rather by a lift in leverage. And in our view, income matters far more to households than optically strengthened balance sheets courtesy of rising dwelling prices.

Employment

Retail trade weakness is showing up in the employment data by industry. In the year to February 2017 (latest available) the number of people employed in the retail sector is reported to have fallen by 59.2k. This is a sizeable decline and highlights the impact that a soft retail sector has on the labour market. The news is particularly sobering for youth unemployment given retail has a higher percentage of its workforce under the age of 25 when compared with most other sectors.

Outlook

In our view, the slow rise in prominence of online retailers is structural and therefore it is here to stay. This means that the Australia retail sector will face a permanent headwind. It’s a win for consumers, however, who are able to access a broader range of consumer goods at lower prices via the web.

With monetary policy stimulus close to being exhausted, the necessary requirements to generate a lift in retail trade growth are: (i) higher wages and household income growth; and/or (ii) income tax cuts. With the latter already having been ruled out, only a lift in wages growth will drive an increase in retail sales growth. Given the significant amount of slack in the labour market we don’t see that happening in 2017 and we therefore conclude that the retail trade sector, in particular the discretionary parts of retail trade, will continue to be under pressure throughout the year.