BHP has received a proposal from activist shareholder, Elliott Associates, to restructure the company. The core parts of Elliott’s “Value Unlock Plan” are 1) Collapsing the DLC structure, 2) Demerging and listing the Petroleum business on the NYSE, and 3) Returning cash to shareholders by increasing off-market buy-backs and unlocking the large franking credit balance.

Impact

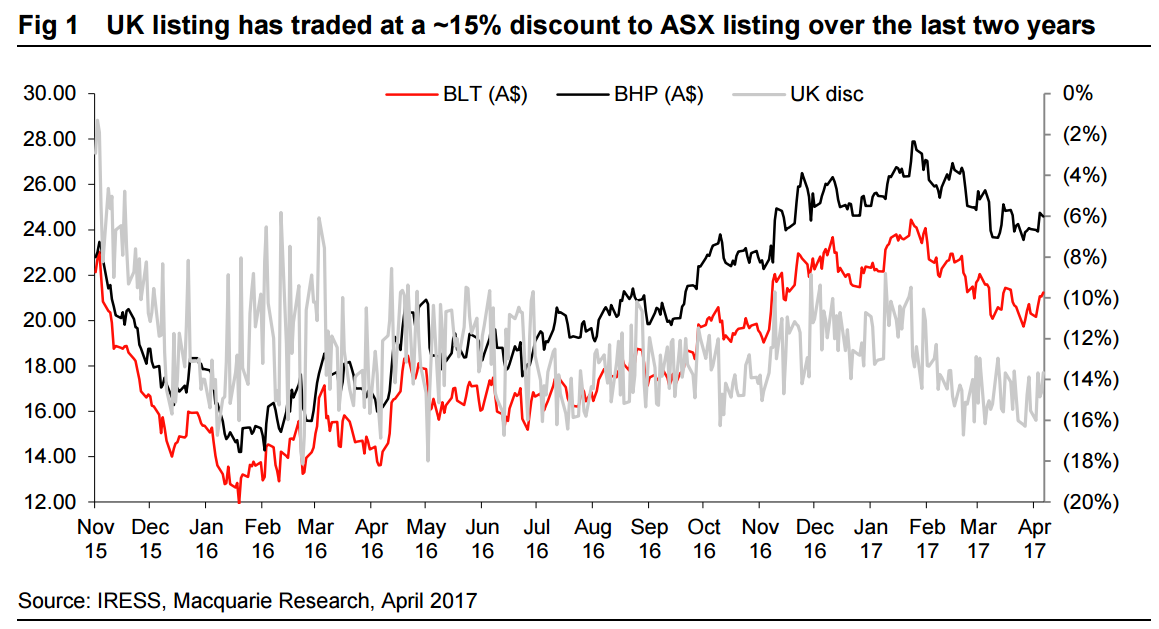

Collapsing the DLC structure: On the surface collapsing the DLC structure makes some sense to us, and has been speculated in the past. BHP notes it already has the DLC structure under review, and it has yet to identify sufficient benefits to outweigh the costs. BHP also believes the proposal would require Australian Foreign Investment Review Board approval. Our analysis suggests that the differences in market P/E multiples between the FTSE100 and ASX200 is the key driver behind the DLC spread, not franking credits. As a result we are concerned that there could be significant leakage of the premium currently enjoyed by the ASX listing.

De-merging the US Petroleum assets: De-merging the US Petroleum assets (Gulf of Mexico and Shale) also makes sense to us on the surface, however while the implied multiple of US Petroleum peers of 7-8x EV/Ebitda is a premium to BHP’s current multiples, we believe ~80% of the US$20bn in net debt could be attributable to these assets given recent acquisition expenditures. The level of net debt ascribed is critical to the value adding proposition.

Returning additional cash to shareholders: The Elliott “Value Unlock Plan” is largely focused on creating a structure that enables BHP to return more franking credits to shareholders via off-market buy-backs of the ASX shareholding at a 14% discount. We agree that trying to unlock the ~US$10bn in franking credits makes sense but we do not expect it to occur under this proposed structure.

Earnings and target price revision

No change.

Price catalyst

12-month price target: A$30.00 based on a NPV – 8.0x EV/Ebitda blend methodology.

Catalyst: BHP is set to release its 3QFY17 production result on the 26 April. An update on Samarco litigation is also expected during FY17.

Action and recommendation

Maintain Outperform: We believe the “Value Unlock Plan” raises some interesting questions worthy of considering. Unlocking franking credits remains a long-term goal for BHP, however management has indicated that the costs of this structure outweigh the benefits. There is a real risk in our view that a combined single listed entity could trade towards the UK multiples rather than maintain the Australian multiples. The key question in our mind remains does the UK stock trade at a discount or the Australian stock at a premium. A de-merger of the US Petroleum assets could unlock value but is highly dependent on the level of debt ascribed to the business.

Why would it give up the Australian stupidity premium?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.