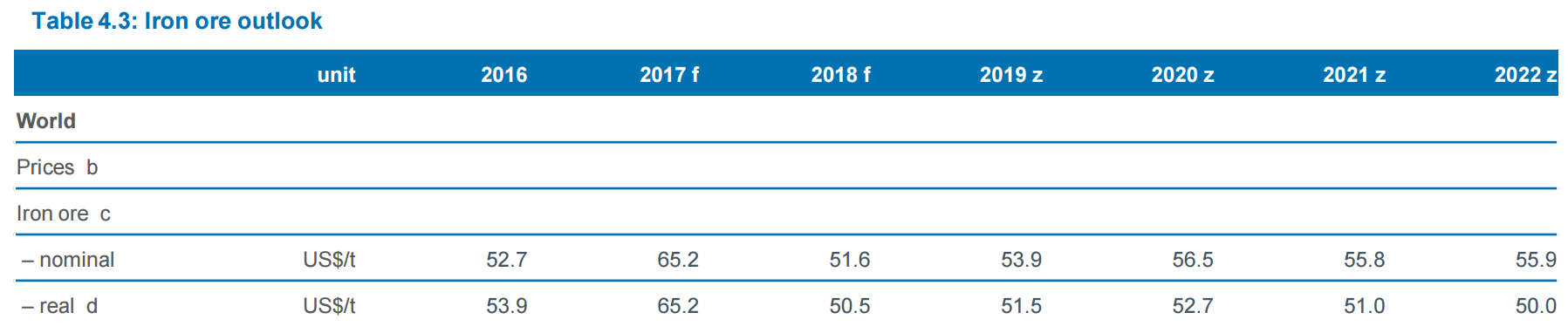

The Office of the Chief Economist, formerly BREE, is out with its quarterly price updates for dirt and, although it is improved, it remains too bullish. Iron ore is seen steadily falling back:

The 2017 forecast is solid. 2018 is reasonable if too high for me. But beyond that it’s all far too bullish. $50 will not displace any iron ore anywhere any more. So if you’re base case is for Chinese steel output to fall then you need to be sub-$50 for an extended period. I would take $10-15 off all of those prices beyond next year.

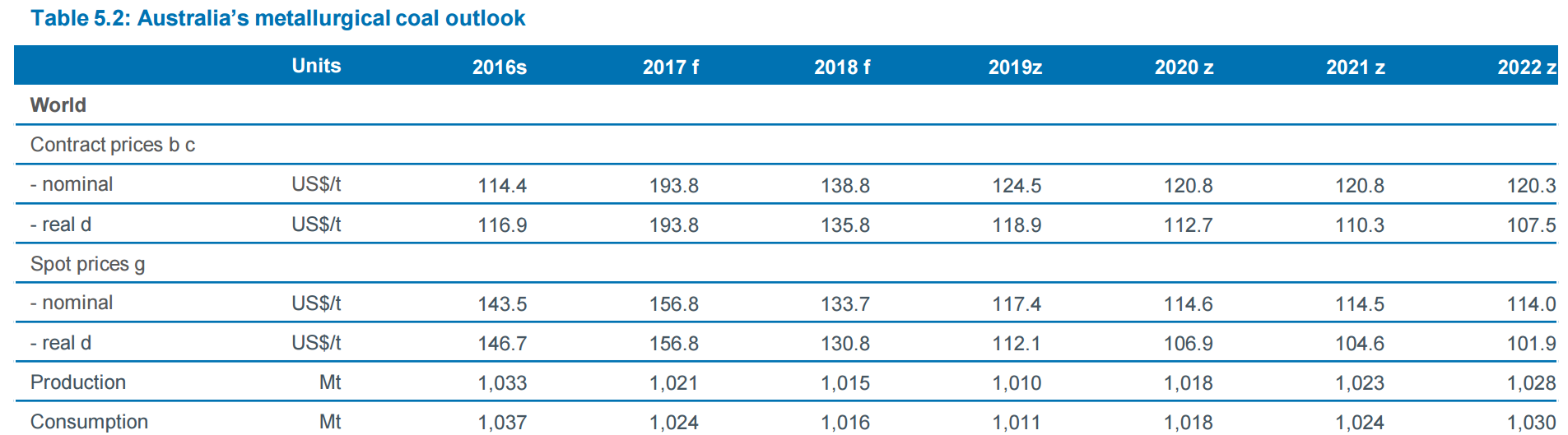

Coking coal is worse:

I expect to see coking coal back at $100 by year end and to stay there.

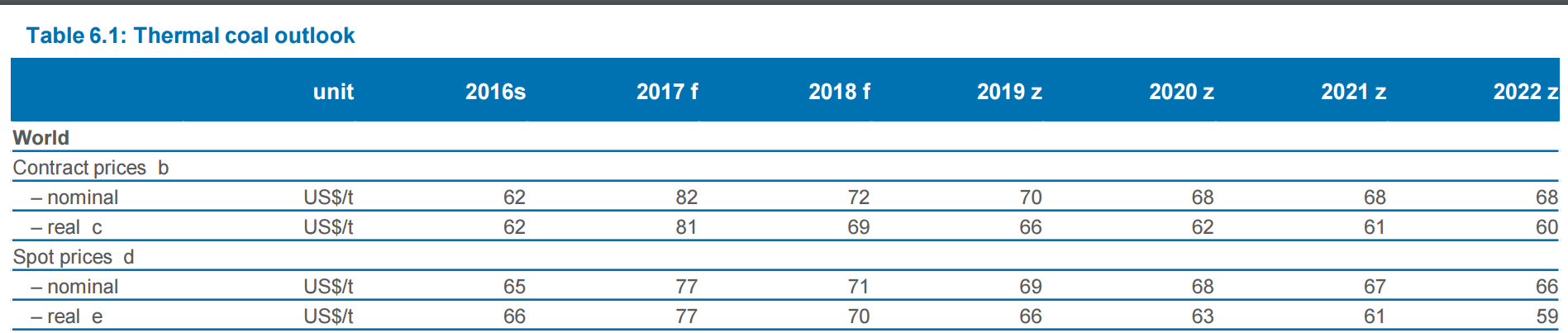

Thermal coal is pretty reasonable:

I would shave those prices a little but they’re close enough.

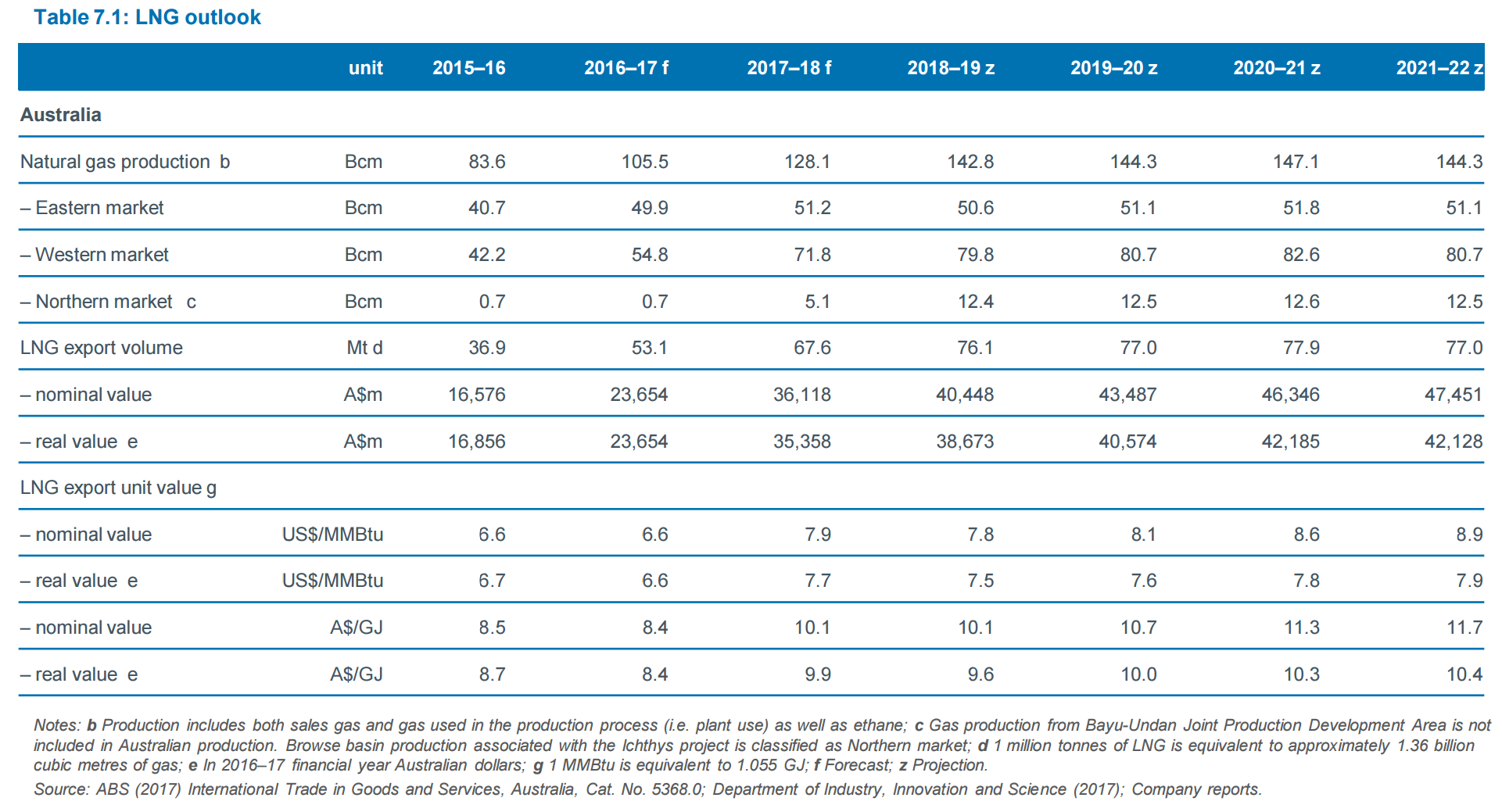

LNG is too bullish:

That is the equivalent of a steady march north in Brent oil to $65 in 2021. That is a little too bullish for me give the shale revolution but more importantly it does not account for any large scale switch from contract prices to spot which I see as inevitable.

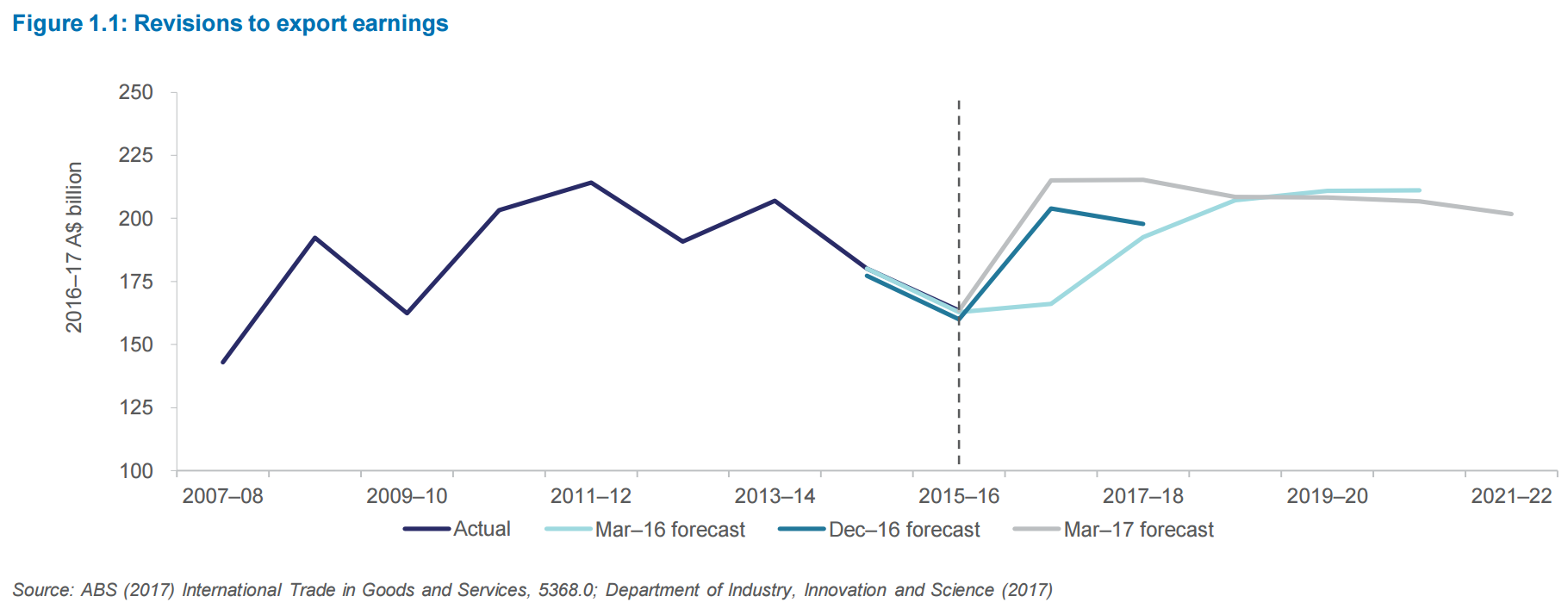

The upshot for dirt exports is a lifted outlook:

My own view, sadly, is a dive back downwards towards 150bn again as Chinese reform returns before a long grind out of the hole into the 2020s.