“For twenty years we have had a logjam of costly regulation, poor planning decisions and excessive taxation across all levels of government. This has driven up construction costs, impeded supply, and resulted in the dramatic increase in house prices in our major cities.

“Australia is benefiting from population growth, record low interest rates and relative economic prosperity, but getting so many other policy settings wrong has made affordability worse.

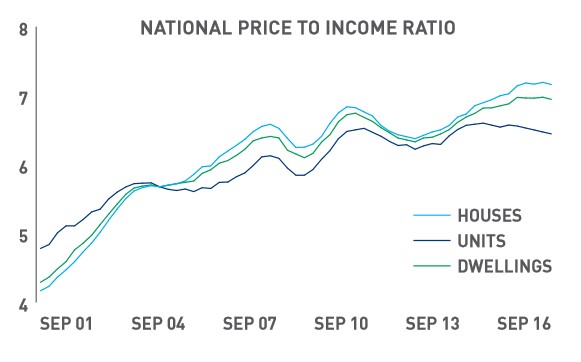

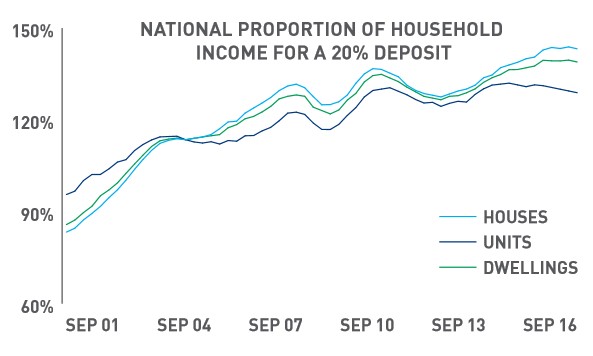

“Fifteen years ago, average dwelling prices were 4.3 times average wages, now it is 6.9 times average wages. Likewise, in 2001, it took 86% of an average householder’s annual income to pay the deposit on an average house. By 2016, this had risen to 139%.

“This affordability cauldron has taken years to develop, and it will take concerted effort over many years to unwind.

“Fundamentally we need policy settings that help Australia build enough houses to match our growing and changing population.

“Our plan seeks to support housing construction, broaden housing choice, reduce unnecessary construction costs, incentivise the states to undertake planning reform, induce institutional investment in new rental stock, and help first home buyers bridge the deposit gap…

“We have to reduce transaction costs which lock people into homes that don’t suit them and are a big drag on the economy. In a city like Sydney, typical stamp duty bills exceed $70,000.

“As well, pensioners are discouraged from downsizing because of the way the pension assets test is configured. Some small changes to the downsizing rules could see tens of thousands of family homes enter the market…

The Property Council’s Plan “Fixing Housing Affordability” identifies 10 planks to tackling rising house prices:

Advertisement

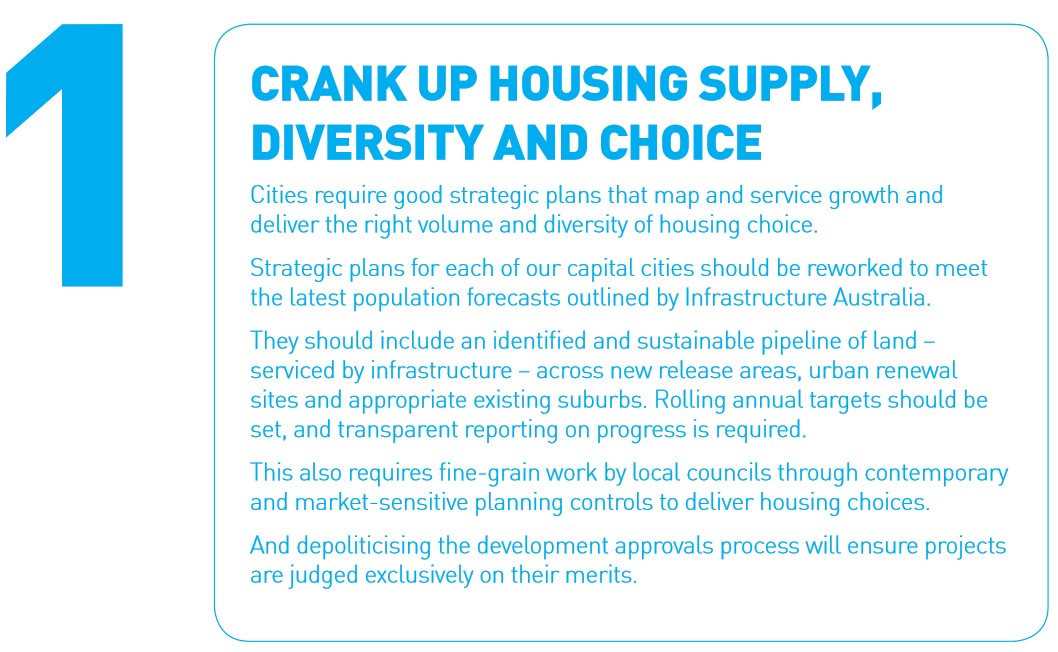

Crank up housing supply, diversity and choice

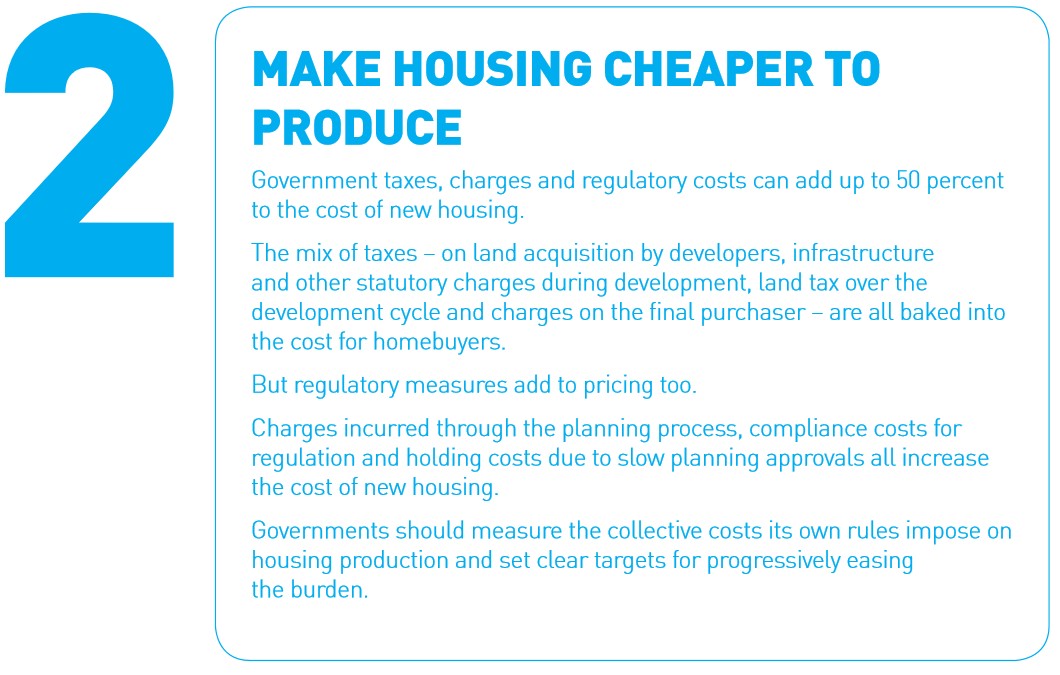

Make housing cheaper to produce

Incentives to spur reform

Bridge the deposit gap – Keystart low deposit home loans

Remove barriers to downsizing

Don’t play with negative gearing

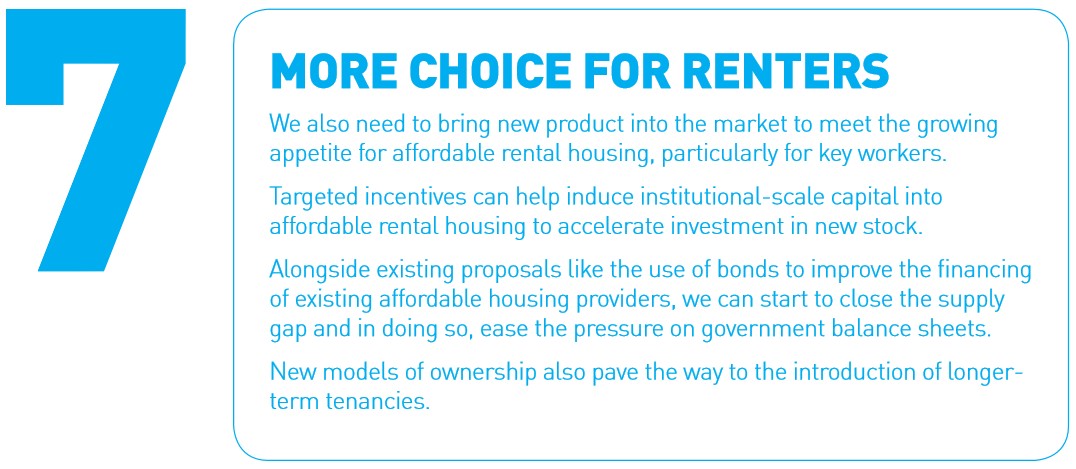

Institutional investment in ‘build to rent’ housing to give more choice for renters

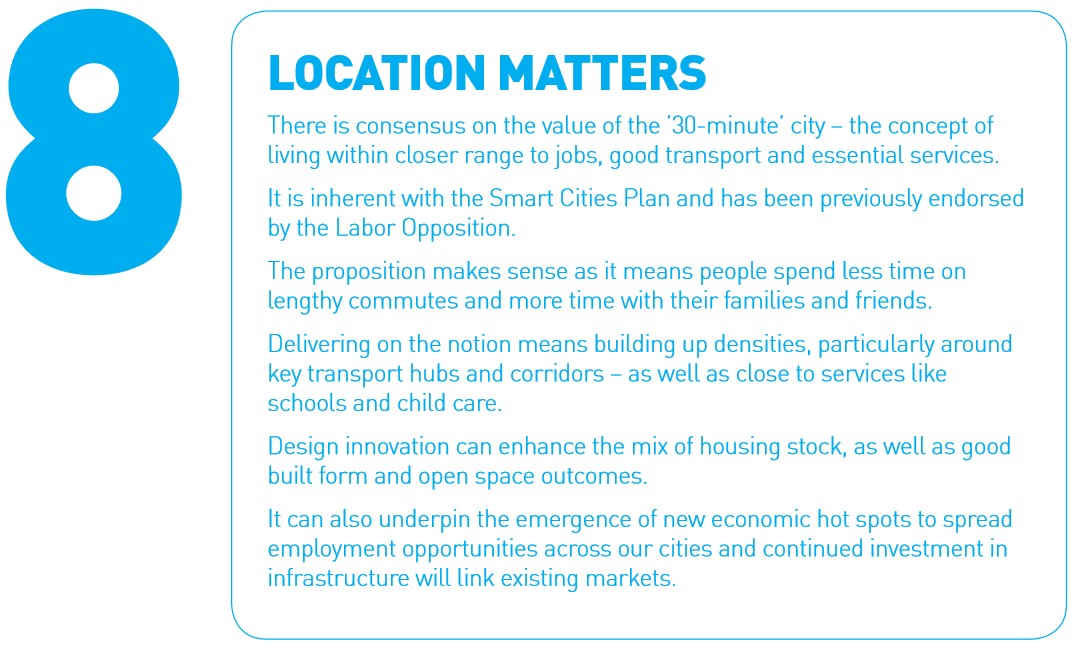

Location matters – densities around transport hubs and corridors

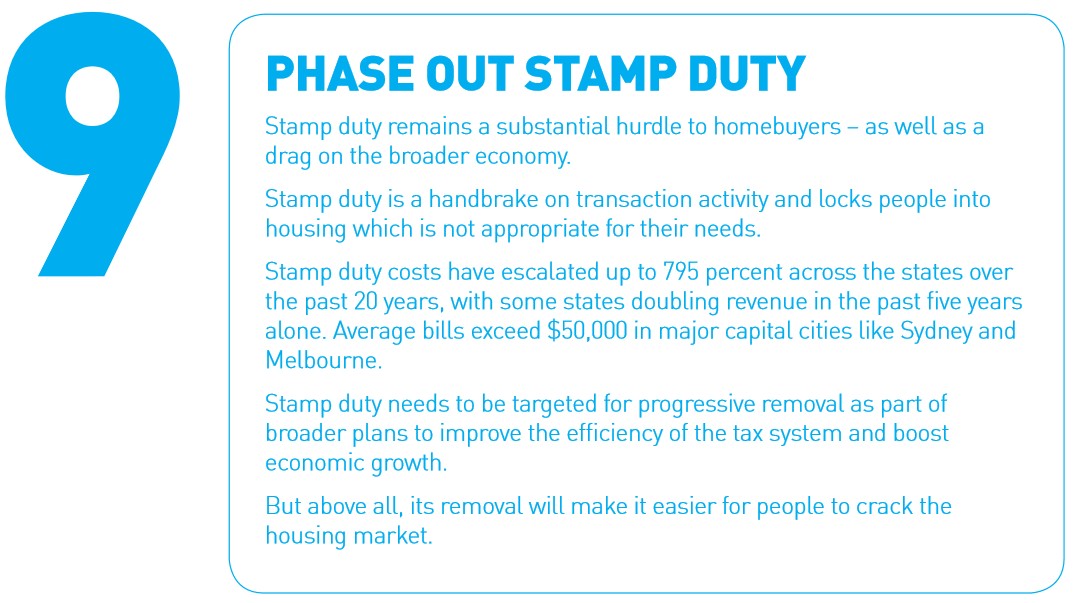

Phase out stamp duty

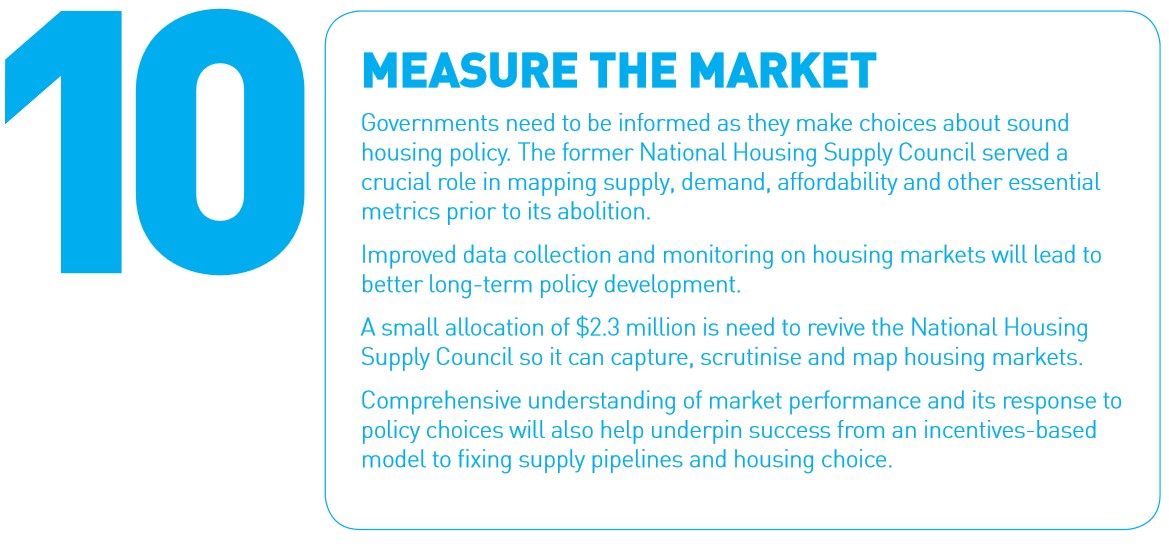

Re-establish the National Housing Supply Council

Now, let’s evaluate each plank of the PCA’s plan.

MB supports this plank. Australia’s planning system is clearly busted, as evident by the rapid escalation of lot prices amid the collapse in lot sales (see yesterday’s post). Making the supply-side of the housing market more responsive to demand is a policy no-brainer.

Advertisement

MB supports this plank in principle, for the same reasons as above.

Advertisement

MB supports this plank and has spent several years lobbying the federal government to provide incentive payments to the states in return for freeing-up land-use and planning (for example, see here and here).

MB strongly opposes this plank. Expanding shared equity schemes would increase housing demand and therefore prices (other things equal), thus becoming self-defeating from a housing affordability perspective. This is because:

Advertisement

A new pool of lower income buyers that would not qualify for a conventional mortgage would suddenly be able to enter the market and bid up prices; and

Buyers that do already qualify for, say, a $400,000 conventional mortgage may choose to take advantage of a shared equity scheme so that they can purchase a more expensive home than they could otherwise afford.

Thus, shared equity arrangements would further fuel price rises in the housing market, resulting in further reductions in housing affordability.

Advertisement

MB opposes this plan. Allowing downsizing retirees to avoid paying stamp duty and pocketing some of the windfall from their sale without affecting their access to the Aged Pension would have a deleterious impact on the Budget. This means younger people’s taxes would need to rise in order to pay for the bloated entitlements of those who had the good fortune of purchasing their homes cheaply before they skyrocketed in value, to the detriment of their children and grandchildren, who must now support them in old age.

Genuine and equitable budgetary reform is about sharing the burden of adjustment. However, by creating a special class of citizens exempted from bearing any pain – i.e. home owning retirees – the PCA’s plan would effectively shift the burden of repairing the Budget to the younger generations.

The PCA should instead advocate:

Advertisement

Including one’s principal place of residence in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2020), thus allowing current retirees and prospective retirees adequate time to make arrangements.

Raising the overall pension asset test threshold as well as the base rate.

Extending the existing state sponsored reverse mortgage scheme, the Pension Loans Scheme, to all people of retirement age so that asset (house) rich retirees can continue to receive a regular income stream in exchange for a HECS-style liability that is recoverable from the person’s estate upon death, or upon sale of the person’s home (whichever comes first).

Under such a plan, asset rich pensioners choosing to remain in place could continue to receive an income stream as they do now under the Aged Pension, but with less drain on the Budget and on younger taxpayers. But they would similarly be incentivised to move as the family home would no longer be viewed as a tax free shelter. Poorer ‘houseless’ pensioners would also be made better-off via the combination of a higher asset test threshold and a higher pension base rate.

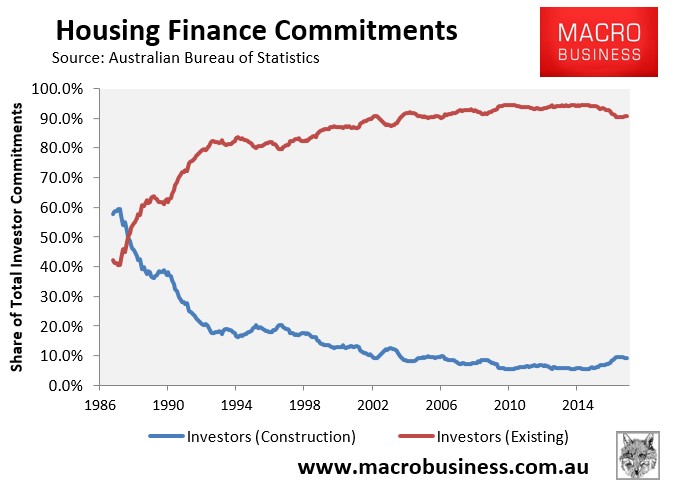

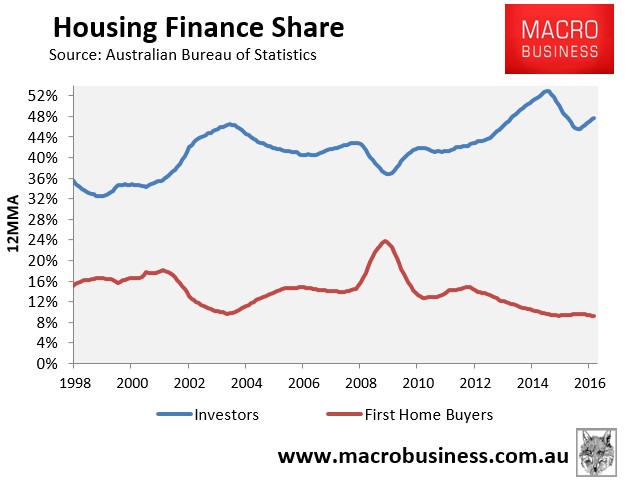

MB strongly disagrees with the PCA. ABS Housing Finance data clearly shows that property investors overwhelmingly purchase established dwellings, hence they are not adding to supply and are merely turning a home for sale into a home for let:

Advertisement

The ABS data also shows clearly that investors are crowding-out first home buyers:

Advertisement

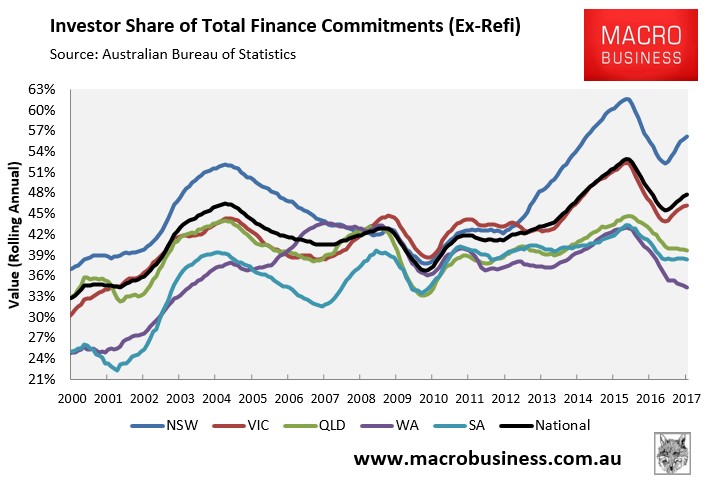

And that investors are driving much of the demand (and price rises) in Sydney and Melbourne, where affordability concerns are the most pressing:

Advertisement

MB supports this plank and believes that some of the funds saved by curbing negative gearing and the CGT discount should be used to boost affordable rentals.

MB supports this plank in principle. However, existing roads, trains, trams, buses, schools and hospitals in the major cities have already been crush-loaded by mass immigration. Further densifying the inner cities to squeeze in tens of thousands of immigrants every year is only going to make these issues worse.

Advertisement

MB supports this plank in principle. However, the revenue lost from abolishing stamp duty must be replaced by something. The logical choice is to replace stamp duties with a broad-based land tax, subject to transitional measures that enable retirees to ‘age in place’ by deferring their land tax bill until after death or sale of the property. Such a policy would not only incentivise both buyers and sellers to move to homes that better suit their needs, but would also significantly improve tax efficiency as well as equity.

Does the PCA support swapping stamp duties for land taxes?

Advertisement

MB supports this plank. Better data is needed around housing supply and housing needs.

While the PCA has made some good policy suggestions, it is also clear that it is concerned first and foremost with lining its own pockets rather than comprehensively addressing housing affordability.

Advertisement

It has offered nothing of value on demand-side reform, strongly opposing changes to negative gearing and the CGT discount, while also calling for assistance to get first home buyers into the market quicker, which would be self-defeating from an affordability perspective.

It is also curious that the PCA acknowledges that strong population growth has driven housing demand, but has omitted to recommend reducing Australia’s migrant intake to sensible and sustainable levels to alleviate pressures on both housing and infrastructure in the big cities.

In short, the PCA’s affordability plan reeks of self-interest.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.