Via the AFR:

Australia’s housing market may be at its peak in this cycle, according to some experts, and investors might be wondering whether they should look for alternative places to put their money.

With four of the top twenty Australian companies trading at discounts to their long-run averages, the top tier of the stockmarket might be a good place to start.

BHP Billiton, Rio Tinto, Telstra and Wesfarmers are the only stocks in the ASX20 trading below their long-run price-earnings multiples.

Goldman Sachs head of portfolio strategy Matthew Ross said on Monday that resource stocks were potentially offering the best value for investors, with the big four banks “mildly expensive” compared with an historical basis and many industrial stocks in the broader ASX200 trading at multiples of more than 20 per cent over their long-run averages over the past 10 years.

Goldman are pushing a really crazy idea here:

They put the recent selloff down to bearishness over the global outlook. Stalled policy stimulus in the U.S., tightening in China’s money markets, property curbs and a crackdown on off-balance-sheet lending — plus the French election and North Korea tensions — have hurt global risk sentiment, the analysts said, highlighting the correlation between iron ore, copper and 10-year Treasury yields.

“Although downside risks clearly remain elevated, our base case is that these risks will not materialize in a manner bearish for the markets,” Layton and his colleagues wrote. “While the market has been focusing on downside risks to Chinese and global growth – we highlight a major upside risk to metals demand coming from the Chinese property market.”

The analysts said they remain “constructive” on the outlook for copper fundamentals and expect refined copper supply growth to slow sharply. A lack of technical support is a very near-term downside risk, but strength in Chinese property and related sectors including consumer appliances should boost the metal, they said. Goldman is also bullish on aluminum due to supply-side reforms.

While the market has been “particularly concerned about the unwind in Chinese steel and iron ore prices,” the Goldman analysts said rebar margins remain solid. The selloff in steel is largely due to a higher level of supply and weak export growth, they said.

Goldman said 10-year Treasury yields indicate the recovery in metals could endure. The yield, which has moved with iron ore and copper prices since Donald Trump’s election in November, should rise to 2.65 percent by June, the note said.

While Goldman sees Chinese economic growth slackening this year, metal prices probably won’t be affected because supply will slow over the next three to six months, the analysts said. There has also been a recent pullback in copper net speculative positioning, suggesting that some slowdown in Chinese manufacturing activity is already priced in.

Note to self, sell Goldman. The only thing that is taking down iron ore, and perhaps to a lesser extent base metals, is Chinese tightening. It has nothing to do with Trump or North Korea, the French election or the frozen pie in my fridge.

Goldman has an overall view of the global economy as powering into reflation, which has it predicting loony numbers of rate hikes everywhere, not least Australia, and global commodities strength appears to be a part of that.

But the iron ore position is terrible. All that matters to it is China where the inventory glut is huge, the supply is flowing, demand is already missing high hopes and the economy is going to slow into H2.

Buying big mining now is bonkers. They’ve barely corrected since the iron ore crash started but will once the price sinks below $60 and consensus.

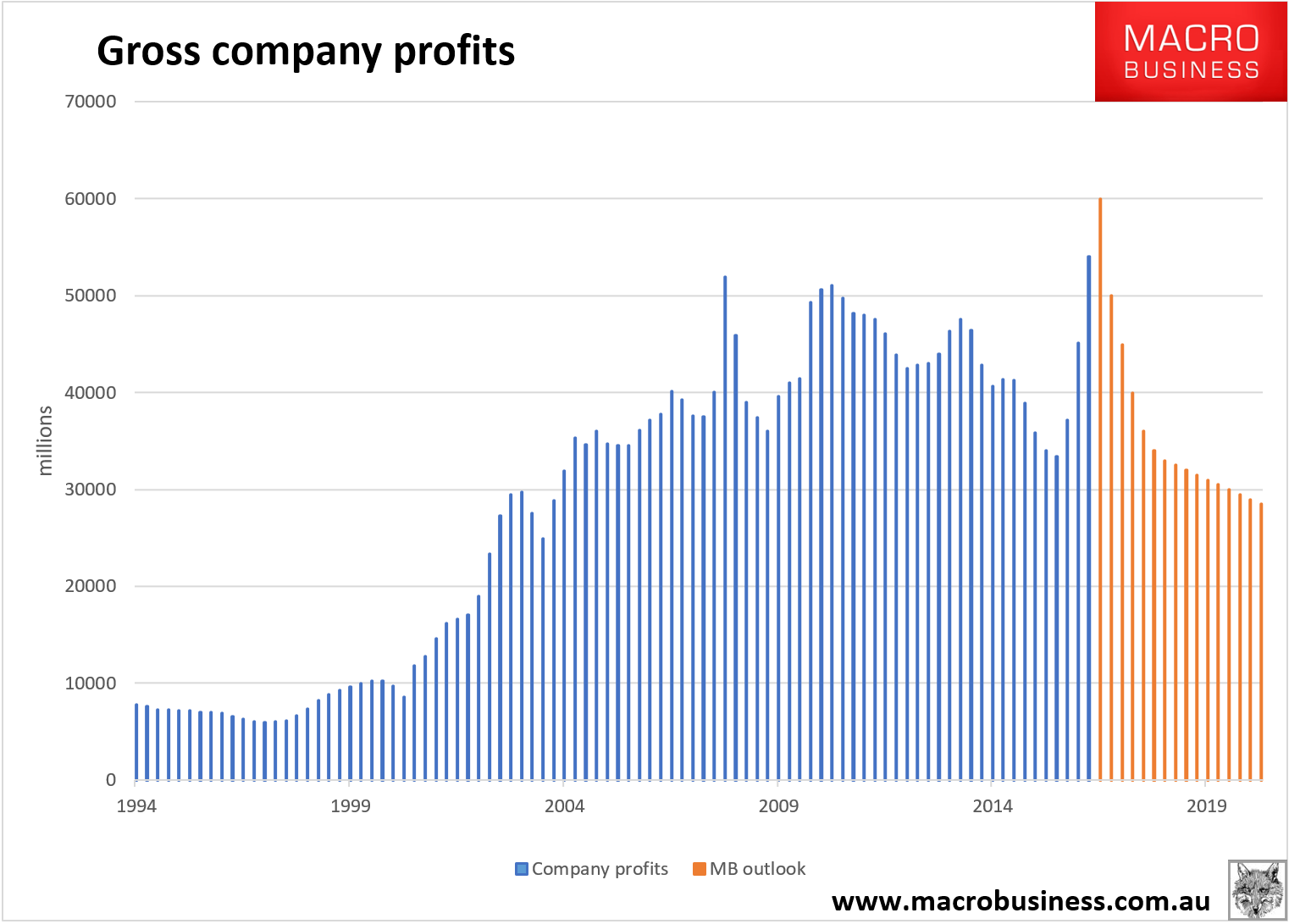

And, given iron ore plays the key role in income generation across the economy, the flow on effect for wider corporate profits will also be very negative:

It’s a much better idea to take your ill-gotten property gains and stick them offshore, where you can make profits amplified by a falling dollar while you wait for the local economy to deflate with the iron ore price.

We can show how to do that from next month, with the launch of the MB Fund which is 70% allocated to international equities. If you have not already, register your interest today: