Don’t be mistaken, no politician anywhere has done anything yet to end the gas crisis. Today from The Australian:

East coast commercial and industrial gas customers are being charged an astounding $12-$15 a gigajoule for long-term contracts as the closure of the Hazelwood brown coal power station in Victoria, combined with Queensland LNG project gas demand, sparks fears of winter gas shortages, according to listed energy consultants Energy Action.

And prices will continue to rise if there is a cold winter, according to the company’s trading and pricing head, David Rylah, with the resultant extra demand from gas-fired power stations leaving little for other users.

“We contract for large users, commercial and industrial, and we’re seeing them being offered at prices of $12-$15. These are real prices being signed in real contracts,” Mr Rylah told The Australian. “Two or three years ago, even when everyone knew LNG demand was coming, prices were on the way up but were $5-$8 (from traditional levels of $3-$4).”

“The rate of the tightening of the supply and demand balance is much quicker than anyone had anticipated,” he added.

“And as soon as cold weather hits southern Australia in the first winter without Hazelwood, and both physical gas demand and gas-fired generation demand hits the market, volatility and price, we believe, will get a further jolt.”

…“LNG projects consuming large volumes at a flat rate are a much better customer than somebody consuming peaking loads for two years, so there are volume discounts at play,” said Mr Rylah, who has been negotiating on behalf of domestic buyers for 21 years.

…“Demand destruction will probably take about 12 months to move through if people realise they can’t pass on higher prices,” Mr Rylah said.

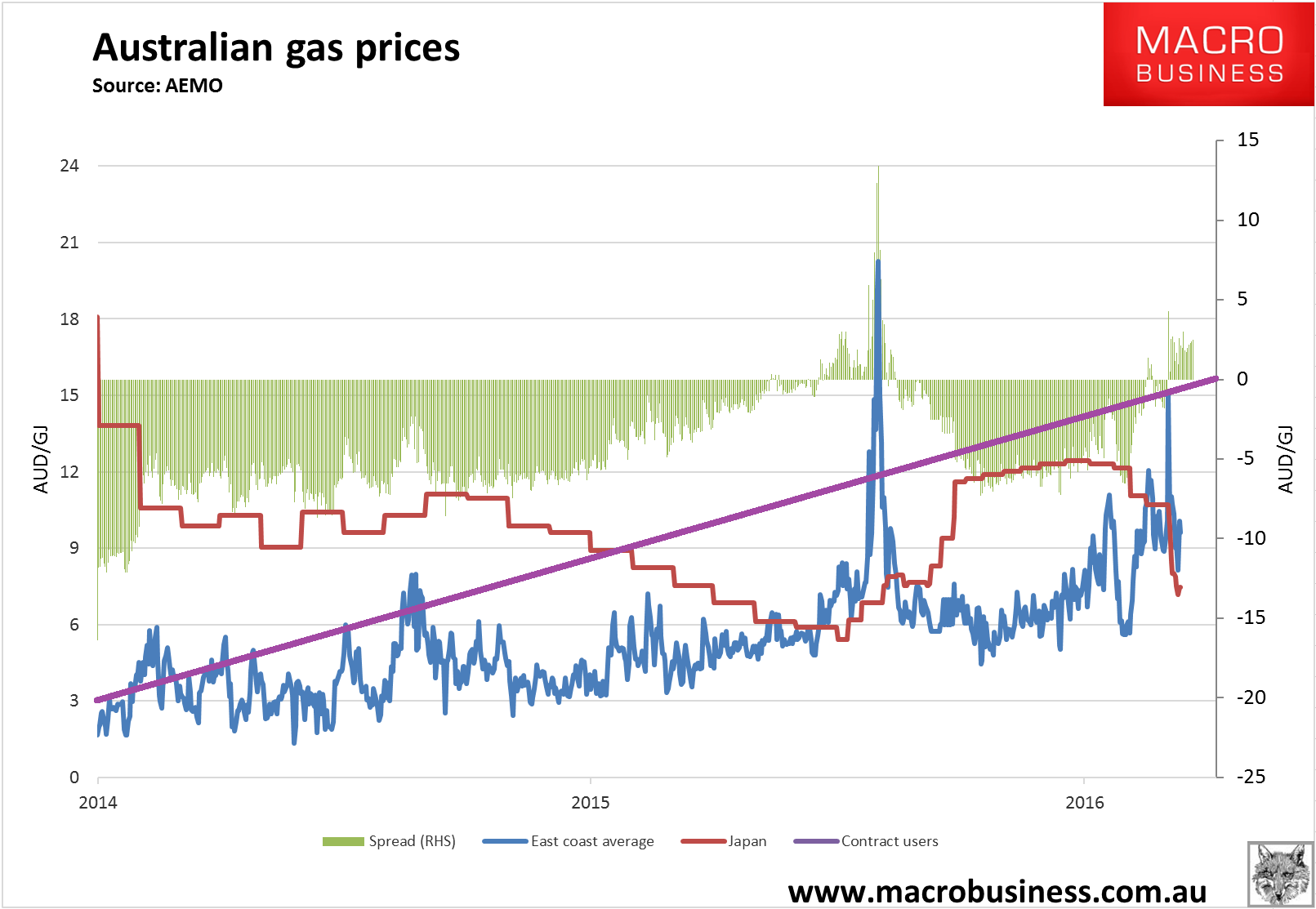

Here’s the chart:

As Credit Suisse has argued, the cheapest and quickest solution is:

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5%

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5% thirdparty gas – 20–25PJa. APLNG is self-sufficient, but as can be seen the other thirdparty gas would get extremely close to balancing the market. Clearly these things are far better done by mutual agreement from all parties, rather than a political mandate.

■ GLNG loses but can all be compensated? We estimate that, at a US$65/bbl oil price, GLNG as an entity would lose US$447m p.a. of FCF if they could no longer toll thirdparty volumes. Interestingly, if Kogas and Petronas could recontract their offtake on a slope of 12x (doable in the current LNG market) then their losses as an equity partner are all offset (not equally between the two albeit). Santos would see ~50% of its US$134mn net GLNG loss offset if the Horizon contract could move up to a slope of 8x from 6x. The clear loser would be Total. We wonder whether cheap government debt, a la NAIF, could be provided at the (new, lower volume) project level or even to take/fund an equity stake in it? In reality all parties (domestic buyers included) have some culpability in the situation, so a sharing of pain does not seem unreasonable 02 March 2017 Australia and NZ Market daily 31.

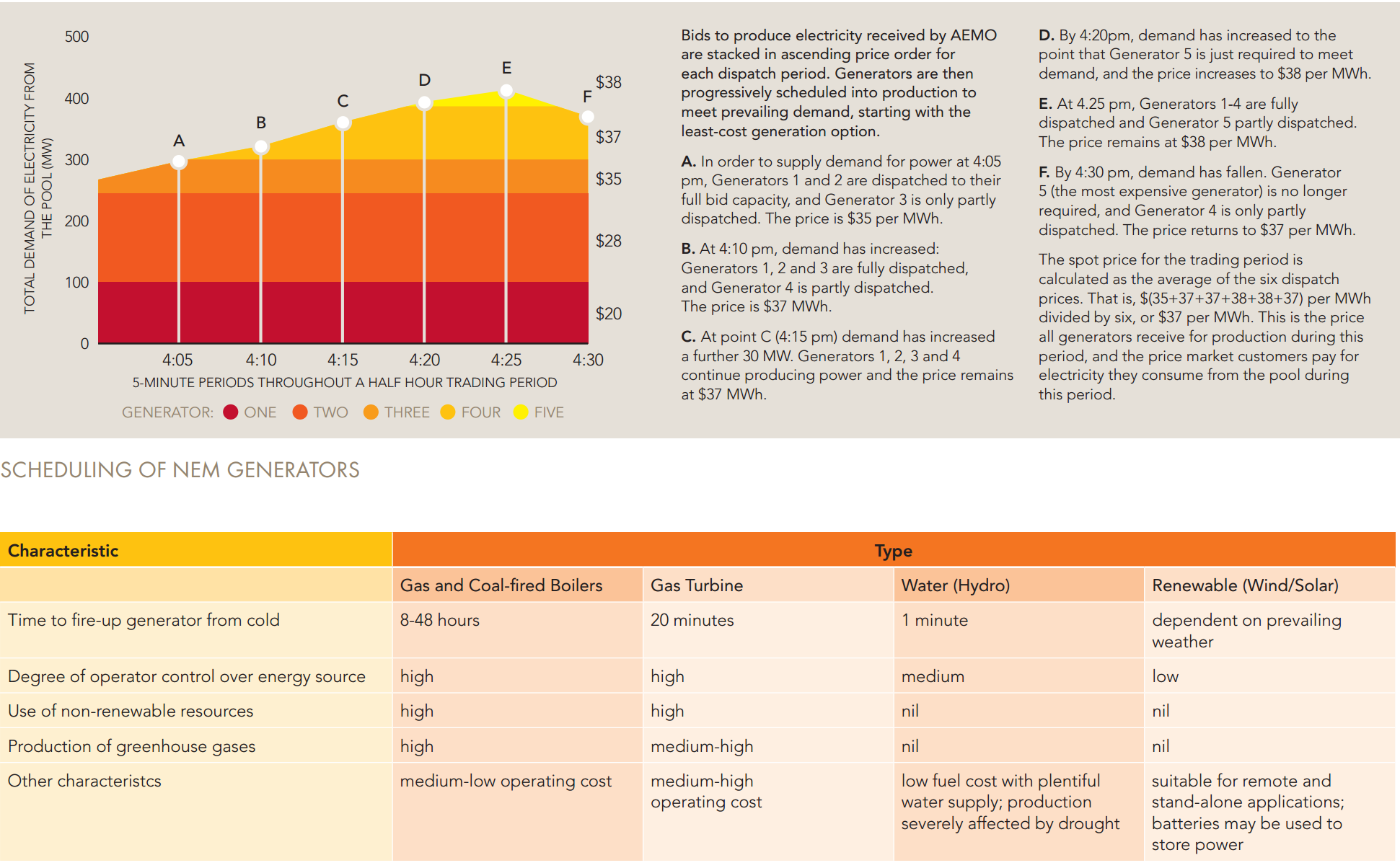

Banning third party exports of gas will instantly free it up for domestic use. That, in turn, will fire up idled gas power plants and drop electricity prices. It is gas that sets the marginal cost in the NEM owing to where it sits in the wholesale electricity market bid stack. See Australian Energy Market Operator description below:

We need cheaper gas and stable carbon pricing policy. Then all of the problems will go away at once and we’ll have time to decarbonise the network with longer term battery and other storage options to stabilise renewables. This was always the national plan, such as it was, that gas would be the transitional fuel as we move steadily from coal power to renewables.

Two things have gone wrong with it. Policy chaos has delayed renewable deployment and an east coast gas cartel has formed around Curtis Island.

Both need to be fixed with urgency.