From Gary Banks, inaugural chairman of the Productivity Commission at the AFR:

Even by today’s standards, the misleading, disingenuous and partisan nature of the energy policy “debate” seemed to have plumbed new depths. So be it, I thought, it’s no longer my job to call out such things. But then a state premier went and made the following observation:

“We’ve got market failure. We know there is an investment strike. The private sector just isn’t building power generation.”

…The inconvenient truth is that the increasingly high prices for increasingly unreliable electricity are a direct consequence of the increasingly high utilisation of renewable energy required by government regulation.

…In blaming the private sector for Australia’s energy problems, there is a real risk that the policy mistakes that led to it will be compounded by further policy mistakes, rather than leading to corrective actions that acknowledge regulatory error. We seem destined to end up in a third or fourth-best world, as economists express it, when the first or second best were well within reach.

Thus we observe at the federal level the threat of regulatory intervention to withhold gas exports for domestic use – while at the same time state and territory governments ban or curtail exploration and production. We even see governments re-entering the energy business. South Australia is to spend a lazy half billion dollars on a new gas generation plant. The Commonwealth is contemplating investing in clean coal generation using its $5 billion northern infrastructure fund, the Minister responsible declaring “the only people who can get rid of sovereign risks are the sovereigns”!

True enough but I’ll note in passing that the bigger failure was that of both the Gillard and Abbott Governments. The first should have scrapped the RET when it installed a carbon price and the latter should not have scrapped the price. We would not be having this discussion today had that been the case.

South Australia has some of the best renewable power endowment in the world on its windy coastline. Had policy been handled properly it would still have been harnessed but in a way that would also have installed greater storage, as well as gas power to handle the intermittency.

And that’s where we do come to “market failure” and the role of gas which Mr Banks neglects to mention.

Everyone assumed that gas would pick up the role of base load power. But the government has little role in the development of Australian gas markets and while everyone was making that comfortable assumption, a raging LNG bubble blew up the domestic Australian gas market.

It wasn’t government that did that. Is was the lack of it. There was no regulator of Australian gas reserves or mechanism by which exports can be modulated to protect the national interest. There was just companies and their push to extract more of it. And they got way over-excited.

Indeed, one them lied. It lied direct to government and to the Australian people about how much gas it had:

As Santos worked toward approving its company-transforming Gladstone LNG project at the start of this decade, managing director David Knox made the sensible statement that he would approve one LNG train, capable of exporting the equivalent of half the east coast’s gas demand, rather than two because the venture did not yet have enough gas for the second.

“You’ve got to be absolutely confident when you sanction trains that you’ve got the full gas supply to meet your contractual obligations that you’ve signed out with the buyers,” Mr Knox told investors in August 2010 when asked why the plan was to sanction just one train first up.

“In order to do it (approve the second train) we need to have absolute confidence ourselves that we’ve got all the molecules in order to fill that second train.”

But in the months ahead, things changed. In January, 2011, the Peter Coates-chaired Santos board approved a $US16 billion plan to go ahead with two LNG trains from the beginning….as a result of the decision and a series of other factors, GLNG last quarter had to buy more than half the gas it exported from other parties.

…In hindsight, assumptions that gave Santos confidence it could find the gas to support two LNG trains, and which were gradually revealed to investors as the project progressed, look more like leaps of faith.

…When GLNG was approved as a two-train project, Mr Knox assuredly answered questions about gas reserves.

“We have plenty of gas,” he told investors. “We have the reserves we require, which is why we’ve not been participating in acquisitions in Queensland of late — we have the reserves, we’re very confident of that.”

But even then, and unbeknown to investors, Santos was planning more domestic gas purchases, from a domestic market where it had wrongly expected prices to stay low. This was revealed in August 2012, after the GLNG budget rose by $US2.5bn to $US18.5bn because, Santos said, of extra drilling and compression requirements.

Now, there is a role here played by shifts in policy around fraccing. But it’s pretty clear that STO knew in its development stages that it did NOT have enough gas and that a second train was one almighty gamble. It went ahead with the mal-investment anyway and is now sucking too much gas from the east coast economy to fulfill contract obligations for gas delivery on which it is losing money hand over fist. This is market failure writ large.

As Credit Suisse has argued, the cheapest and quickest solution is:

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5%

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5% thirdparty gas – 20–25PJa. APLNG is self-sufficient, but as can be seen the other thirdparty gas would get extremely close to balancing the market. Clearly these things are far better done by mutual agreement from all parties, rather than a political mandate.

■ GLNG loses but can all be compensated? We estimate that, at a US$65/bbl oil price, GLNG as an entity would lose US$447m p.a. of FCF if they could no longer toll thirdparty volumes. Interestingly, if Kogas and Petronas could recontract their offtake on a slope of 12x (doable in the current LNG market) then their losses as an equity partner are all offset (not equally between the two albeit). Santos would see ~50% of its US$134mn net GLNG loss offset if the Horizon contract could move up to a slope of 8x from 6x. The clear loser would be Total. We wonder whether cheap government debt, a la NAIF, could be provided at the (new, lower volume) project level or even to take/fund an equity stake in it? In reality all parties (domestic buyers included) have some culpability in the situation, so a sharing of pain does not seem unreasonable 02 March 2017 Australia and NZ Market daily 31.

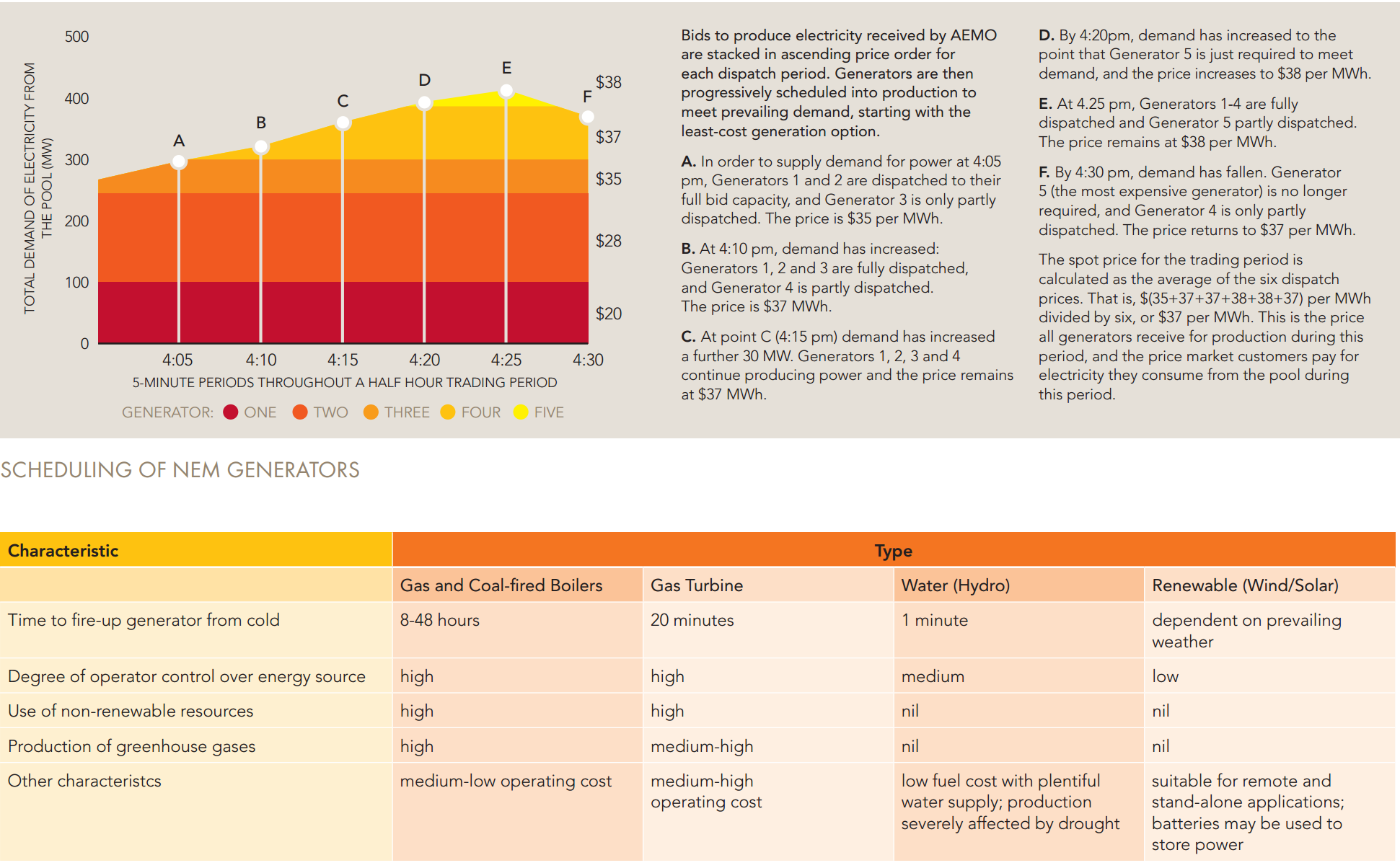

Banning third party exports of gas will instantly free it up for domestic use. By next year it will only be 3.6% of total exports that we’ve held back. But that will be enough to fire up idled gas power plants and drop electricity prices. It is gas that sets the marginal cost in the NEM owing to where it sits in the wholesale electricity market bid stack. See Australian Energy Market Operator description below:

We need cheaper gas and stable carbon pricing policy. Then all of the problems will go away at once and we’ll have time to decarbonise the network with longer term battery and other storage options to stabilise renewables. This was always the national plan, such as it was, that gas would be the transitional fuel as we move steadily from coal power to renewables.

Gary Banks can argue all he likes about whether this test tube of that contains his perfect market. But right now Australia needs simple and firm government intervention in the gas market or the nation will risk further erosion in the very foundation stone of its modernity.