By Gareth Aird, Senior Economist at CBA:

Key Points:

- House price cycles are not captured in the CPI because the cost of land is excluded from the consumer basket.

- The CPI is a poor barometer of changes in the cost of living for people who don’t own a dwelling and aspire to purchase one.

- Consumer price inflation would look very different in Australia if the complete cost of a dwelling was included in the CPI.

Overview:

The CPI is generally considered to be a de-facto cost of living index. It is the measure of inflation that most policymakers and commentators refer to when making statements about changes in the cost of living. Real wages, for example, are calculated as nominal wages deflated by the CPI. But there is a massive flaw in using the CPI as a proxy for changes in the cost of living. The index ignores price changes in the single biggest purchase a person (or household) is likely to make in their lifetime – a dwelling. For households that do not own a dwelling and aspire to purchase one, the CPI is a very poor measure of changes in the cost of living.

In this note we look at the justification for the omission of dwelling prices in the CPI. We then create a theoretical CPI that includes dwelling prices for illustrative purposes. We conclude with a brief discussion on the relationship between monetary policy, inflation and house prices.

Rationale for the exclusion of dwelling prices in the CPI:

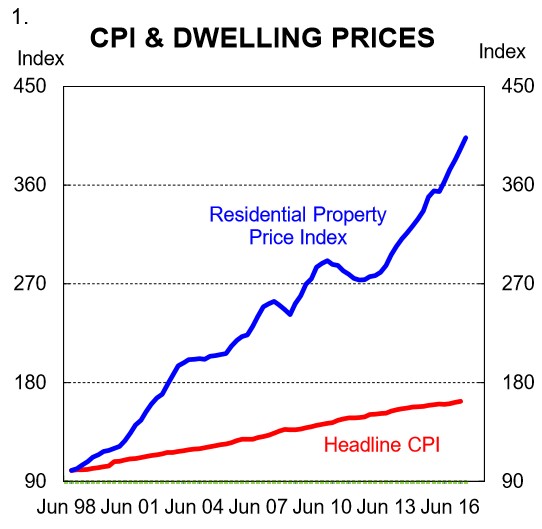

According to the ABS, consumer inflation in Australia has risen by 63% since 1998. Over that same period, national dwelling prices have lifted by ~300% (chart 1).

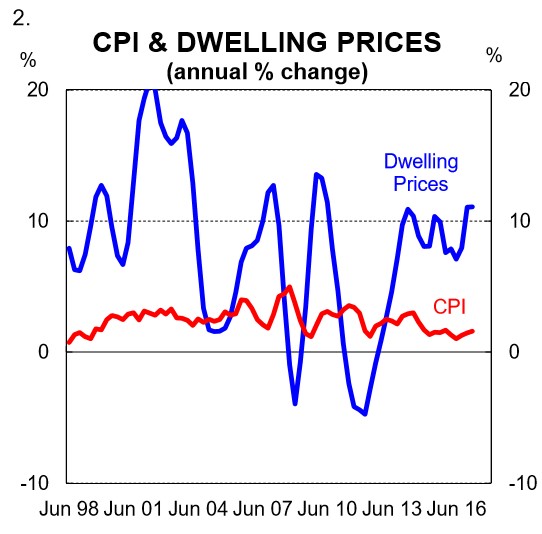

Looking at the more recent past, dwelling prices have lifted by 44% since QI 2013 while headline inflation has only risen by 8% (chart 2).

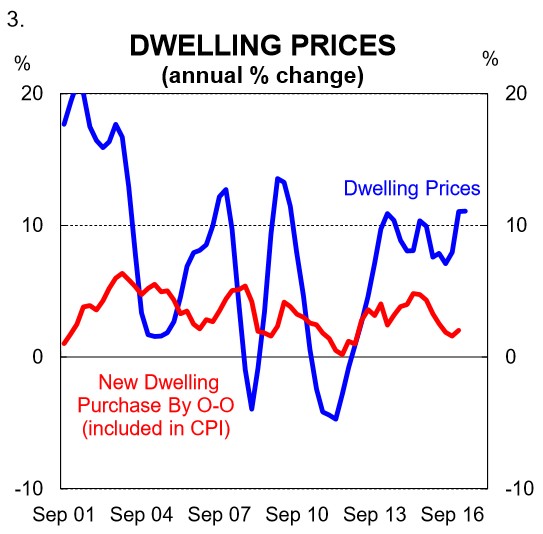

For all intents and purposes, dwelling prices are excluded from the CPI. In a technical sense, “new dwelling purchase by owner-occupiers” is included. But this is simply the cost of new homes excluding land (i.e. it is basically a residential construction cost index). In reality it’s not a representative measure of dwelling prices because it doesn’t take into account the primary driver of changes in the price of a dwelling – which is of course the price of land. Growth in the new homes ex-land component of the CPI bears no resemblance to changes in dwelling prices (chart 3). And yet this component of the CPI is worth a non-trivial 8.7% of the total basket.

According to the ABS, land prices are excluded from the CPI because they don’t fit the definition of a consumption good. The ABS states that, “the

CPI only includes goods and services that are purchased by households for consumption. A consumption good or service is one from which households directly derive utility or satisfaction. Any business – related purchases by households are excluded from the basket, as are those items that have a significant savings or investment component, such as land and capital goods.”

Here one could reasonably argue that purchasing a home to live in has aspects of both investment and consumption as utility and satisfaction are derived from home ownership.

We continue: the ABS also states that, “the principal purpose of the CPI has been to measure inflation faced by households to support the operation of macroeconomic policy decision making.”

Our emphasis is on “inflation faced by households” because clearly based on the exclusion of land prices in the CPI the ABS does not consider dwelling price rises to be “inflation faced by households”. That is true for households who own a home. But for aspiring home owners dwelling prices are part of the inflation that they face. Their exclusion from the CPI therefore makes it an inaccurate measure of the type of living costs that they face.

The RBA supports the exclusion of land prices in the CPI and according to the central bank, “the purchase of existing housing represents a transfer within the household sector (which means that there is zero net expenditure by the household sector in these transactions)”. Very true. But then rent is also effectively a transfer within the household sector from tenant to landlord and rent is included in the CPI.

Land is not the only component of the cost of home ownership that is excluded from the CPI. Mortgage interest payments are also not in the consumer basket (they were included prior to 1998). And there is no estimate of imputed rent (i.e. owner-occupiers are effectively renting properties from themselves). This simply leaves “rent” as being the main component of the CPI that picks up changes in the cost of having a roof over one’s head, notwithstanding the ‘residential construction cost index’ component. This would be fine if households were completely indifferent between renting and purchasing a home (i.e. if they were perfect substitutes). But this is simply not the case.

Here we want to point out that we are not arguing for the inclusion of dwelling prices in the CPI. Rather, we are questioning the basis for their exclusion given nothing in the CPI as it currently stands fairly picks up changes in the cost of purchasing a dwelling to live in.

What if the complete cost of a dwelling was included in the CPI?

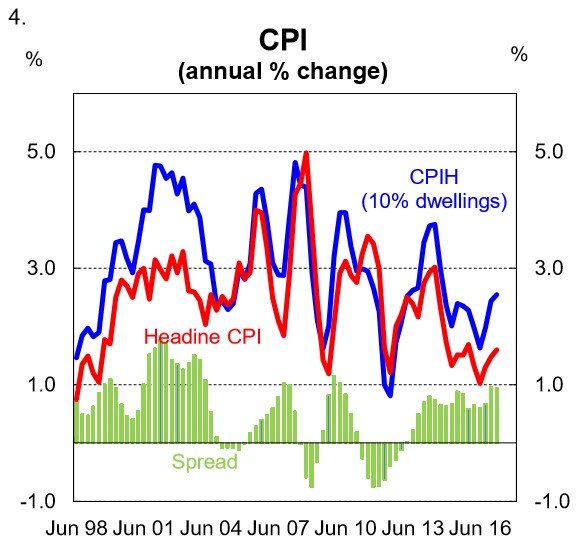

For illustrative purposes, it’s very easy to construct a CPI that includes changes in dwelling prices. Here we construct a modified CPI (called CPIH) whereby dwelling prices account for 10% of the basket – roughly equivalent in size to the “new dwelling purchase by owner-occupiers” component of the CPI. We use the ABS residential price index as the measure of changes in dwelling prices to construct our new CPIH. The results are telling, but unsurprising. The inclusion of dwelling prices in CPIH, even just accounting for 10% of the basket, pushes up the annual change significantly since 1998. The annual change in CPIH is, on average, 55bps higher than the annual change in CPI (chart 4).

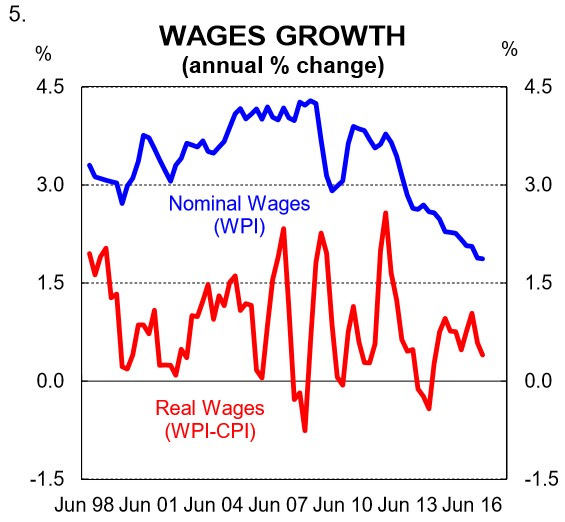

The point of this exercise is to highlight how the exclusion of dwelling prices from the CPI has masked the uplift in the cost of living for households who don’t own a dwelling but aspire to purchase one. For them, the cost of living has risen by more than is implied by the CPI. This is, to an extent, very much a question of generational equity. Real wages growth has generally been positive over the past five years despite falling nominal wages growth as CPI inflation has been trending down (chart 5).

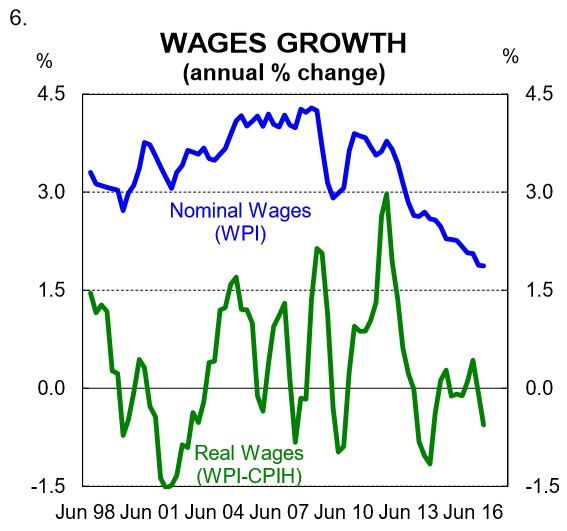

But if we deflate nominal wages growth by a measure of inflation that includes dwelling prices (i.e. CPIH) the picture looks quite different (chart 6). Deflating wages growth by CPIH more accurately captures real wage changes for those who aspire to own a home. These individuals (or households) are generally below 35.

To put it another way, younger people, who are less likely to own a dwelling, have faced a greater deterioration in real wages than is implied by deflating nominal wages by the CPI. This is because the single biggest purchase they are yet to make is not included in the CPI. And it has, of course, been rising much, much quicker than the CPI itself.

CPI, dwelling prices and monetary policy

There is a monetary policy, inflation and dwelling price nexus. The RBA’s mandate is to maintain price stability, full employment and the economic prosperity and welfare of the Australian people. To achieve this, the Bank has an ‘inflation target’ and seeks to keep consumer price inflation in the economy, as measured by the CPI, in the 2–3% range on average, over the medium term.

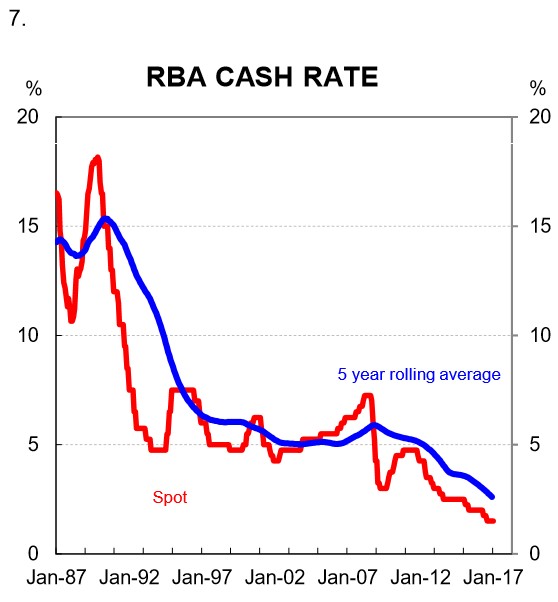

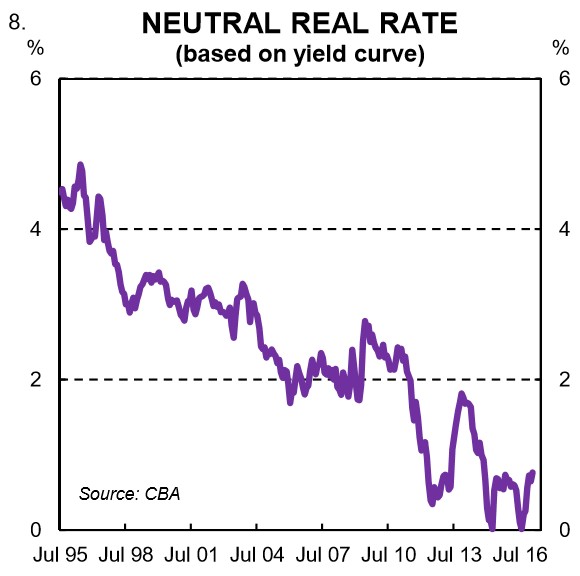

Interest rates have needed to be on a long-run downward trend for the RBA to meet its inflation target as the neutral rate has fallen (charts 7 and 8). We covered this back in February.

Throughout that period, Australia’s stock of debt has risen as a share of income, mainly driven by the household sector (chart 9). Most of that debt has been going into bricks and mortar and dwelling prices have therefore risen faster than income. But as discussed above, none of this has been captured in the CPI.

Back in 1997, the RBA argued against the inclusion of land in the CPI in its submission to the 13th Series CPI review. And they also argued against including a mortgage interest component in the CPI because, “the interest charges as measured tend to distort the signal offered by the CPI of inflationary trends, by incorporating the policy responses to those trends.” In other words, if the RBA cut (increased) rates then interest charges would fall (rise) thereby having the opposite intended impact by pushing down (up) on CPI inflation. But including dwelling prices in the CPI would assist the RBA in hitting its inflation target. Lowering (raising) interest rates has an immediate positive (negative) impact on the price of the very thing not included in the CPI – dwelling prices.

The hangover in Australia from pushing interest rates lower over an extended period of time to hit an inflation target has been a huge accumulation of debt and very high dwelling prices. A raft of other policy decisions have also played their part.

The interest rate lever has helped to smooth out the business cycle. But as we sit close to the lower bound in rates, and with debt a share of income at a record high, it seems futile to chase inflation any lower via more monetary policy stimulus unless the housing market falters and the appetite for additional debt cools. A suite of policy reforms could help here.

When Governor Lowe appeared before the House of Representatives Standing Committee on Economics in late February he stated that, “the main effect (of another rate cut) would be more borrowing for housing, pushing up housing prices.” Touché!