We are nothing if not surprised to read this morning’s article in the AFR, suggesting that the message from the gas producers is that AEMO (and we guess therefore implicitly us) have it wrong on the looming gas shortages.

We note the comments from APPEA that “clearly there is more gas being brought to market” and that the article highlights an expectation that “Origin and Shell will also point to new contracts they have signed with domestic power producers and manufacturers since the initial meeting last month”. Whilst this is good to see, there is absolutely no evidence that has been provided to suggest that this is new supply being brought to market – it seems impossible to see how it would be in Origin’s case and with Shell they have not made clear if any of it is anything other than gas diverted away from exports.

To an extent one could argue that it doesn’t matter if gas is coming domestically as a diversion away from exports by Shell – gas is gas is gas. However, this largely misses the point for us.

It should not escape anyone’s notice that these contracts being signed are 6-18 month deals. With an oil price around US$55/bbl, Shell’s cash ambivalent price (bearing in mind it can supply LNG contracts out of portfolio) is somewhere around A$8-9/GJ at Gladstone (this admittedly is off contract, not spot, LNG prices – we have accounted for cash costs of liquefaction etc). Whilst calling the oil price is hard even on a 6-18 month view, the risks around small volumes for a short period, particularly given the political benefits of being seen to do something, are low for a business like Shell.

But is anyone stepping up and offering 5-10 year term volumes? Let’s use the ~US$80/bbl that Santos and Origin broadly use in the reserve testing (who knows in business planning), then you are talking about a cash-ambivalent price of ~A$15/GJ into the Gladstone plants. Add the now famous A$3.50/GJ of transportation costs from Queensland to Victoria and the economically rational price for an LNG project to divert export gas to a customer in Victoria is potentially ~A$18.50/GJ.

The challenge with so much of this debate is a lack of publicly available data on production expectations, frankly a lack of geological certainty even if we had those expectations and any clarity on at what price gas the LNG projects would be happy to divert long-term gas to domestic users.

With the intermediaries (the likes of AGL, Origin and EA) having largely stepped away from their role for C&I customers (in many ways understandably given the risks they would take on over volumes with an uncertain demand outlook and the more onerous asks being put on them by upstream suppliers) there is also a seemingly gaping hole in how the market has traditionally worked.

For many decades most industrial users went to the intermediaries and had pretty simple discussions on volumes, level of take or pay, duration and signed a CPI linked contract. Now the intermediaries are asking why they should sign up for 10PJ’s of gas a year, taking on that volume risk, when it is unclear how much of that demand will last the duration of the contract that the producers might want them to take. From our conversations with many gas buyers, it seems that many buyers wouldn’t even know where to start negotiating directly with the producer.

We believe the market is ripe for either manufactures to team up together, or for the government to fulfil the role of a pseudo book builder. Let’s make everything public so we really all know where everyone stands. If a public tender was put out for say 50PJa for 10 years, from 2019, and all bids were made public on volume, tenure and price then we would truly have an answer on what gas is available at what price (ex geological/operational risk on delivering those volumes). We can understand struggling industrials not wanting to take on this risk independently (although collectively bidding mitigates it to an extent), nor do they offer the scale necessary in most cases, so maybe the government is better placed? Let’s be honest, with >300PJa of redundant capacity on Curtis Island there is always going to be somewhere to re-sell excess gas if it eventuated, just price risk really exists here. We are being unduly dismissive of the logistical challenges of delivery etc, but hopefully the point is clear that a public book build process would reveal the vast majority of the unanswered questions on how big the problem is and where it truly sits.

Nothing to see here?

We sincerely hope that the message the gas producers take to the PM next week is not one of “we know we didn’t say it last month, but turns out there really isn’t a problem”. Whilst we, along with them, have raised consistent concerns over AEMO’s numbers, we only have the LNG projects at “contracted” (remember QCLNG really isn’t dedicated contracts as such) volumes and still see a large shortage. That is not to say our numbers will be right, they almost certainly will not be, but it appears a mathematical impossibility that current contracted volumes and existing domestic gas demand can all be met over the coming few years. Whilst we do not wish to denigrate the move, it is needed and in plenty more spades, Shell selling 6-18 months’ of supply to a couple of domestic customers does not instantly fix things. There is undoubtedly a domestic gas price and an export price at which it becomes entirely economically rational for Shell to sell domestically (it could in theory comfortably supply all of industrial demand), but whether we see them commit to material volumes and more importantly for serious duration is a different question.

The intermediaries have stepped away

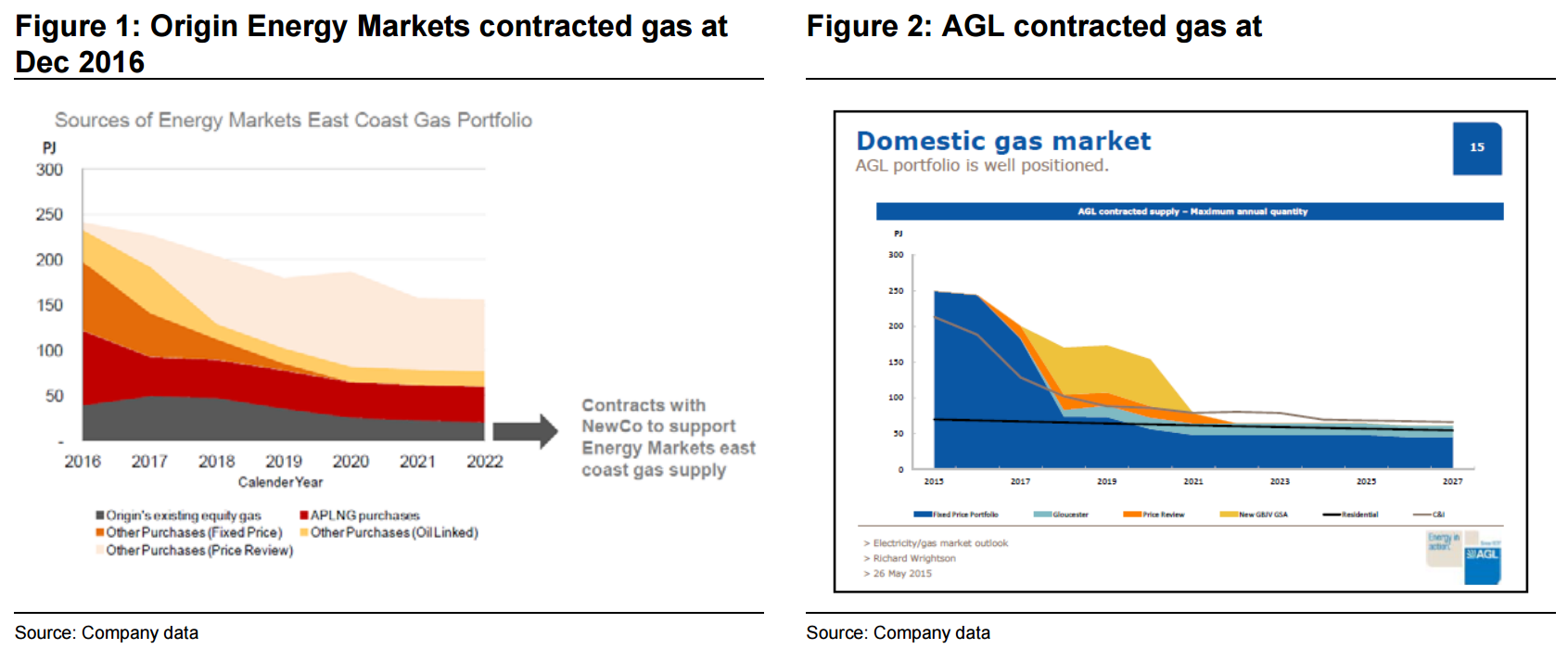

What becomes ever clearer from both simple facts (admittedly we have been accused in the past of not being able to grasp simple facts), and anecdotal comments from industrial gas buyers, is that the intermediaries (the big ones being AGL, Origin and Energy Australia) are stepping away from their role of supplying C&I customers. As can be seen in Figure 1 , Origin will have maybe 60-80PJa less supply by 2020 vs what they had last year. AGL will have <100PJa by the start of the decade (since the chart in Figure 2 they have lost Gloucester and gained 12PJa from Sole post 2019). We get no public disclosure on Energy Australia’s book, but it is hard to imagine it looks much different – it is pretty hard to see where they would have contracted material volumes of gas from anyway. Clearly the merit order for these companies, in terms of meeting demand, is to fill retail and generation before worrying about C&I customers. Fundamentally, as we roll into the early part of next decade (particularly given both companies’ sales agreements to LNG projects) both Origin and AGL are risking looking short of gas currently to honour existing retail, generation and existing commercial contracted demands collectively.

To be fair, whether they have made this clear implicitly or explicitly, the challenge for the intermediaries is understandable. They are asked to take on material volume risk (at a far higher price than historically, so the bet on being wrong is bigger) when the medium term certainty simply doesn’t exist on demand and they have probably made very mediocre margins on most industrial customers for much of the last decade (although clearly not so currently).

So what do the small/mid-sized C&I customers do now?

From our conversations with numerous gas buyers, the message is resoundingly uniform. No one is willing to offer them volumes from 2019 onwards and any offer for the short/medium term is extremely highly priced. Their list of suppliers is the usual big list of intermediaries. The problem with the intermediaries fundamentally stepping away from this roll is that end users have lost their seller. Even surprisingly large gas users never have, and wouldn’t know where to start, in dealing directly with say a BHP-Esso and arranging transportation/delivery etc. Likewise the major sellers don’t know where to start in trying to sell to 100’s of individually small loads. The split in industrial use probably becomes ever starker in the coming months and years. There are those who are export exposed, or cannot pass through the cost increases for other reasons, who will get forced to shut down if affordable, term gas isn’t made available soon. There are then those we can pass it through, who will frankly potentially source gas at any cost to ensure the cogs keep turning. Despite a distinguished 7 month career as an economic consultant for yours truly, we will leave the economic implications to those economists far smarter than us. What this does begin to sniff of though is large scale unemployment on the one hand, just as material inflationary pressures are likely to be getting pushed through by the other half of the equation (particularly with, the cost equation at least, as frightening in electricity as it is in gas).

An obvious way exists to get a truer picture?

We know, we know – we make these grandiose comments that make implementing things sound easy when they are in fact a logistical, political and corporate mine field. Still, that hasn’t stopped us in the past and it won’t stop us now. The reality is that we believe the market is far more structurally challenged than even the growing recognition acknowledges and without clear parameters risks deteriorating further.

What really needs to happen is that we need a clear picture of what volume truly is available, for what duration and at what price. One solution is that the ACCC, government or whoever it might be asks all gas suppliers to provide their answer on what uncontracted gas they have available and at what price they would make it available (this is important for the LNG projects – there is 5-6x industrial demand being exported, that all parties would agree to sell domestically for a high enough price). The risk with this is that it is left to corporate optimism still (and, to be fair, government paving the way for new development), rather than them actually being contractually bound to meet those volumes. If one had asked the producers back in 2012 what they would have available now, it seems highly likely they would have grossly overestimated it. So how about a collective, public tender for gas. Some of Mrs S’ more frugal purchases (there are plenty less frugal ones unfortunately) are done on effectively a crowd buying site, where people bid together to get wholesale prices for goods (how could anyone possibly live without reversible meat trays for their BBQ in 5 different colours?). If a collection of gas buyers, under some guise, came together and offered a material amount of volume for a long tenure, let’s say 50-100PJa for 10 years, then with the tide well and truly out we might get to see which suppliers remembered to put their speedos on.

We would like to see this whole process played out publicly and visibly.

For the say 100PJa for 10 years, each supplier can bid in a volume, a duration and a price at which they can make that gas available. This should by no means be a one-sided event, stacked in favour of the end user. If you have a new project, like Narrabri or Arrow, where you need meaningful volume to justify the infrastructure, risk etc then this is perfect. You can bid in the full 10 years’ of supply at whatever volume and price underpins the economics. If your competitors can’t match it, and there is matched demand at that price, the project is off to the races (political roadblocks aside of course). The challenge, or one of the many challenges (which of course include the complexities of delivery, levels of take or pay, counterparty risk etc), is getting a big enough pool of industrial users together for this. Could the government again play a roll here, as the pseudo intermediary? Again, the complexity issues exist on delivery etc, but one thing is for certain is that if this pseudo book build occurred it would soon become obvious what uncontracted gas is truly available – surely the holy grail in the current debate. We’ll emphasise the point again here that, for Shell in particular given their portfolio flexibility to honour LNG contracts, that more than enough gas could be diverted back domestically if the economic signal is correct. This process would reveal at what price, for long duration (the real key for these LNG volumes) the LNG project participants would be willing to divert gas. Let’s not forget the other LNG projects would in reality be the same too. The offtakers don’t want the gas in most cases, so as long as the sellers are economically ambivalent they should be willing to divert that gas domestically. Fundamentally this would boil down to a view on long run oil – unless they chose to bid in on an oil linked contract too, but one assumes they wouldn’t get many takers for this. We would finally learn where the bottleneck is and how big it is If there truly is enough available gas out there then this process will well and truly highlight that. It will stop the smoke and mirrors of short-term contracts, diverted gas, wishy washy verbal commitments to try and help, etc.

Provide competitively priced gas, for long duration to end customers and the onus of the problem would then fall on the end customer. Particularly if the “book build” is from both sides, with the end-users putting in what volumes they are willing to take, at what price, it should also provide a strong guide to at what price domestic demand disappears involuntarily. One would have to assume that from a volume perspective, if admittedly not a price perspective, the risks of over-contracting the gas is next to nothing. If GLNG is running at 6mtpa, QCLNG at 8mtpa and APLNG at 8.6mtpa then in theory the 6 Trains collectively, if debottlenecked, could accommodate an incremental >300PJa. It feels like the last thing we need to worry about is that gas couldn’t find an end customer the tender has overdone it for true end user demand. Everyone can talk in hyberbole, everyone can talk their own vested interest and play the (understandable) political game. This solution could provide a high level of clarity to cut through all of that nonsense and tell us where we really stand. What does it all mean for the stocks?

We will try and rescue some kind of stock implication from this all.

If the message suggested in the AFR today is right, that the gas industry will be sending the message to the PM next week that all is fine and dandy then it certainly wants to make sure it truly believes it. If our view of the shortage is even close to right and the industry has dismissed it, the potential for more onerous political backlash has to increase dramatically – fool me once and all that … If there were to be some kind of structured “book build” process for new supply then we do think this is a positive for new project development. With the intermediaries seemingly unwilling to underwrite new projects now, and so few industrial buyers of large enough scale to do it alone, it is harder to see how investment decisions will be made in a timely manner when added to all the political and capital challenges already faced. This should help a project like Narabri for Santos (currently valued at $0 by us given the full impairment) and also be significantly supportive for the smaller players actually trying to do something and bring gas to market – the likes of Senex and Beach in our coverage universe spring most obviously to mind here. If this process is done and it turns out that all the problem sits with the buyers (i.e. plentiful, long duration and affordable gas is being offered) then the sword of Damocles could be well and truly removed from above the upstream industry’s head too. To be fair, we really struggle to believe this is the case – but we have been spectacularly wrong in the past and never would we like to be proved wrong more than in this situation.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.