■ ‘Clean coal’ and CCS take the stage: Lately a key strain in our national policy conversation has involved the promotion of ‘clean coal’ – the idea that some coal-fired technologies might allow coal-fired power to be part of a low-emissions generation portfolio. Carbon Capture and Storage (CCS) is occasionally thrown into the discussion when decarbonisation targets are raised.

■ Taking a look at clean coal in more depth: In this note we assess both ultrasupercritical coal technologies (USC) and CCS in order to interrogate these claims a little. We review existing CCS for coal-fired power projects around the world (three, two operational), as well as other CCS projects, and survey existing research on USC and CCS, including cost forecasts and emissions intensity.

■ ‘Clean coal’ a misnomer, CCS far from a done deal: We note that USC plants are only low emissions compared to sub-critical coal – the most emissions intensive option on the NEM. As such, ‘clean coal’ is a misnomer for USC. Furthermore, we note that although CCS technology is often presented as an available option, this technology is presently far from proven for sequestration and storage following power production, and is also far from viable at present. No commercial project to date has captured and stored CO2 emitted from power production. In Australia we have conducted some surveys, some desktop research, and some sequestration trials, but are otherwise in the Dark ages as far as CCS implementation goes.

■ Let’s talk about emissions reductions, rather than getting caught on coal: In our view, the conversation is currently obsessively stuck on coal/no coal, a narrative reflective of our role as an energy exporter. Recent Australian work on CCS has been laser focused on CCS for use in power production. However, we think the conversation needs to move away from this obsession, and consider our least cost emissions reduction options.

■ Consider critical CCS, rather than CCS for those who complain loudest: Broadening this focus a little leads immediately to the fact that CCS will be most critical for industry – much of which has no other emissions reduction option, and a much higher cost of abatement. We make suggestions that CCS apparently more viable for industry, and more critical, Australia’s CCS development efforts should be more effectively allocated. Presently, our CCS policy looks very much like an effort to preserve the assets and resources of a particular industry, rather than an effort to develop CCS as a useful option and deploy it where most needed.

The role of CCS

■ Business as usual in Australia exhausts our CO2 budget by 2030: On current estimates Australia has a carbon budget of 10.1 GT of CO2-e between 2013 and 2050 as part of its share of the 1,700 GT CO2-e global carbon budget. Under a business as usual approach, Australia will exhaust its share of that budget by 2030, according to the latest report from the University of Queensland, Energy Security and Prosperity in Australia: A roadmap for carbon capture and storage. AGL assumes that the electricity sector’s share of this is 3.363 GT, while other analyses assume that electricity will take a larger share. Sector emissions must decline by 7% year on year from 2020 to 2050 to meet the target of decarbonizing the sector by 2050.

■ How much carbon? Australia’s emissions in 2014 were 523MtCO2e. Of this, 181MtCO2e came from power production, 150Mt of this from coal-fired power. Another 93Mt came from transport, 47Mt from manufacturing and construction, 38Mt from fugitive emissions, and 32Mt from industrial processes. Compared to emissions from electricity, industrial emissions are particularly challenging to abate, often being intrinsic to the chemical processes used to create products.

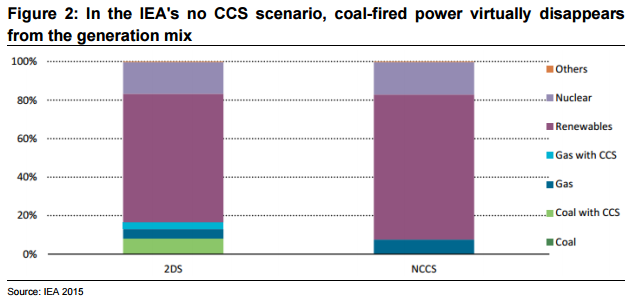

■ IEA says 2 degree scenario needs CCS: CCS is estimated to deliver 94 GT of global CO2 emissions reduction through 2050. This is 12% of the cumulative emissions reduction for the energy sectors. 52 GT of that is estimated to come from the power generation sector (80% of that will be from coal fired generation). This represents 850 GW of electricity generation with CCS (570GW of this will be coal). Any residual coal plant without CCS in 2050 is assumed to be running at very low capacity factors (219 GW). 29 GT is estimated to come from the industrial sector, representing 20% of their emissions. Without CCS, coal-fired power virtually disappears from the generation mix (refer Figure 2).

■ Industrial emissions particular difficult: Emissions reductions from industrial processes would be particularly difficult to eliminate. The use of scrap in the steel and iron sector increases by 80% from 2020 to 2050 but the 2 degree scenario from the IEA assumes there are limits to then availability of economical scrap steel. In cement production, clinker substitution and CCS are considered the only available measures for drastically reducing CO2 emissions.

■ CCS has struggled for power generation: High costs coupled with limited sequestration opportunities outside enhanced oil recovery (EOR) are impacting the future potential of CCS in the electricity sector. At the very same time, the economics of renewables are now well ahead of new coal plant. The race to couple renewables with other methods of storage, such as battery and pumped hydro, means that CCS for power generation may be entirely bypassed in most countries. In Australia, it may well become a technology that is more suited to capturing CO2 from industrial processes that do not have such alternate economic solutions.

■ The size of the problem – an example: A 1000MW coal fired plant working at 90% capacity will generate 7,884 GWh, and likely emit 6.3 MT of CO2. With a 20% energy penalty, only 800MW of that capacity is available for use outside the CCS plant. With 90% of the CO2 captured, 0.63MT of CO2 will be still be emitted for an 800MW plant. This equated to 0.1t/MWh, or about 25% of what a thermal gas plant would emit. Uncompressed, the captured emissions are is 3,153GL or 3,153,654 m3 .

■ Storage options little progressed in Australia: The Federal Energy and Environment Minister, Josh Frydenberg, has described CCS as “absolutely critical” for decarbonisation. However, in Australia CCS cannot work without the storage part of the CCS process. We do not have a history of using CO2 for EOR, so that avenue is not an option for solving the storage puzzle. To date, storage appears to have been the stumbling block for the industry. Finding safe reservoirs within a viable distance to sources of CO2 emissions has been difficult, with only a project in the Otway Basin of Victoria showing any viable progress. However, we understand this basin is too small to provide an industry wide solution, leaving the little explored Gippsland Basin in Victoria and the Surat Basin in Queensland as the only frontiers of possible carbon sequestration.

■ CCS important for viability of some companies: BHP’s scenario for a 2 degree world assumes that CCS is viable and used post 2030. Without CCS, BHP’s energy coal division is expected to be more impacted. In contrast, AGL, with only domestic operations, has reviewed the impacts of a 2 degree scenario, assuming that CCS does not play a part in Australia’s energy mix.

What is “Clean Coal” and CCS?

■ Carbon capture and storage (CCS) is a process to capture carbon dioxide (CO2) emitted from industrial processes such as thermal power generation, gas and oil production, or manufacturing such as cement or steel making. The carbon dioxide is captured before it is released into the atmosphere and “stored” either through sequestration into underground reservoirs or through re-injection into gas reservoirs, often for enhanced oil recovery (EOR).

■ Carbon capture: There are three types of carbon capture: pre-combustion, post combustion and oxyfuel combustion. In the post combustion (most common) capture process, emissions are separated by a solvent or membrane technology that captures the carbon dioxide. It becomes attracted to a liquid or solid material (say an amine solution) and then subject to pressure or temperature to desorb it from the chemical solution to make it suitable for transportation and storage. The carbon capture process requires capital investment to build the capture plant and operating costs for the solvent or filtering process.

■ 90% of carbon dioxide is captured (in the ideal case): The aim of most CCS is to capture 90% of the CO2 emissions, leaving 10% of the CO2 to vent into the atmosphere. However, many plants achieve lower levels of capture, with numbers around 70% being common.

■ Transport: The storage of CO2 usually involves transportation through a pipeline (or via a ship is an option if offshore) to an appropriate underground reservoir. The CO2 is in a compressed liquid form. CO2 transportation technology is mature in some places, with North America having networks for CO2 transportation for use as part of enhanced oil recovery.

■ Storage: The storage reservoir must ensure safe and permanent capture of carbon dioxide and is usually a porous geological structure several kilometres underground. Old oil and gas reservoirs are often suitable, as are deep saline formations. The reinjection is usually at a temperature and pressure to ensure the CO2 is in a liquid form. The storage needs ongoing monitoring to ensure it is safety encapsulating the CO2. The CO2 may just remain in the porous storage (“residual storage”), it may bind with salty water in the reservoir and sink to the bottom of the site (“dissolution storage”) or chemically bind to the rock formations in the site (“mineral storage”). The reservoir has a natural impermeable seal, just like existing oil and gas reservoirs.

■ Energy penalty: All that work to capture carbon and store it requires energy. Most of the energy consumed is spent in capturing and compressing the CO2. This energy spent in CCS is called the energy penalty. This energy penalty is estimated to range from theoretical low bounds of 11% through to 40% with 29% assumed to be a good target (scientists at MIT). The IEA estimates this could become as low as 7-10%.

Coal-fired power not a strong contender for emissions reductions

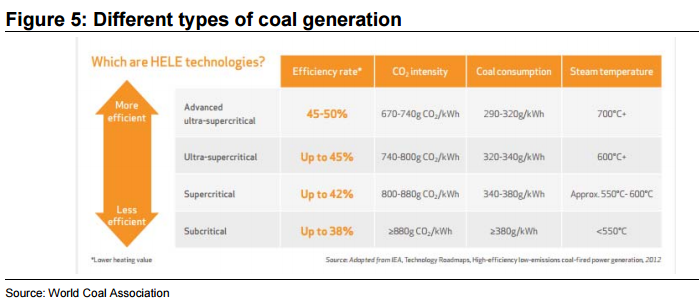

■ “Clean coal” versus “cleaner coal”? There has been much political discourse on “clean coal” in Australia of recent times. But the discourse is not clear on what is meant by “clean coal”. Some of the commentary is coupling CCS as part of the meaning of clean coal. Other discourse is focusing on the “lower emissions” of ultra-super-critical coal (USC) plants, the latest technology for coal fired generation. This technology is sometimes called HELE – high efficient, low emissions coal technology.

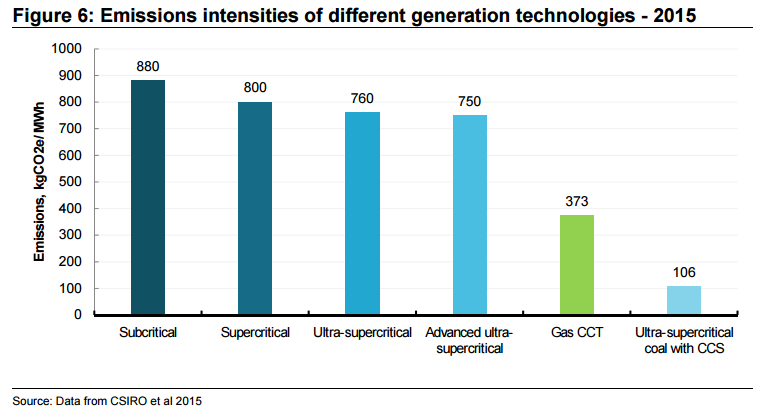

■ USC plants provide ~20% reduction on sub-critical coal: Various USC technologies exist for electricity production from coal-fired power. These technologies achieve emissions reductions by achieving higher thermal efficiency, increasing the power output per unit of coal used. Where existing thermal efficiencies are around ~33%, HELE technology can achieve ~40-45%, reducing emissions from above 0.88t CO2e/MWh for new subcritical coal to ~0.74-0.80tCO2e/MWh (refer Figure 5). This is still twice the emissions produced by base load gas fired generation (CCGT – 0.37tCO2e/MWh – refer Figure 6), so it is important to keep in mind that these stations are only low emissions compared to sub-critical coal-fired power (the most emissions intensive option on the grid). It is expected that R&D efforts will bring these efficiency levels up to 50% or above.

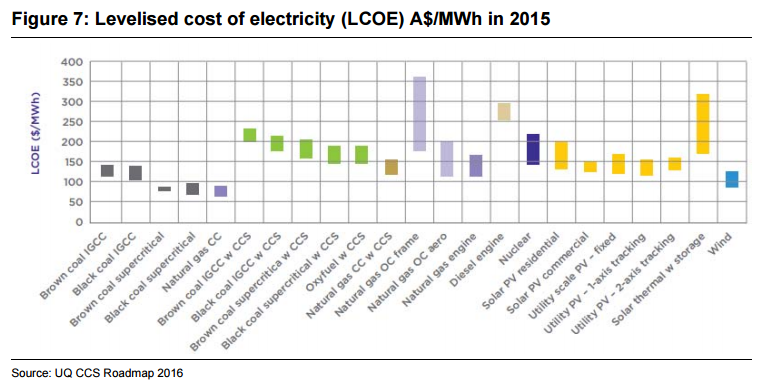

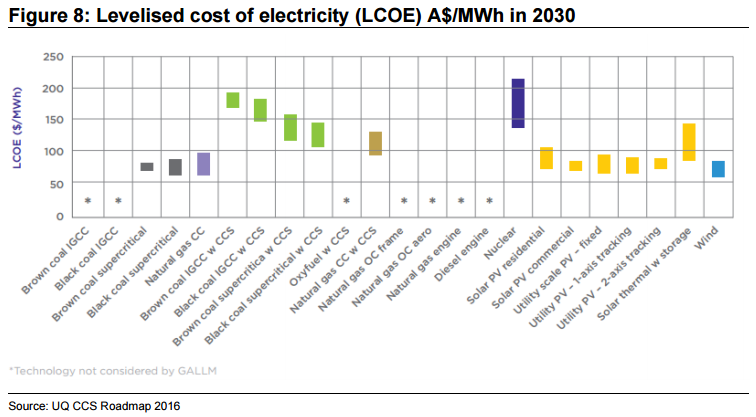

■ USC plants operate at relatively average cost: USC plants tend to have slightly higher LCOEs (Levelised Cost of Electricity – the NPV of the unit cost of electricity over the lifetime of the generating asset or the average breakeven price of electricity) than comparable sub-critical coal-fired plants. This is due to the more expensive materials involved with their construction. However, power production from USC plants is not overly expensive – in the major OECD nations LCOEs for these plants are estimated at around US$95-$120/MWh depending on location, using a 10% discount rate.1 Australian estimates put average estimated LCOEs for new USC plants using black coal at A$80/MWh as of 2015, compared to A$79/MWh for supercritical plants, A$122/MWh for IGCCs and ~A$75/MWh for Combined Cycle Gas.2 Figure 7 and Figure 8 outline cost range estimates made by CSIRO in 2015.

■ USC plants a road to lower emissions? USC plants have been touted in Australia as a route to reducing the emissions produced by the Australian electricity sector, being presented as a low emissions option. As outlined above, the emissions intensity of USC plants is ~0.8-0.74tCO2e/MWh. This is ~14% lower than new subcritical coal, 23% lower than Australia’s existing coal fleet, and about 5% below the current average of the NEM (which is majority fueled by sub-critical coal). Other key contributors to the grid – gas-fired power and renewables – are of course far more emissions efficient that USCs (gas CCTs at ~0.37tCO2e/MWh). As such, USC plants are only low emissions compared to subcritical coal-fired technologies, and the addition of new USC plants would not provide any significant reduction in emissions intensity.

■ What if we stranded existing coal-fired stations? One route to emission reductions often presented is replacing Australia’s existing coal-fired generation fleet (brown and black) with USC technology. This of course firstly requires someone to swallow the cost of stranding existing assets. This difficulty aside, this move would reduce emissions from the production of coal-fired electricity by 23% on our numbers, providing ~20% emissions saving for all electricity production (using 0.76tCO2e/MWh – the most regularly quoted figure for USC plants). This equates to ~7% reduction on Australian emissions (523MtCO2e as of 2014). As an extreme comparison, replacing the entire coal-fired fleet with combined-cycle gas-fired power would result in electricity of roughly the same price, and emissions savings of 62% for replaced power, 52% for the electricity sector and 18% for Australia. This of course assumes gas availability – another of those energy debates that Australia is having.

■ 20% emissions reduction… to 2050: Assuming one were happy funding the replacement of Australia’s entire coal-fired generation stock to achieve these emissions reductions, this proposal has a more important shortcoming. The investment horizons on plants of this magnitude of course run from three or five decades. Investing in a brand new USC fleet would lock in significant generation capacity with relatively high emissions intensity for decades. Least-cost decarbonisation scenarios present emissions savings from coal-fired power of ~90% by 2030, far above the ~20% that would be effectively locked in by a new USC fleet. Undertaking such investment in new USC capacity would take this much of this comparatively cheap emissions reduction opportunity off the table.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.