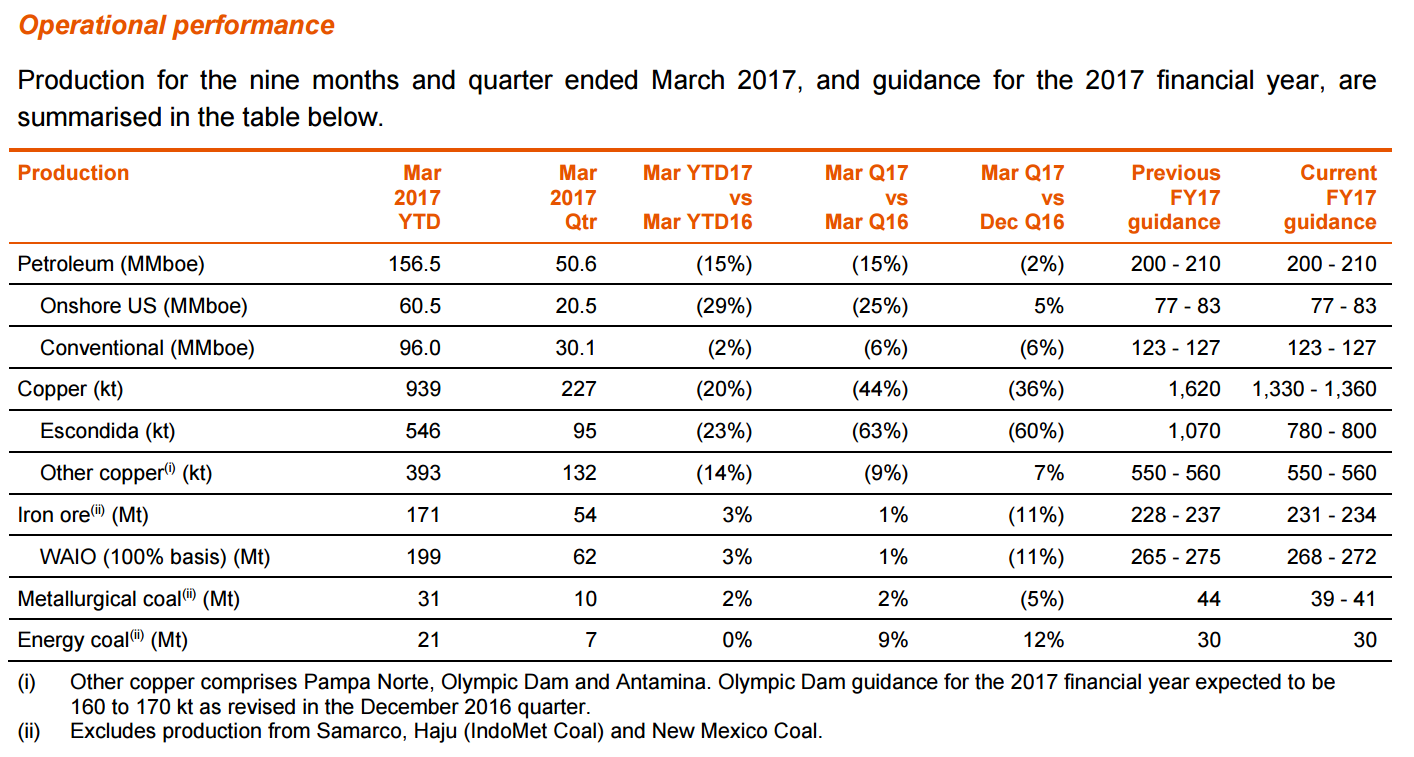

Iron ore – Total iron ore production for the nine months ended March 2017 increased by three per cent to a record 171 Mt, or 199 Mt on a 100 per cent basis. Guidance for the 2017 financial year has been narrowed to between 231 and 234 Mt, or between 268 and 272 Mt on a 100 per cent basis. WAIO production for the nine months ended March 2017 increased as a result of the successful completion of commissioning of a new primary crusher and additional conveying capacity at Jimblebar, ongoing progress on the rail renewal and maintenance program and productivity improvements. This was partially offset by wet weather impacts in the March 2017 quarter. The rail renewal and maintenance program is expected to be completed in the June 2017 quarter, in line with the earlier completion date highlighted previously. On 10 March 2017, BHP Billiton lodged a submission with the Department of Environment Regulation to increase its export licence from 270 Mtpa to 275 Mtpa. BHP Billiton will continue to work with the authorities in relation to the necessary permits to enable an increase in system capacity to 290 Mtpa in the 2019 financial year. Our Yandi mine is currently operating at 80 Mtpa but will be depleted over the next five to 10 years. We are looking at options to replace this production and the low-capital intensive development of South Flank is the preferred longterm solution, subject to Board approval being obtained. The investment case for using this high-grade deposit for replacement tonnes is strong, given our ability to leverage existing infrastructure at the Mining Area C operation. Mining and processing operations at Samarco remain suspended following the failure of the Fundão tailings dam and Santarém water dam on 5 November 2015. During the March 2017 quarter, 35 kt of pellet feed sales were finalised.

BHP will have to ship 71mt of ore before the end of June to meet guidance, the highest volume quarter ever and up 36mt tonnes annualised from the first quarter.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.