As I’ve said since late last year, what we’ve seen over the past six months is the first ever iron ore bubble. The big run-ups in the past have always been supported by genuine supply shortages amid huge demand shocks. This time around, the price rocketed amid a huge glut in supply and only a modest improvement in demand. Thus it was very clearly a bubble, with prices rising simply because they were rising, egged on by the financialisation of dirt in China.

Let’s take a look at some new charts from Macquarie to show just how extreme the mis-pricing has been, as well as how quickly it will unwind.

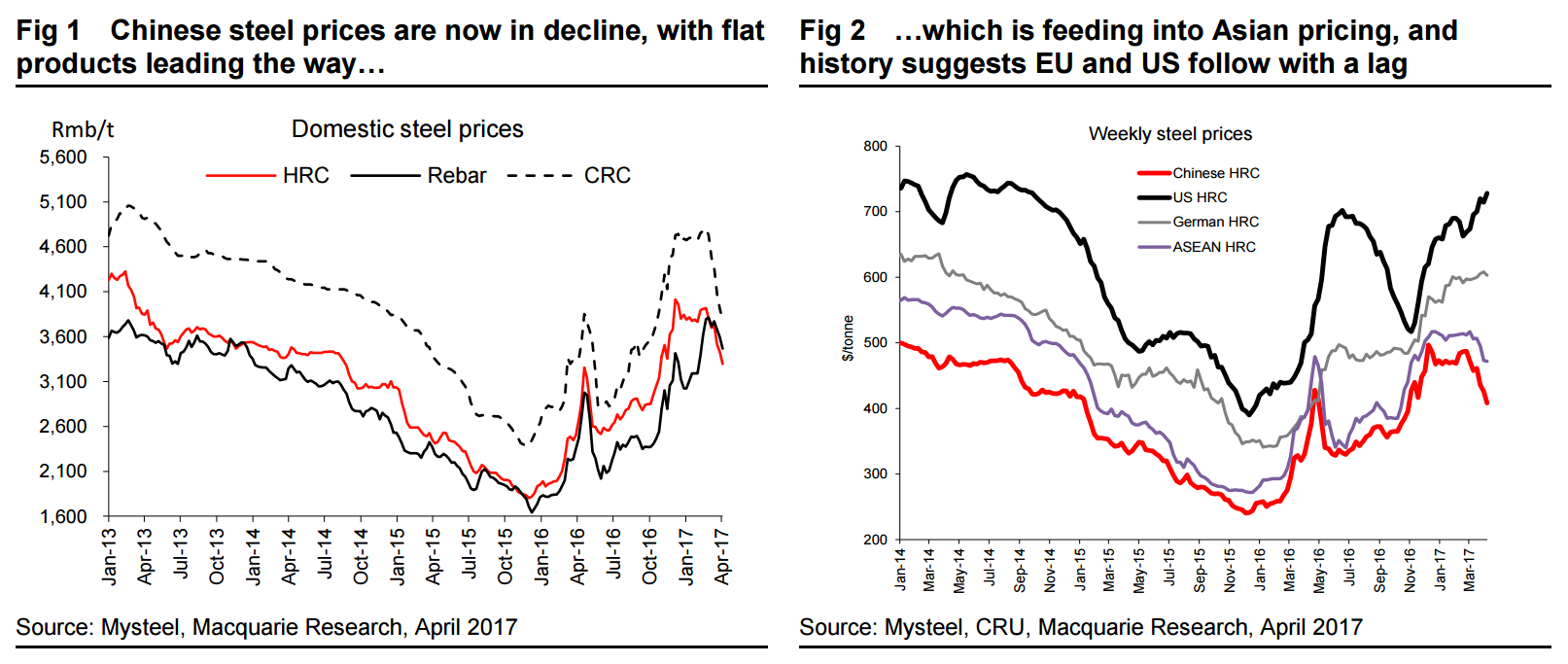

First up, the steel cycle:

Over the past three weeks, Chinese hot rolled coil steel prices have been on the retreat, falling >$50/t (~12%). This is now starting to feed into Asian prices, suggesting Chinese export volumes may be on the rise once more, and the natural chain of events is that EU and US prices will follow with a lag, though decent demand conditions and enhanced protectionism will still see these prices at a large premium to Asia. With expectations that Chinese construction demand, which remains robust at present, may also be dropping into mid-year, we look to have seen the peak of 2017 steel prices already.

Perhaps the wider issue is why prices are starting to drop now, as we enter what is traditionally peak season for demand. In our view, a major factor is the end of the restocking cycle seen through the Chinese and global industrial economy over the past six months, which has boosted apparent demand for steel and other metals. This is not to say underlying demand is bad – rather that it has normalised back to the ~+3% global industrial production growth rate seen at the present time after a restock-driven boost.

Following the great run up seen last year, Chinese flat product domestic steel prices had an extended plateau from late November to March. Meanwhile, rebar prices have been playing catch-up through the early part of this year. However, over the past three weeks domestic prices in China have been dropping – quite fast in terms of hot rolled coil and in particular cold rolled coil.

At the same time, global prices have generally been flat to up over the past two months. As a result, the arbitrage to export steel from China, which had been unattractive, looks to have opened up. Recent weakness in quoted assessments for ASEAN HRC suggests Chinese price weakness is now starting to infiltrate global markets. And when China has a problem, it does tend to spread through the world in the subsequent months.

The sudden drop in Chinese prices is considered a bit of a surprise, given the strong sentiment seen preceding and coming out of Chinese New Year. However, it has become increasingly clear that monetary policy in the country is tightening at the margin, with the liquidity tap would a notch or two back. In our view, this has changed sentiment towards future orders. Essentially, there is less confidence that order books for steel containing products will keep improving. And this has turned a steel restock cycle into the beginnings of a destock cycle.

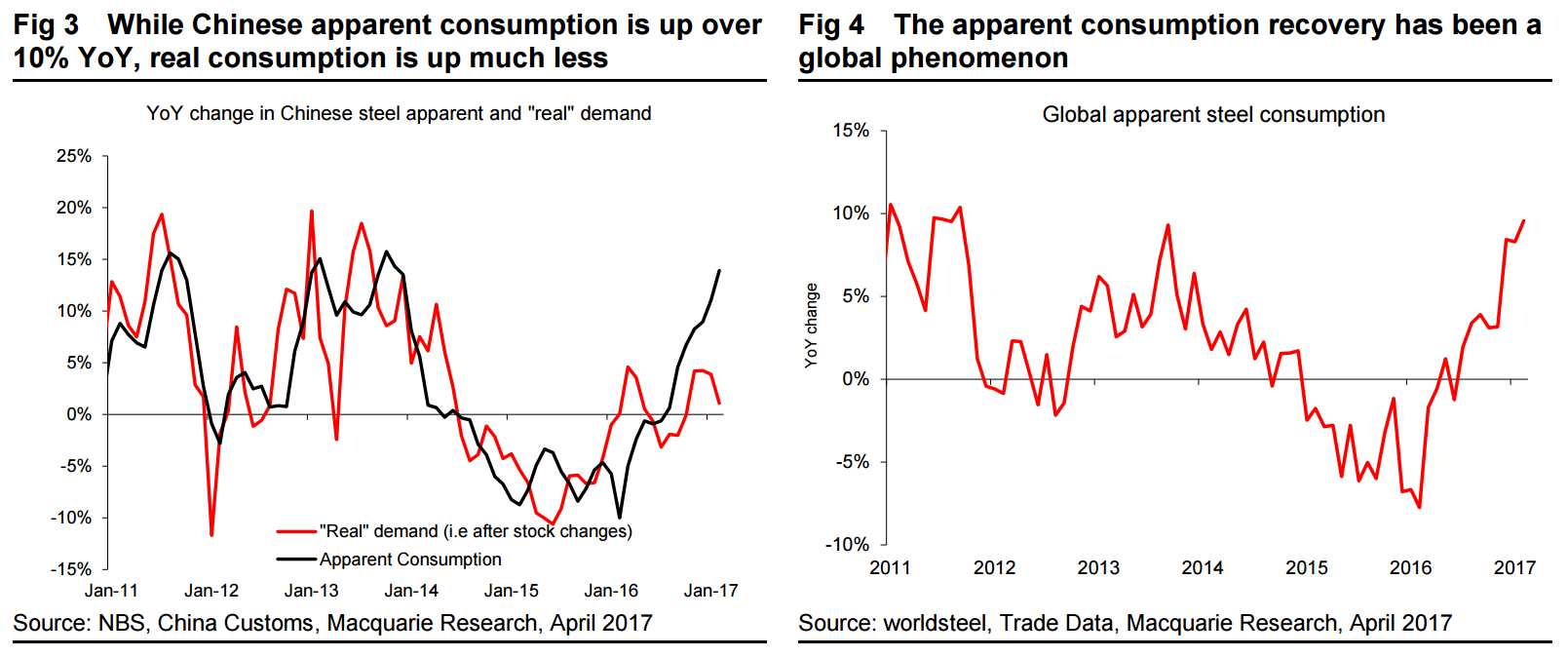

It is always hard to disaggregate the stocking element of steel and other metals, particularly in terms of downstream products. But given industrial profits in China started recovering aggressively over Q4 2016, it is fair to assume there was both a sustaining capital and inventory replenishment cycle in these areas over the past six months, particularly given the relatively ready availability of credit. As Figure 3 shows, Chinese real consumption (after adjusting for inventories) is up YoY, but not aggressively so. Helped by lower exports, apparent consumption in China is running up over 10% YoY over Jan-Feb.

This restock cycle may have started in China, but in our view has become a global phenomenon. With global industrials in a significantly better position than six months ago (and certainly a year ago) inventory replenishment has become the norm. Currently, global steel apparent consumption is running up ~10% YoY, albeit off a low base. However, just as China led the cycle up, it also looks likely to lead things lower.

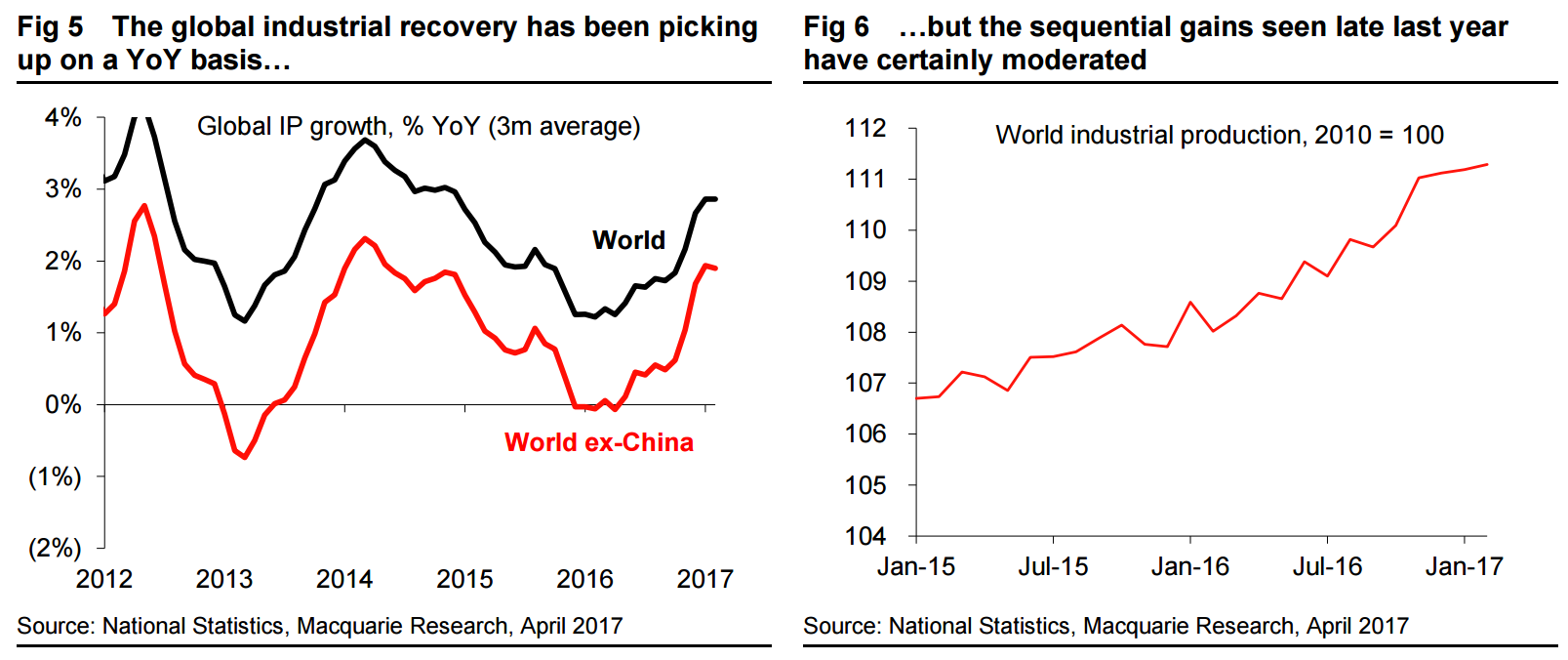

The end of restock is not to say the global industrial recovery is doing badly. On the contrary, this has continued into early 2017 on a YoY basis, with both China and ex-China recovering. However, in our view apparent steel demand has been running a little bit too strong for the underlying market conditions (bolstered by positive sentiment towards Chinese, US and thus global economic growth). We do however look to be reaching an inflection point here as well, with the strong sequential gains seen in H2 2016 moderating somewhat (partly owing to lower OPEC output). We do still expect sequential growth, but without the same aggression, hence the push back up the chain to steel.

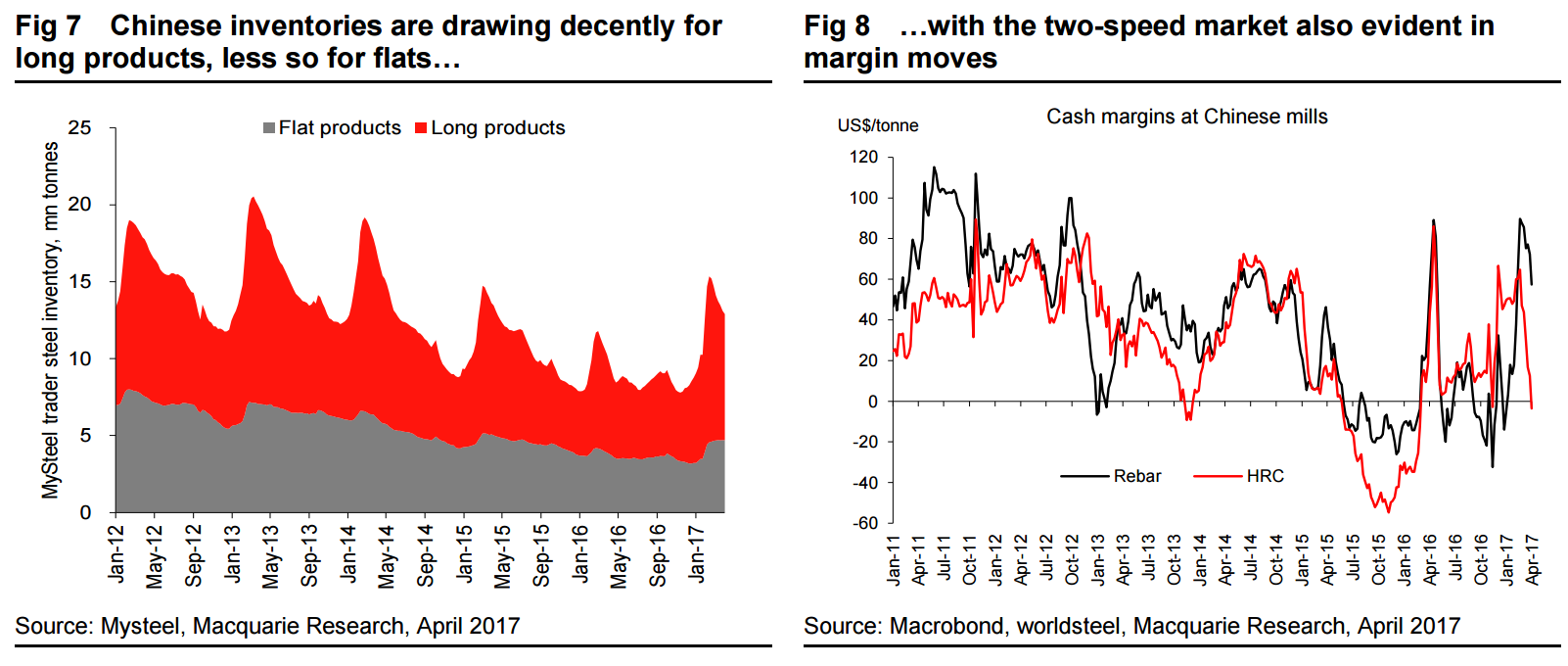

Inventories will thus help to tell the tale over the coming months. Currently, these have been building (both in steel and downstream products). We would expect a decline over the coming months, providing steel output reacts appropriately to falling prices. Meanwhile, our proprietary China Steel Sector survey due in the next fortnight will also give a good guide to changes in sentiment and orders. Interestingly, this showed a sequential weakening of orders in white goods last month, which ties in well with the more amplified cold rolled coil price decline.

It is important to note, however, that Chinese steel demand does look slightly bifurcated at present. Long product inventories at steel traders are still drawing down relatively quickly, while the rebar price is now trading above the HRC price. This reiterates the findings of our March survey that construction and infrastructure steel orders remain robust. Rather, flat products look to have the greater problem with traders clearly struggling to shift inventory, hence the gap lower in pricing.

This has an interesting read through for iron ore. We generally consider the smaller rebar producers as the marginal (and hence price-setting) buyer of physical iron ore. The iron ore price has dropped ~$20/t from the peaks, but this is more in line with long product prices, meaning only a small drop in margins. Flat product cash margins, however, are now trending negative. We reiterate our view that iron ore pricing will head to ~$50/t average for H2, but this large leg lower will only occur when Chinese construction activity weakens, hurting long product pricing disproportionally.

Very insightful and rational and, in my view, completely wrong. The steel cycle is described very correctly but this was no ordinary restock. It went mad on a combination of unusual inputs that led markets to extrapolate near-perfect conditions endlessly forward. That is, blow a big fat bubble:

Advertisement

moderate Chinese stimulus;

steel supply side rationalisation;

a major policy blunder in coking coal supply;

financialisation of dirt futures;

a falling yuan;

the election of Donald Trump, and

a very nasty Pilbara wet season.

These things triggered an huge ferrous complex reflation that fed upon itself and prices went up because prices went up. Now, as it becomes obvious that all of the stimuli were temporary, looking for some orderly unwind here is wrong. It’s just going to burst.

To wit, iron ore supply is literally gushing out now:

Advertisement

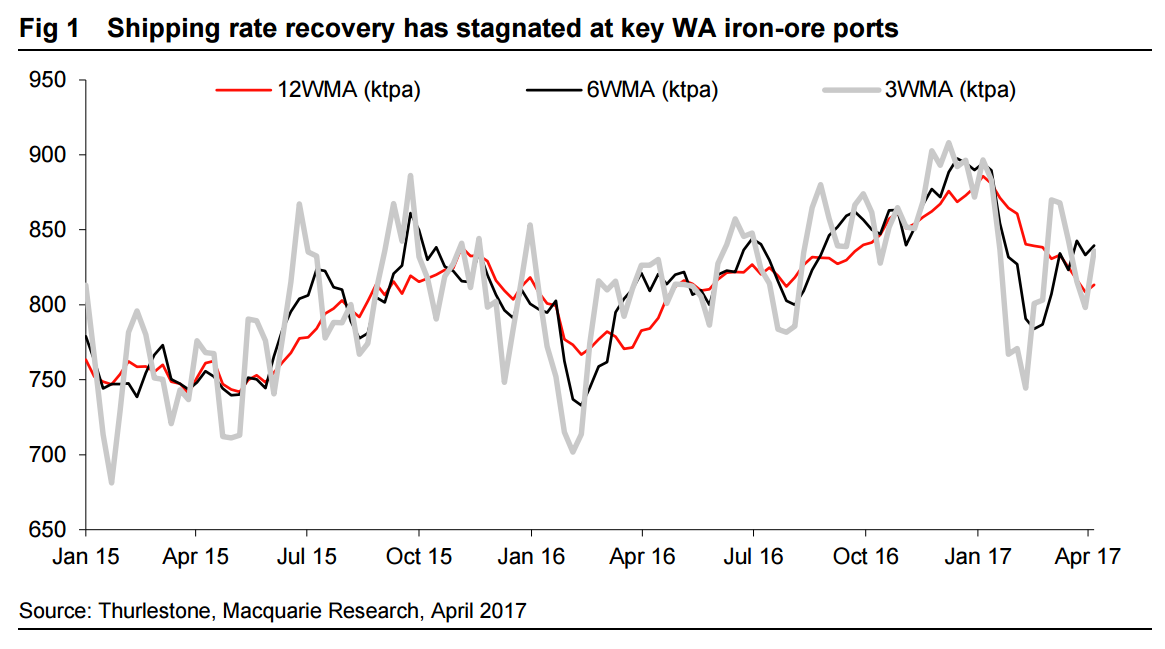

Shipments from key iron-ore ports in Western Australia have begun to recover, although at a slower rate than we had expected. We note that domestic iron-ore production in China has also begun to rise. Iron-ore prices are now down ~US$27/t from the peak to US$68/t, but remain well above our forecast for the 2HCY17 of US$50/t.

Shipping rate recovery underway but slower than expected: Macquarie’s latest weekly port data suggests that shipments from the key Pilbara ports has started to recover. In the past few weeks average shipping rates have risen to 835mtpa, still below the ~850mtpa run rate in the December quarter but well above the rain effected through in late January/early February of 730mtpa.

Recovery has been strongest for RIO and Roy Hill: The 125mtpa drop in shipping rates from the December quarter run rate to the late January/early February period was largely attributable to RIO and BHP, which accounted for ~100mtpa of the total. Since the trough most producers have recovered strongly with RIO’s shipping rate up 65mtpa and BHP and Roy Hill up ~20mtpa. We note FMG suffered the least from the wet season hence has had less ground to make up.

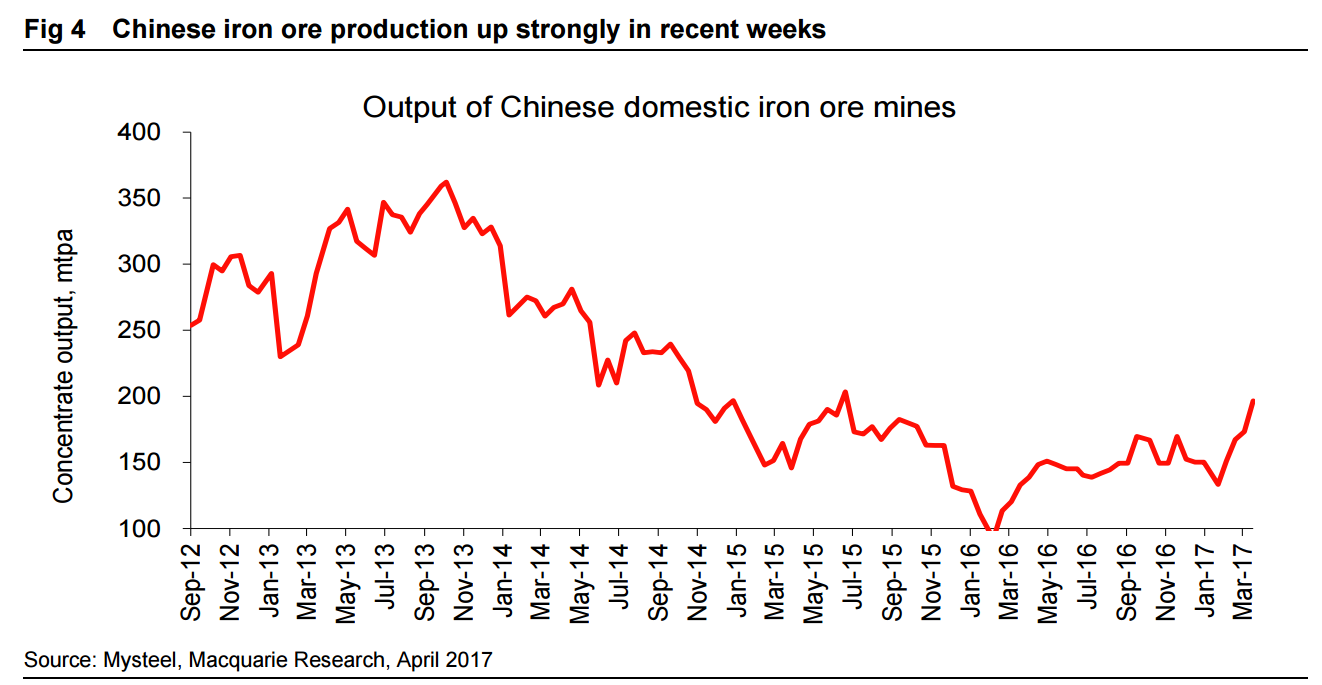

Iron-ore prices have declined as shipping rates have recovered: The recovery in the Pilbara iron-ore shipping rate coincided with iron-ore prices declining ~US$27/t from the US$95/t peak in late February to US$68/t currently. We note that Chinese domestic iron-ore production has also risen by ~50mtpa from previous run rates.

Guidance revision looks likely for BHP: The March quarter was tough with BHP, RIO and Roy Hill reporting material reductions in shipping rates compared to December quarter averages, with only FMG able to maintain its shipping rate. The recovery in April has been impressive although we still expect BHP to revise down its FY17 production guidance of 265-275mtpa to the bottom end of the range. FMG and RIO both look on track to hit guidance while Roy Hill has averaged an impressive 50mtpa for the past two weeks.

BHP, RIO and FMG look cheap under a spot price scenario: We note that the Australian iron-ore miners continue to look cheap on earnings multiples under a spot price scenario. At spot prices BHP and RIO are trading on EV/Ebitda multiples of 3.0-4.0x while FMG is trading on less than 3.0x. Free cash flow yields remain strong under spot prices, with BHP trading on 16%, RIO 14% and FMG over 20%.

Maintain Outperform: Iron-ore prices remain well above our ~US$50/t forecast for the 2HCY17 and beyond and the earnings upgrade risk to BHP, RIO and FMG remains significant under a spot price scenario despite the recent decline in prices. Accelerated debt reduction under a spot price scenario increases the potential for capital management surprises at the August results, particularly for RIO and FMG, and we retain our preference for these stocks for iron-ore exposure.

To this you have add Vale’s S11D and the possible return of Samarco, as well as rising India and African output and that the yuan has fallen 10% boosting Chinese iron ore competitiveness. And, as Macquarie says, Chinese demand is going to fall away in H2.

In short, new structural and cyclical supply is racing to market just as inventories brim at astonishing levels and demand peaks into a slowdown.

Advertisement

Not only is the cyclical froth going to come out, it’s going to segue straight into a return of the structural cost-curve shakeout of 2015 with all producers now fabulously efficient and deleveraged.

In all my years of tracking this market, I have never seen a set-up so bearish.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.