It has been a difficult few months in terms of positioning as the market has had extremely strong momentum in a short period whereas the underlying fundamental economic data has not been as conclusive, the subject of this newsletter. The Trump election resulted in acceleration in the global reflation theme which has brought into question the long-term bond bull market, much faster than we and many investors anticipated. Over these last few months (February included) we have been closing out the long-held structural longs on the portfolio whilst continuing to maintain some level of long volatility via short-credit positions, in which we have a high degree of confidence. We look to these positions to provide the portfolio protection and negative correlation to equities in times of stress.

Last month we took a look at the idea that the alternate economic views being put forward by a number of the new populist leaders, like Trump, should not automatically be considered as a terrible thing for economies or markets. This is because these alternatives at least have a chance of delivering upside against what the establishment offered, which is a continuation of the slow grind towards a world of worsening income inequality, perpetually climbing debt and a 100% chance of a devastating implosion at the point that the proverbial can could no longer be kicked. We argued that Trump and his old fashioned protectionist policies may actually be a positive for global production where countries compete on a more even playing field, reducing the rot that works from the inside out in destroying the way of life for the middle class. This rot has forced the electorate towards the political fringes as they seek answers and solutions to their plight which has resulted in an extreme level of partisanship. In turn, it has seriously decreased the quality of the media on both the left and the right as divisions have increased. The ‘us vs them’ attitude is far more pervasive than it ever has been, so it’s no surprise that such a polarising president was chosen at the last election, especially against a competitor that was the figurehead for the ruling class. The increase in the populist/revolt vote was enough of a difference to set in to motion this turning point in history.

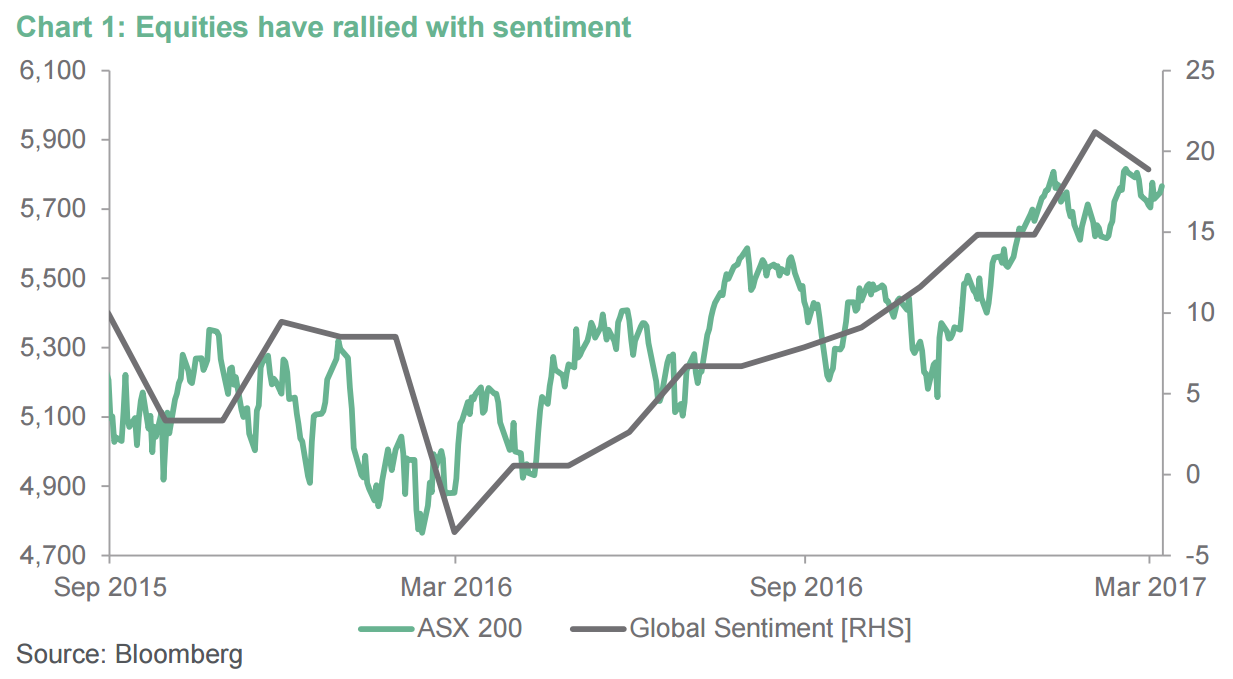

While the future is incredibly uncertain and economists and the public are still quite confused with what this shift represents and will mean for the future, the markets have swung wildly from pricing in secular stagnation to embracing optimism by believing in a full-bore ‘global reflation’. The evidence for the reflation theme is very compelling; global manufacturing surveys have all picked up, commodity prices have accelerated and have broken long term down trends, consumer and business confidence surveys have gone parabolic along with investment intentions, global trade has picked up and accelerated to levels we haven’t seen since the recovery out of the GFC, equities have risen to all-time highs, bond yields have risen, and as a result several central banks are now shifting from a dovish to a hawkish stance.

Most importantly however the global reflation and risk asset rally has driven volatility to new absolute lows, with capitulation evident in all short-volatility products. While easy to justify, these moves make us very uneasy and so I decided to dig a little deeper into the reasoning and drivers for the reflation we are seeing.

These economic data prints and market moves are all consistent with an economy that is going through ‘reflation’. Trump and his policies have been credited for the sudden upswing, but is this just coincidence? Have there been more important macro trends in play that were suppressed in the shadow of a US election which was the most bizarre in history? Challenging the ‘Trump-flation’ thesis is important as getting to the bottom of the trigger for reflation is the key to understanding its sustainability over the long-term, and if there isn’t sustainability over the long-term then we can make educated guesses at when the euphoria may end and markets will turn back towards the funk we had in the middle of last year.

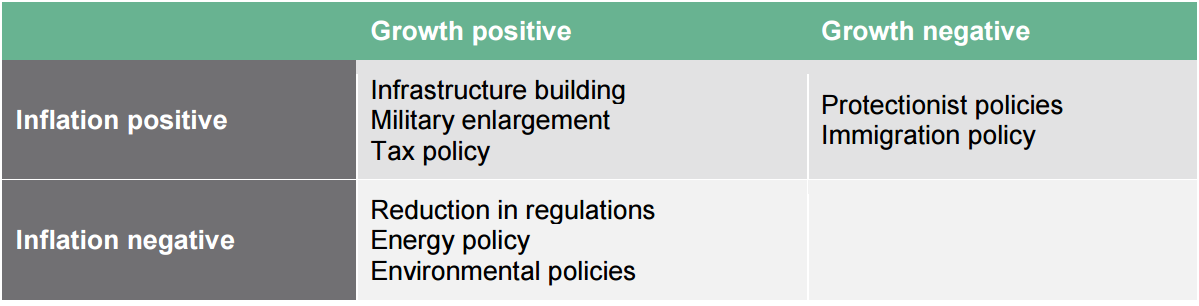

The first step is to look at Trump’s policies (from what we know so far) and determine if they are positive for growth and inflation. The table below shows our best guesses for what a selection of policies means for both growth and inflation. This is obviously highly speculative, but the market is working off the same information as we have in formulating its views so it is still worth the thought exercise. Healthcare was intentionally left out because we don’t think the Republicans even know what the game plan is there yet and so trying to bucket it at this stage is pretty pointless.

Optically the centre of weight of the effect of policies is definitely tilted towards pro-growth and pro-inflation, so it’s no wonder the market has traded like it has and built those expectations for the future. The other interesting aspect is that the class of policies that fit into each part of the table are very similar, with the pro-growth/pro-inflation group being all old-school Keynesian stimulus, pro-growth/anti-inflation being economic reform and antigrowth/pro-inflation consisting of closed border policies.

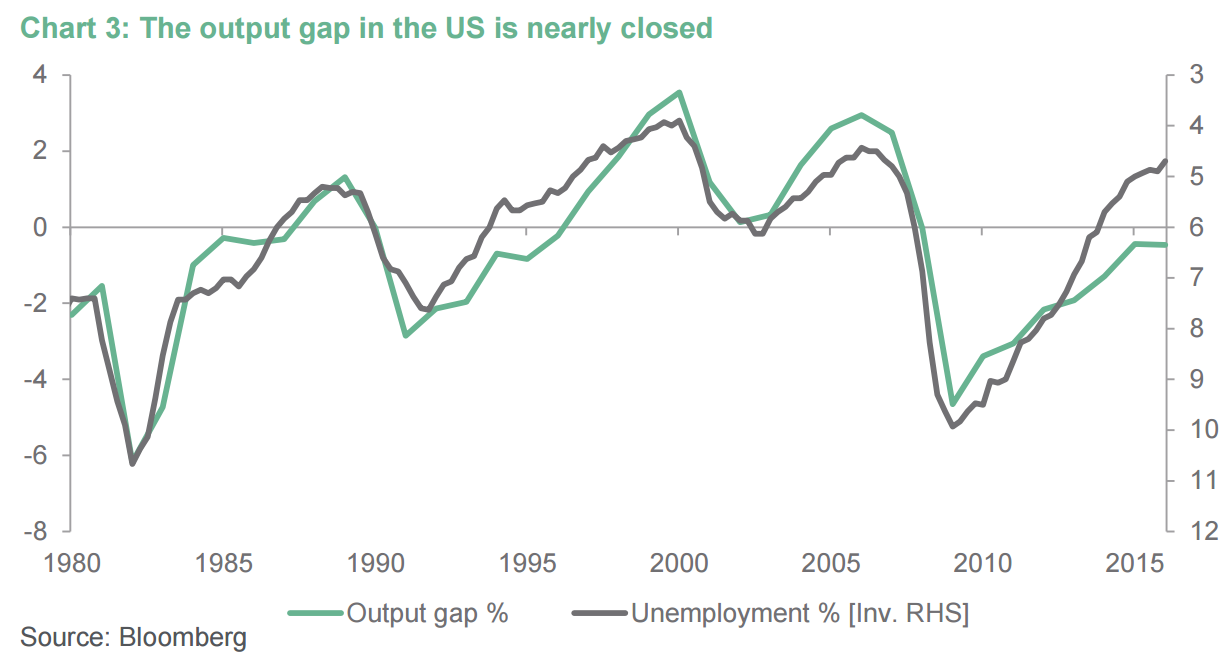

As is always the case, the stimulus policies will be limited by debt growth, however the corporate cash repatriation plan may be able to subsidise this somewhat. More debt is a drag on growth in the long-term (Rogoff and Reinhart) unless they can find projects which are a genuine contributor to productivity. This is difficult to achieve because the temptation of deploying on ‘shovel ready’ projects is so high, given the immediate flow through to employment and growth numbers (just ask the Chinese). So this group of policies will be more about short-term boosts to growth, with potentially more effect on inflation if they are deployed at a time when the output gap is basically non-existent and the economy is at full employment. This places the upside risk not to growth, but definitely more towards inflation.

The pro-growth, anti-inflation economic reform policies will drive growth by making it easier to do business (the US actually ranks fairly low on the ‘ease to start a business’ rankings due to excessive regulation, ranking at 50th between Cote d’Ivoire and Puerto Rico). Energy policy will lower the cost of energy domestically and environmental policy will slow future regulations that would have made it harder for US production facilities to compete on the global stage. This group of policies is a big switch away from the trend of ‘governing by increasing regulation’, epitomised by Obama, where the size and effect of government had been growing over the last 30 years.

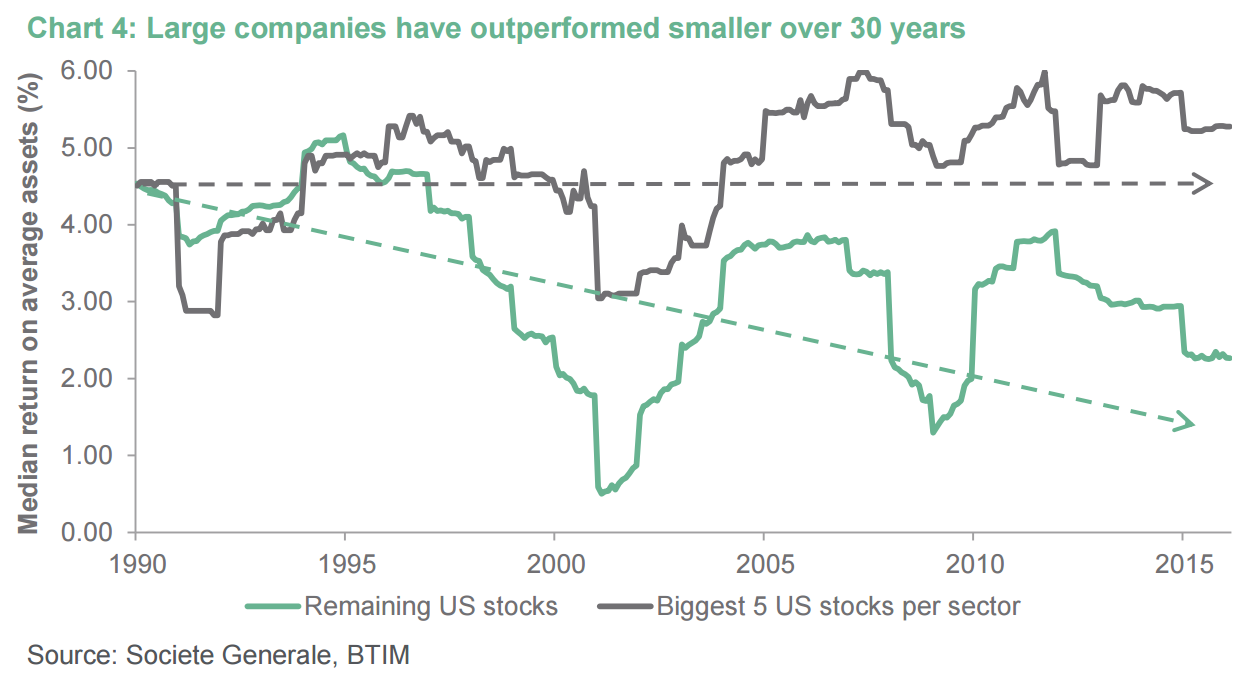

The increase in regulation could be one of the reasons why certain sectors are dominated by such large companies as the cost of regulation has put smaller companies at a significant disadvantage. This has created supernormal profits for the big companies which they have been able to perpetuate via lobbying. This trend has been strong again for the last 30 years and changes here should push small business to be a bigger contributor to growth in the future. Similarly all of these policies are also negative for inflation as they should reduce costs and increase efficiency. There is a good chance we’ve passed ‘peak regulation’ which would be a blessed relief for the economy.

Changes to financial regulation will have a considerable positive effect on the competitiveness of the US financial sector especially against Europe who continue to push profitability crushing regulation in the name of post-GFC safety. Early in March Deutsche Bank announced another €8bn equity raise, a good 10 years after the crisis. Increasing capital makes a company ‘safer’ but it also makes return on equity targets harder to hit at a time when their core businesses are being choked by more regulation. DB’s behaviour into and out of the crisis has been questionable, but at this point regulators will be cutting off their nose to spite their face as they essentially ensure the slow demise of a key cog in the workings of the European economy.

This leaves the group of policies which are the most contentious – immigration policy and protectionism. They represent the most radical change from the previous leadership, and in last month’s newsletter I went through the economic argument for why these despised policies may be required in the current world which has restricted the benefit of globalisation to a privileged few, and has been gamed by countries willing to conduct state-sponsored capitalism. Last month I also established that it has a high likelihood of being inflationary as the price of imports must increase, and if protectionism is successful at re-shoring jobs back in the US, wage inflation would surely follow as it is the whole point of protectionism in the first place.

If the Fed hikes because of this lift to inflation however, we should see the US Dollar rally which will work against the inflationary impulse. Surely interest rate hikes would cause growth to falter as well though, illustrating how difficult it is to even attempt to forecast such a huge change to how the global trade system works. There are a whole lot of unintended consequences that could arise from this, just like they did from globalisation, arguably a more theoretically sound framework which clearly didn’t deliver for a lot of people and has led to the mess that we find ourselves in now.

The assessment of what the growth impact should be unfortunately is not as ‘easy’. Successful re-shoring should spark economic growth through initially the investment required to build out the plant and equipment necessary for production, and then from increased consumption driven by strong wage growth. The reality will likely be a lot different though. Investment will still be necessary but this will only happen after consumption falls significantly because of rising prices. A hastily introduced Border Adjustment Tax or tariffs would raise prices within the US immediately, with no domestic substitutes available for many goods. Real GDP growth is based on volumes rather than value of consumption, and as such the hit to growth could be substantial, similar to how the introduction of the GST suppressed consumption in Australia back in 2000. Corporate profitability will be way down as well, again reversing the trends of the last 30 years, naturally holding back large wage gains.

Going back to our table it is clear that even though it is optically weighted towards being good for growth and good for inflation, evaluating the individual parts delivers a story that is very different. The bias towards higher inflation remains, but the upside to growth isn’t as clear. Add to this the probabilities of each change actually making it into law. For example, the economic reform policies are far more likely than fiscal stimulus, which is far more likely than the Border Adjustment Tax. You could even come to the outcome that the policies point towards lower inflation. Certainly the market is looking on the optimistic side currently but we feel the uncertainty should keep volatility elevated rather than crunching it to new lows, especially when you consider the current state of US growth.

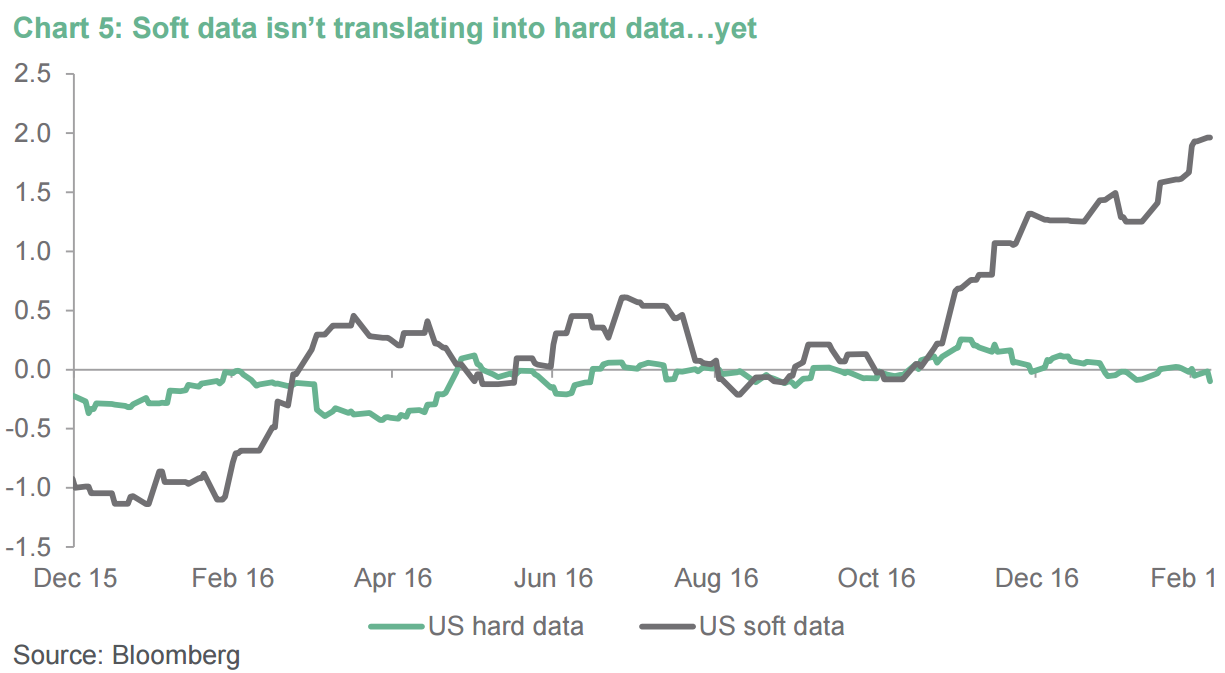

While survey data (called soft data), like manufacturing surveys and consumer confidence surveys have been super strong, actual economic data (called hard data) that follows into GDP growth calculations has been lacklustre. As a result, Q1 GDP estimate are now being revised down to the mid-1% level (from 3.5%), which will result in further deceleration of the yearly rate of GDP growth. Trump could well deliver or even over-deliver on what the market has priced in, but we have to wait and see, leading us to look elsewhere to identify if and when markets could possibly turn.

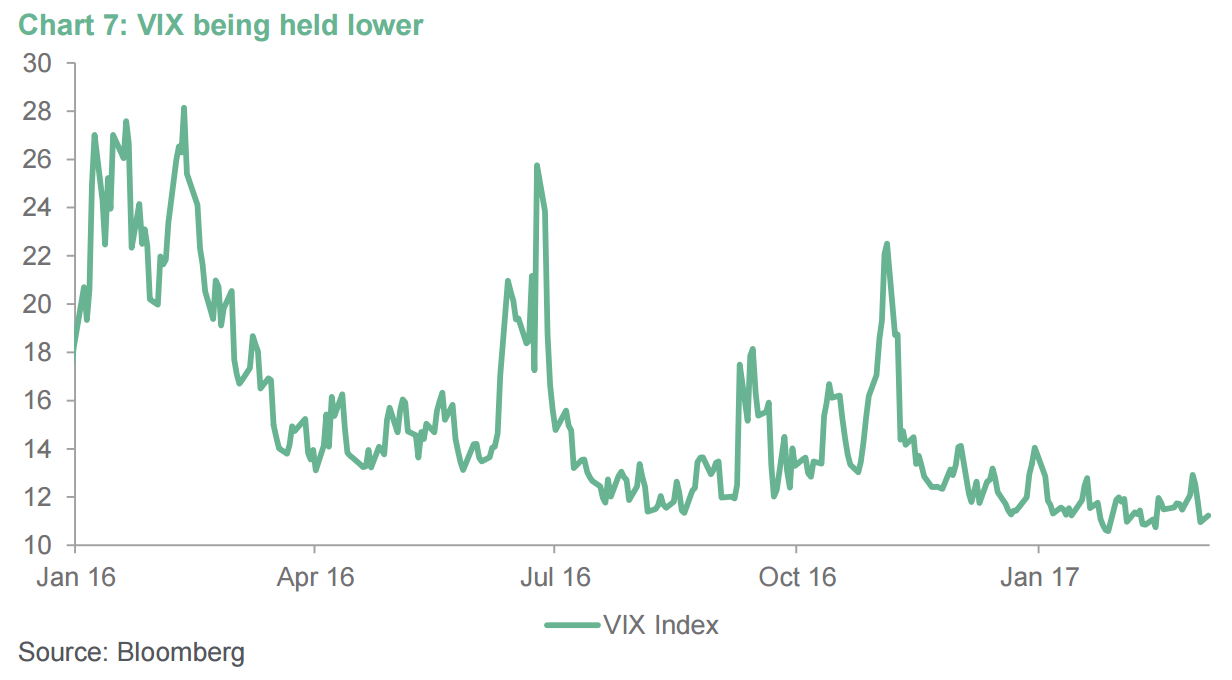

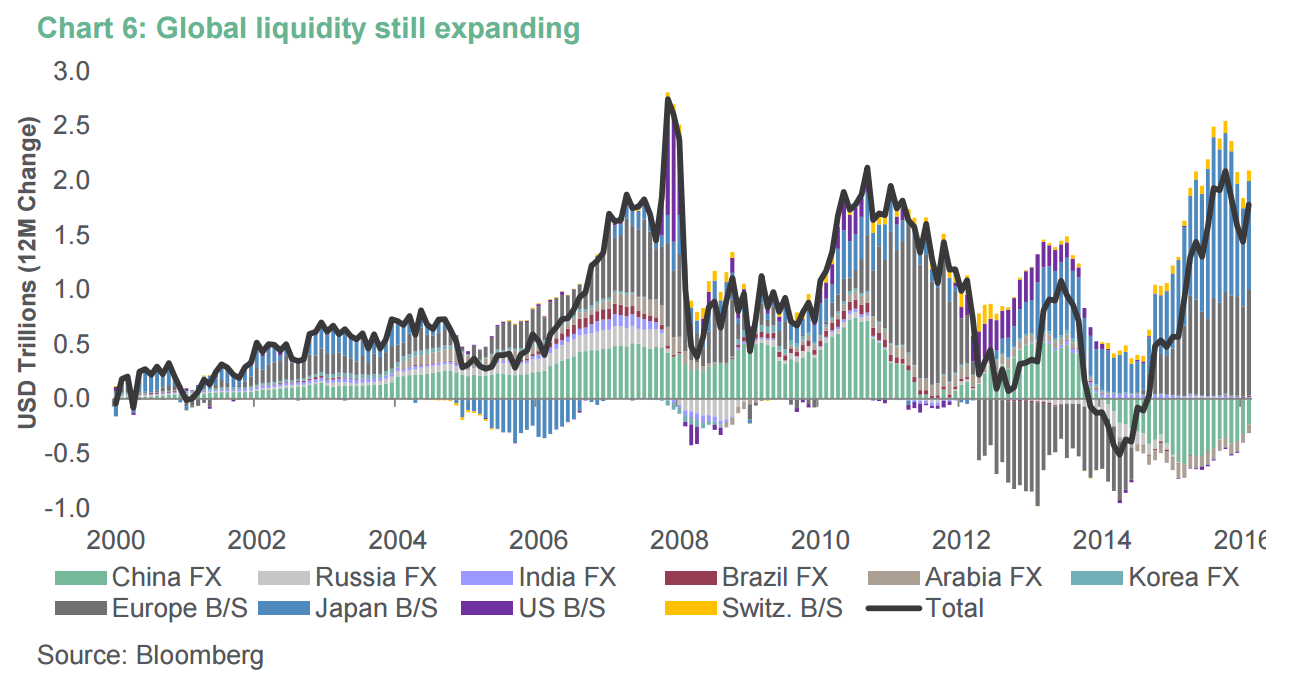

So if the Trump story doesn’t hold up, what else can explain sky high equities, super tight credit spreads and non-existent volatility? We’ve lived through these periods a number of times in the last 5 years, and every time the market was at a loss to explain risk asset performance at times when the risks to the macro background were so downwardly skewed. The answer was always “QE!”, with the expansion of global liquidity providing the buffer for markets to rally no matter what. The transmission mechanisms for QE are hazy but the link is definitely there, so it’s worth going back to our global liquidity chart to understand where we are at the moment in terms of global monetary accommodation.

It’s quite telling that we are still running at crisis levels of global liquidity growth, with a recent reacceleration being driven by the falling pace of FX reserve falls in China, and Switzerland adding to the giant packages continuing from Europe and Japan. The move towards the $2trn expansion of global liquidity started in late 2015 with another leg up after the ECB meeting in March 2016. This certainly lends credence to idea that the elevated volatility we saw in late 2015 and early 2016 was tempered by extraordinary monetary policy.

There were still risk events in 2016 after the bounce, namely Brexit and the US election. The spike in volatility measures around these events was incredibly short lived, and the incredible pace of accommodation helped to drive performance in risk assets. With such a strong force driving down volatility, key events like Brexit haven’t got a chance to break the downtrend in volatility if there isn’t an immediate crisis. Brexit was not an immediate crisis that led to recession or trouble in the banking system or a series of defaults, so the volatility it introduced was sure to be drowned out by what central banks have been doing.

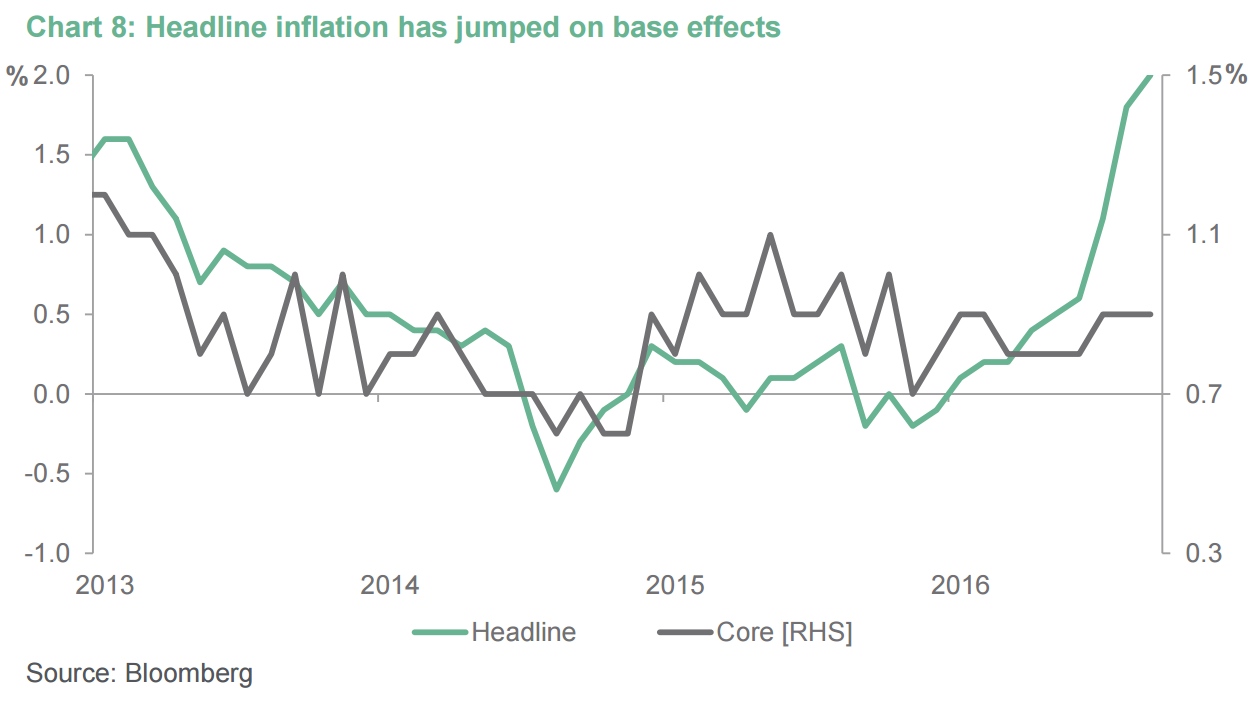

The central bank party is beginning to end though. The Fed has had an epiphany and is talking like they are behind the curve and both the ECB and the BOJ will have to make moves to slow or stop their programmes soon. The BOJ is staring down the barrel of a proper economic recovery and the potential for rising inflation, while the ECB’s issue is more acute as so much high quality collateral has been extracted and locked up that markets are ceasing to operate normally, leaving banks in vulnerable positions. The rally in headline inflation back to 2% (which is entirely due to the recovery in oil prices), masks core inflation that is still anaemic. This may still be enough for the ECB to give up on QE, who is already slowing the pace of purchases to €60bn from €80bn a month from April. The BOJ has already lifted the white flag with their pivot to ‘yield curve control’, which allows a much slower pace of purchases. The ECB could taper before the end of this year with a signal towards it coming much earlier, putting the current low volatility on notice.

There were still risk events in 2016 after the bounce, namely Brexit and the US election. The spike in volatility measures around these events was incredibly short lived, and the incredible -1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5 3.0 2000 2002 2004 2006 2008 2010 2012 2014 2016 USD Trillions (12M Change) China FX Russia FX India FX Brazil FX Arabia FX Korea FX Europe B/S Japan B/S US B/S Switz. B/S Total 10 12 14 16 18 20 22 24 26 28 30 Jan 16 Apr 16 Jul 16 Oct 16 Jan 17 VIX Index www.btim.com.au 9 pace of accommodation helped to drive performance in risk assets. With such a strong force driving down volatility, key events like Brexit haven’t got a chance to break the downtrend in volatility if there isn’t an immediate crisis. Brexit was not an immediate crisis that led to recession or trouble in the banking system or a series of defaults, so the volatility it introduced was sure to be drowned out by what central banks have been doing. The central bank party is beginning to end though. The Fed has had an epiphany and is talking like they are behind the curve and both the ECB and the BOJ will have to make moves to slow or stop their programmes soon. The BOJ is staring down the barrel of a proper economic recovery and the potential for rising inflation, while the ECB’s issue is more acute as so much high quality collateral has been extracted and locked up that markets are ceasing to operate normally, leaving banks in vulnerable positions. The rally in headline inflation back to 2% (which is entirely due to the recovery in oil prices), masks core inflation that is still anaemic. This may still be enough for the ECB to give up on QE, who is already slowing the pace of purchases to €60bn from €80bn a month from April. The BOJ has already lifted the white flag with their pivot to ‘yield curve control’, which allows a much slower pace of purchases. The ECB could taper before the end of this year with a signal towards it coming much earlier, putting the current low volatility on notice.

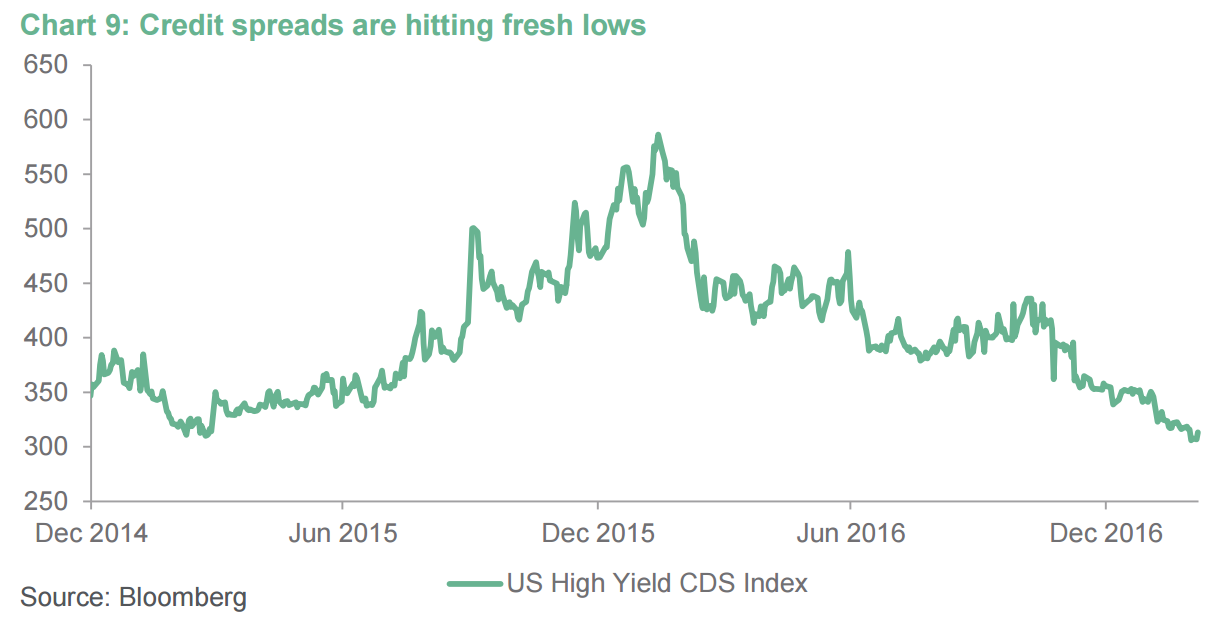

This leaves assets closely linked with volatility, like credit, at significant risk. After peaking in early 2016, US high yield credit (and credit in general) enjoyed a monster rally over the rest of 2016 and early 2017, hardly being phased by risk events around Brexit and the election. The fundamental backdrop for credit securities has been worsening for a while, but the technical bid has continued to drive spreads in. If volatility were to increase as we expect and monetary accommodation is removed we think these markets will be very exposed.

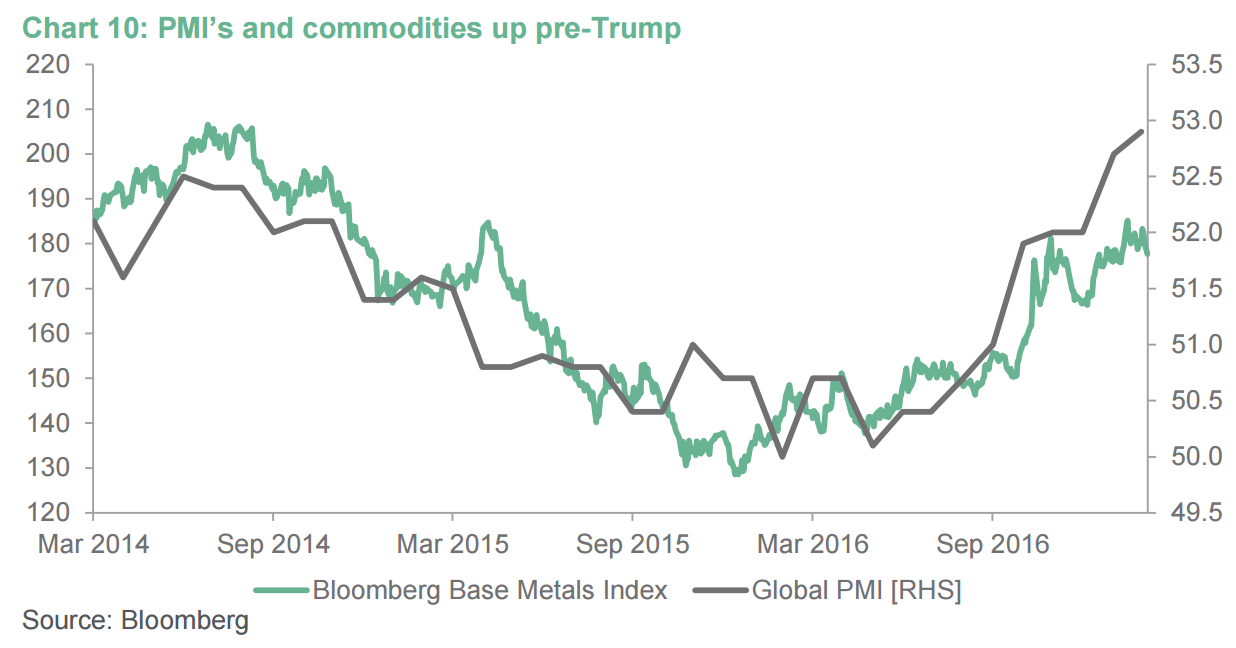

The liquidity theme may explain the performance of markets, but what about the jump in commodities and economic activity globally? Using a global PMI index that aggregates surveys from around the world, manufacturing activity bottomed in May 2016 and rose aggressively far before the US election, roughly around the time when the market had Trump pegged at a <15% chance of winning the election. In fact three quarters of the recovery in activity occurred before Trump-flation was even a term used by economists and strategists. The ‘Global reflation’ trade was already well underway due to another catalyst, and while the expansion of global liquidity was important, global fiscal stimulus was even more important.

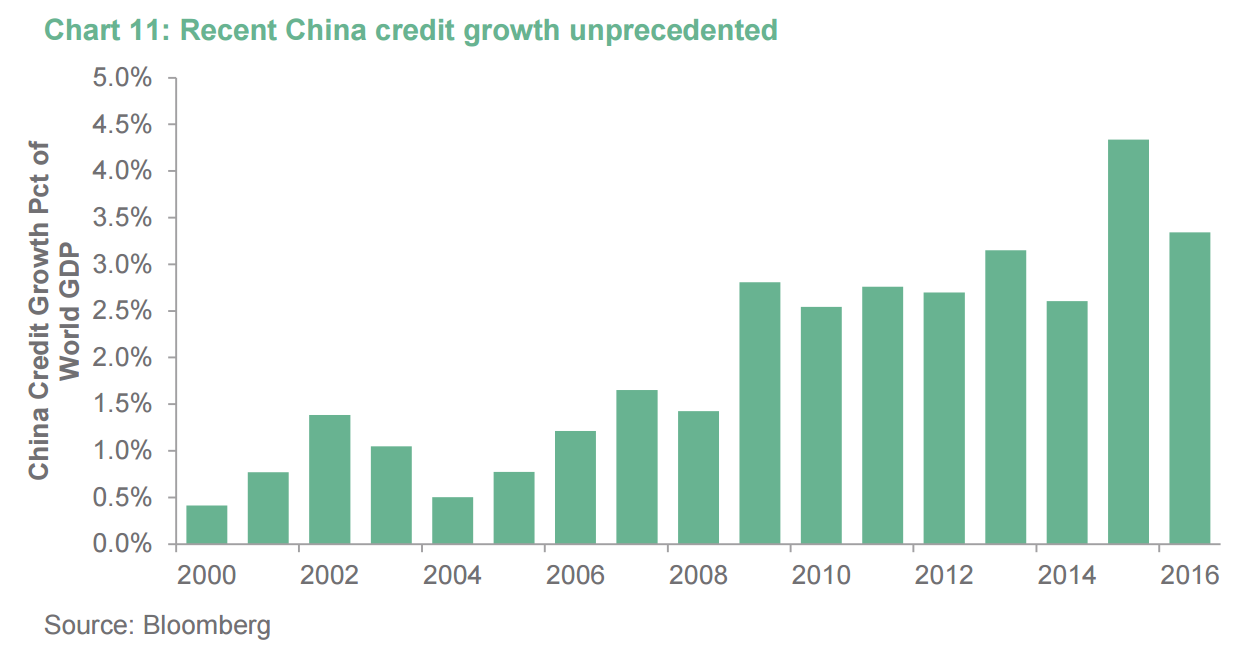

We have spoken previously about the pace of credit expansion in China over the last two years as being a major driver of the jump in global trade, activity and growth in 2016. The chart below highlights the scale of the expansion in a different way, as a percentage of world GDP.

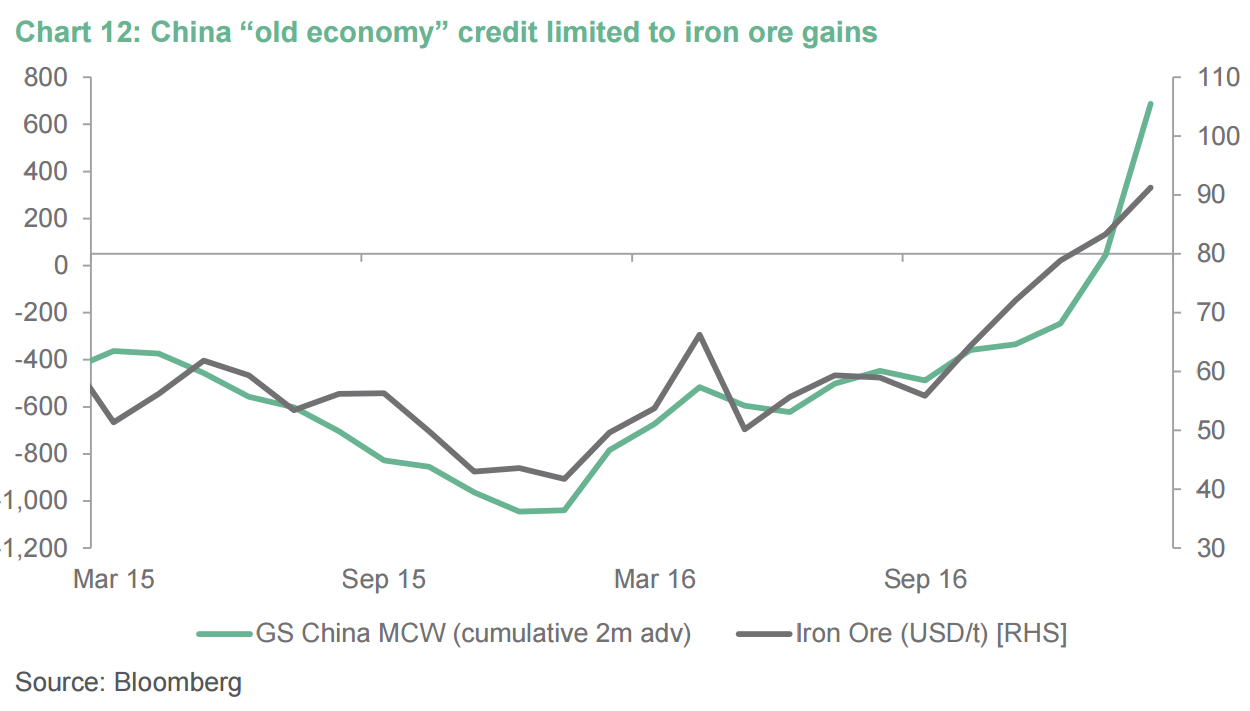

The credit expansion of 2009, credited with saving not only Australia’s economy but the world economy, registered at around 5.5% of GDP over two years. The most recent credit expansion (which really started in late 2015) over the last two years has accumulated to nearly 8% of world GDP. The magnitude of this cannot be underestimated, and the links to the recovery in key assets and commodities cannot be ignored. This pace of credit expansions obviously can’t continue for ever, so the positive effect of central bank balance sheet expansion has a limited life span. While headline credit growth has already turned in China, lending to “old economy” sectors (heavy industry) has accelerated more, and this provides a good lead on commodities once again. The Chinese National People’s Congress put a 6.5% floor on the economy’s growth rate in 2017. If 2016 achieved 6.7% with this volume of credit growth, there is no doubt the same feat will have to be repeated in 2017. Stability will be sought until the National Congress late this year when President Xi Jinping will look to solidify leadership for another 10 years throughout this important event. It’s unlikely that the economy will be left to falter before then.

The three factors – the expectation of Trump upside, central bank stimulus and Chinese stimulus – are probably responsible for the elation we are seeing in markets right now. This is an incredible cocktail for risk assets as liquidity is abundant and volatility should still remain low for as long as these three factors work together. There is a temporary nature to all of them however. For Trump the delivery has to meet or exceed the lofty expectations while the time lines attached to QE liquidity and the Chinese credit growth are far more finite, and cracks should start to appear from these effects subsiding by the end of this year at the very latest.

Until then however, we could be in a situation where equities still go up, volatility will continue to fall, credit will continue to tighten and bond yields may be higher than they are now. The Fed would have also probably hiked rates three times on current pricing, with the first scheduled for the March FOMC meeting (the Fed has delivered on all occasions since 1994 where the probability of an interest rate move has been greater than 65%). But as I said earlier this low volatility environment makes us very nervous as it is priced pretty much for perfection. Committing further risk capital to this time-limited upswing may prove to be a costly mistake in the future and may bring the down turn quicker than we expect.

Remember the commodity economies hiked rates as a response to bouncing commodity prices in 2009 which was a result of…record Chinese credit expansion. These central banks had to eventually reverse those moves less than two years later. The rules may seem different but they really have stayed the same. Bonds and long volatility strategies will still protect you in the times of risk asset stress, which seem so far away from everyone’s thoughts right now. Equity bull markets create a euphoric feeling and caution and hedges are thrown to the wind. It’s at these times that you need your protection most.

This is not to say that we shouldn’t price in a different future with Trump. It’s likely we are entering the third phase of the post-WWII global economy, with the first two being the Bretton Woods phase until 1970, and the globalisation phase after that. Each of these phases ended with a crisis. The last time we had a retreat in globalisation was in the period of 1914 to 1945, which was not the finest period in the world’s history. We sincerely hope we aren’t heading that way again.

In short, do not sell your bonds. We’re not!

Super as always. I remain a little more bullish on the US because I think Trump will deliver enough and along with the shale rebound it’ll enter a better growth phase for a little while. Subsequently crashed by the Fed.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.