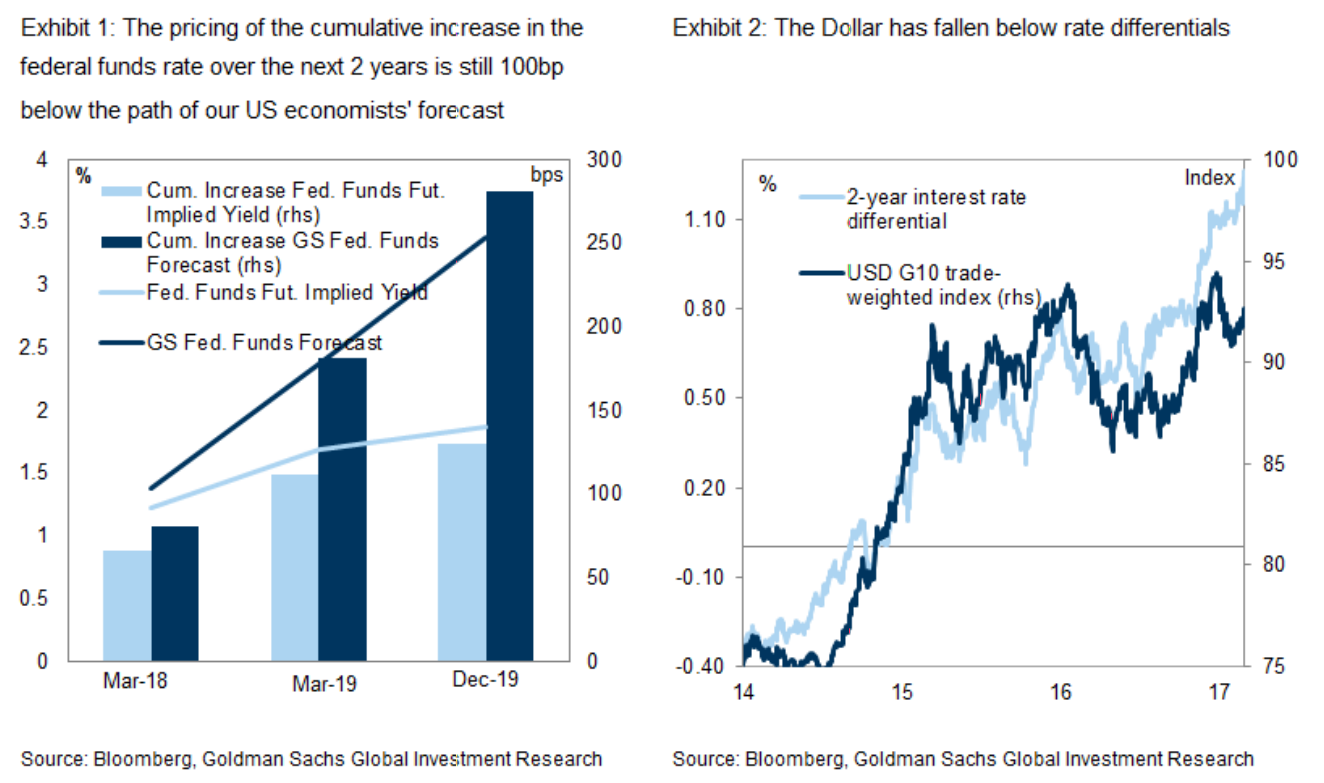

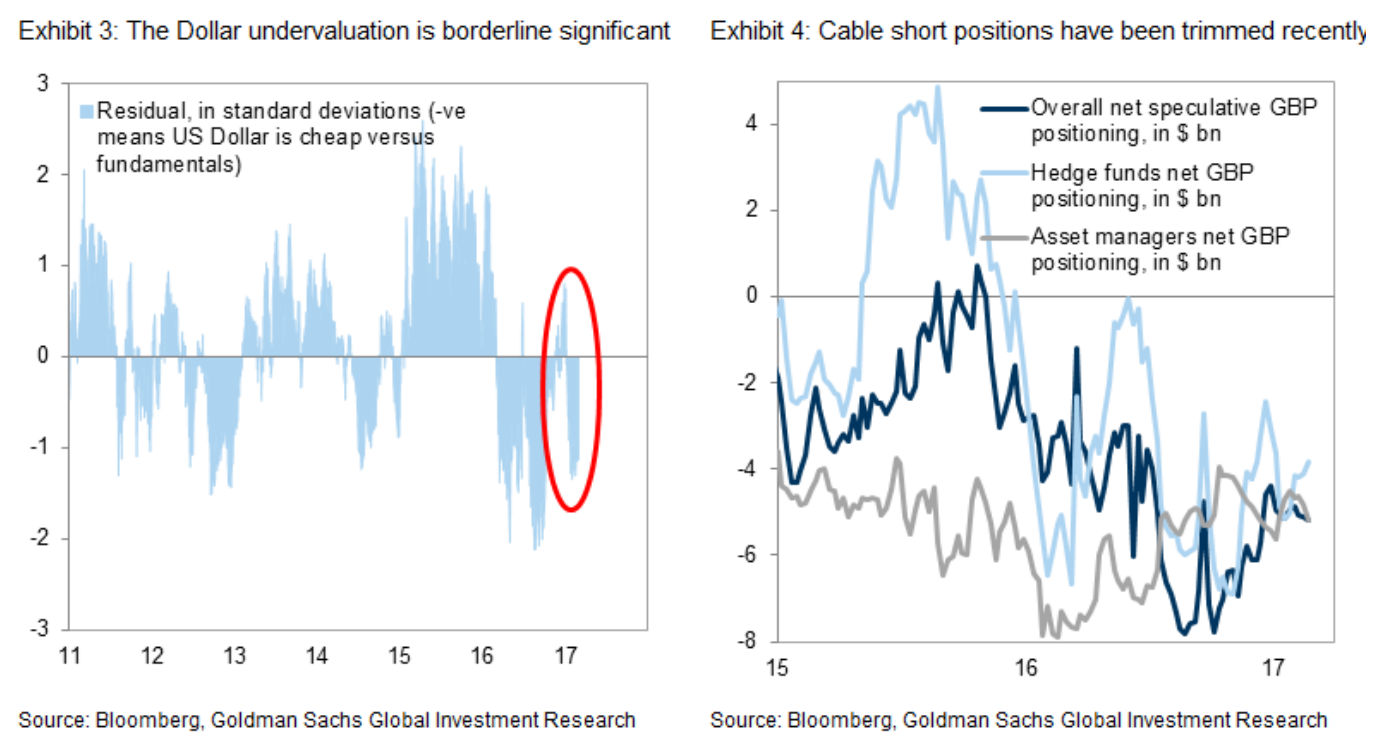

1. The USD is prone to a quick upside repricing if the FOMC were to hike the federal funds rate in March. Even though the market updated quickly the probability of a March hike, the pricing of the cumulative increase in the federal funds rate over the next 2 years has not changed much, and is still 100bp below the path of our US economists’ forecast. We would expect a March hike to lead the market to price two additional hikes in 2017 and three hikes in 2018. In the second half of the year, if data remain solid, the market could price four hikes over the following twelve months. As we have often discussed, the 2-year interest rate differential is what matters most for the currency and, based on our interest rate differential model, a 100bp increase in the 2-year USD interest rate translates into a USD appreciation versus G10 currency of about 10 percent, slightly higher than the 8 percent appreciation implied by our 24-months forecast.

2. From current market pricing, tactically and also taking into account political risk factors, our preferred short versus the USD is Cable, where the macro and monetary policy outlook in the US and UK, as well as political considerations, is pushing for a decline in Cable. For the EUR, better activity (see here), a mixed inflation outlook (a sharp repricing in headline but not much pressure on core CPI) and news on the French elections (see here) are pulling in opposite directions. Our base case remains that of a “muddling through” in the Euro area, which still supports our view of a lower EUR. That said, the tails of the distribution are quite fat. On the one hand, there is the potential for sizeable re-denomination risk to build up in the EUR and in Euro area assets if Ms. Le Pen wins the French elections (not our baseline case). In this case, the EUR would likely move below parity much faster than our forecast implies. On the other hand, EUR/USD could move into the 1.10-1.20 range if Mr. Macron wins and discussions around France’s willingness to cede some national sovereignty to Brussels in terms of more fiscal integration gain traction at the same time as GDP growth remains significantly above trend. Based on macro and monetary policy factors, on a 6-months horizon, USD/Yen has the strongest upside: core inflation is significantly below the BoJ’s forecast and we remain convinced that the BoJ will stick to the current framework and keep its word on delivering an inflation overshoot.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.