President Donald Trump on Tuesday signed an order to undo Obama-era climate change regulations, keeping a campaign promise to support the coal industry and calling into question U.S. support for an international deal to fight global warming.

Flanked by coal miners and coal company executives, Trump proclaimed his “Energy Independence” executive order at the headquarters of the Environmental Protection Agency.

The move drew swift backlash from a coalition of 23 states and local governments, as well as environmental groups, which called the decree a threat to public health and vowed to fight it in court.

The order’s main target is former President Barack Obama’s Clean Power Plan, which required states to slash carbon emissions from power plants – a key factor in the United States’ ability to meet its commitments under a climate change accord reached by nearly 200 countries in Paris in 2015.

Trump’s decree also reverses a ban on coal leasing on federal lands, undoes rules to curb methane emissions from oil and gas production and reduces the weight of climate change and carbon emissions in policy and infrastructure permitting decisions. Carbon dioxide and methane are two of the main greenhouse gases blamed by scientists for heating the earth.

“I am taking historic steps to lift restrictions on American energy, to reverse government intrusion and to cancel job-killing regulations,” Trump said at the EPA.

So, what will this change? Not much. Morgan Stanley rather conveniently explains why today:

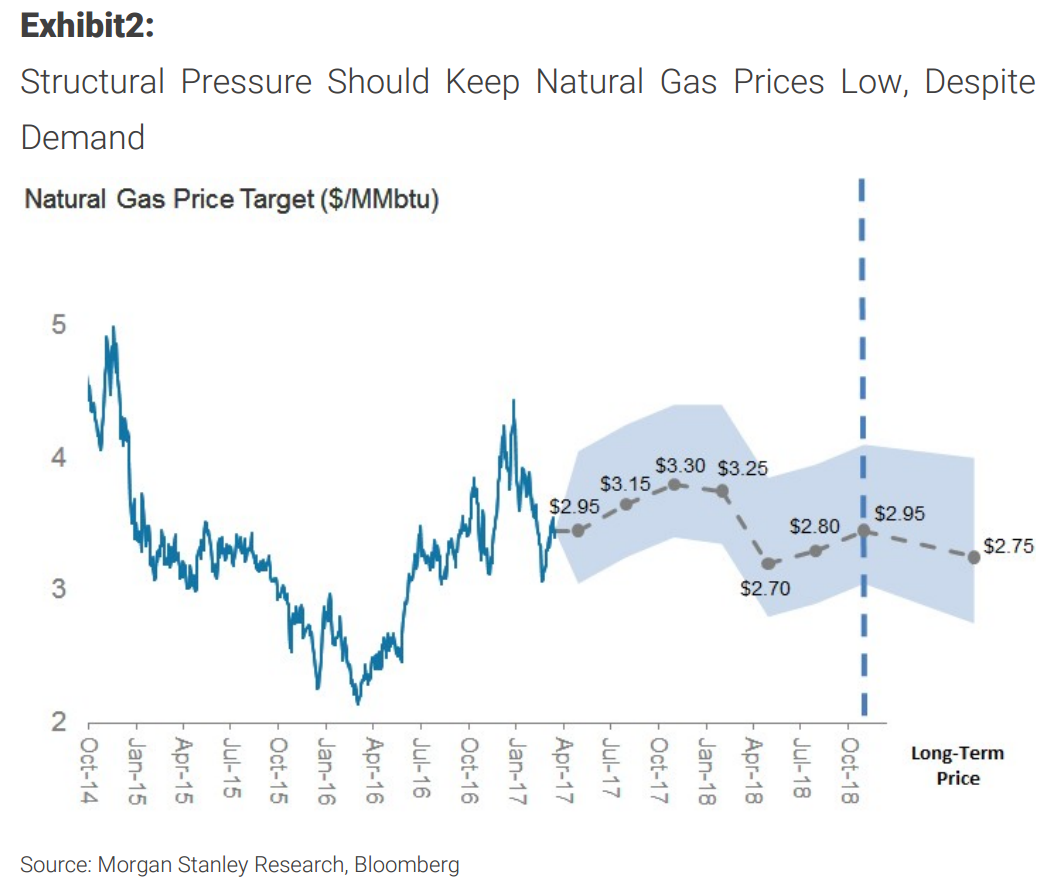

Natural Gas: Lower for Longer – Sub $3 Is the New Normal

Pricing pressure from oil, productivity improvements & power demand. For years the “bull case” for natural gas has been anchored in structural demand growth in the later part of this decade. That structural growth has arrived, and remains intact despite the negative impacts of yet another very mild winter. However, innovation across the energy sector has created several headwinds that should keep prices low. The most notable of these is a precipitous decline in breakevens for unconventional US oil plays. We expect improved oil economics, particularly in the gas-heavy sections of the Permian basin, to drive rapid growth in associated gas production, regardless of how low gas prices fall. On the gas side, capital productivity improvements have also taken hold, with breakevens across several key plays now well below $3/MMbtu. Lastly, in power, the end of drought conditions in the western US will allow hydro to displace gas. Longer term, declining electricity demand and growth in renewables gradually erode gas and coal generation needs. As a result, the window for the gas price bull case to play out is quickly closing. We are reducing our 2017-18 and long-term Henry Hub gas price forecasts, with a refreshed outlook driven by three key themes:

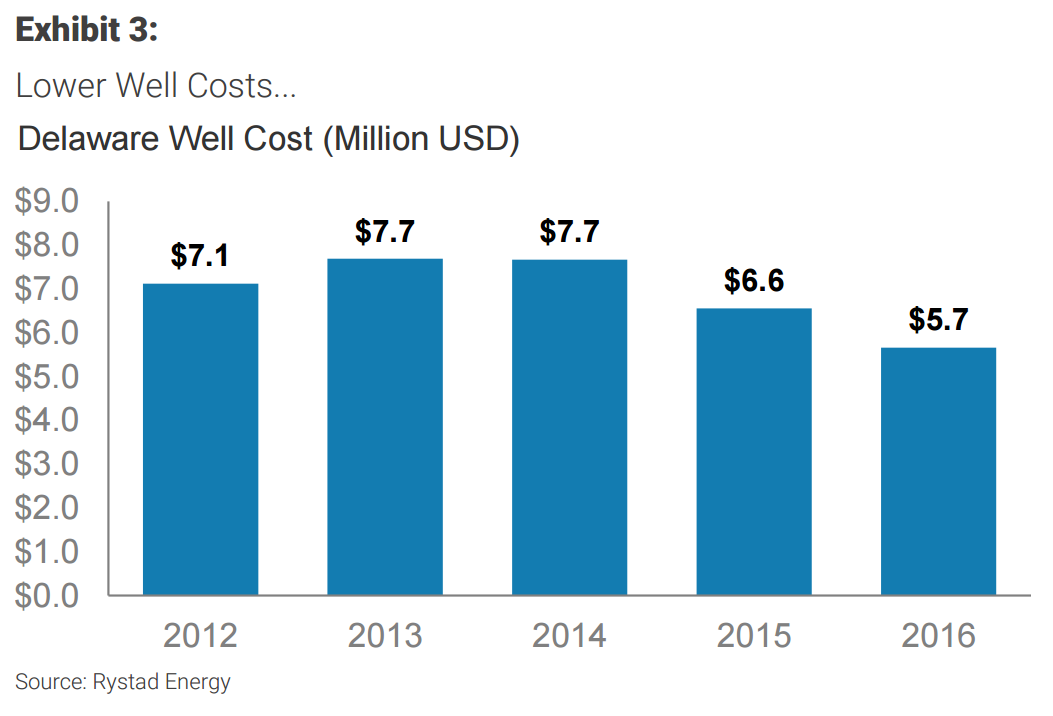

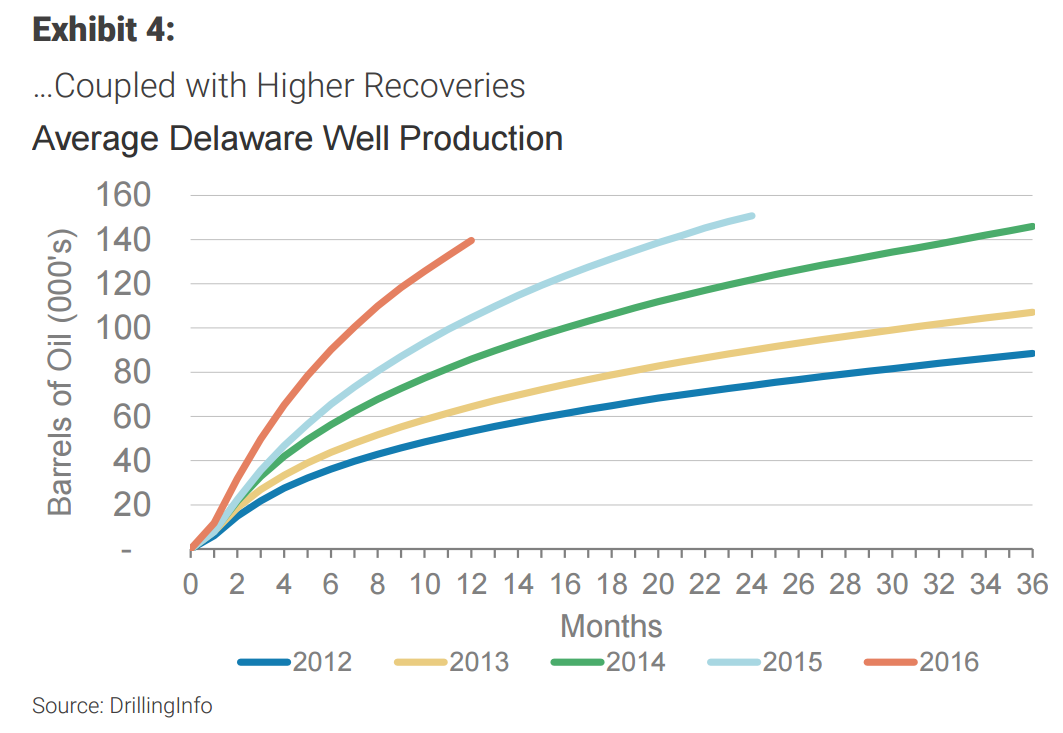

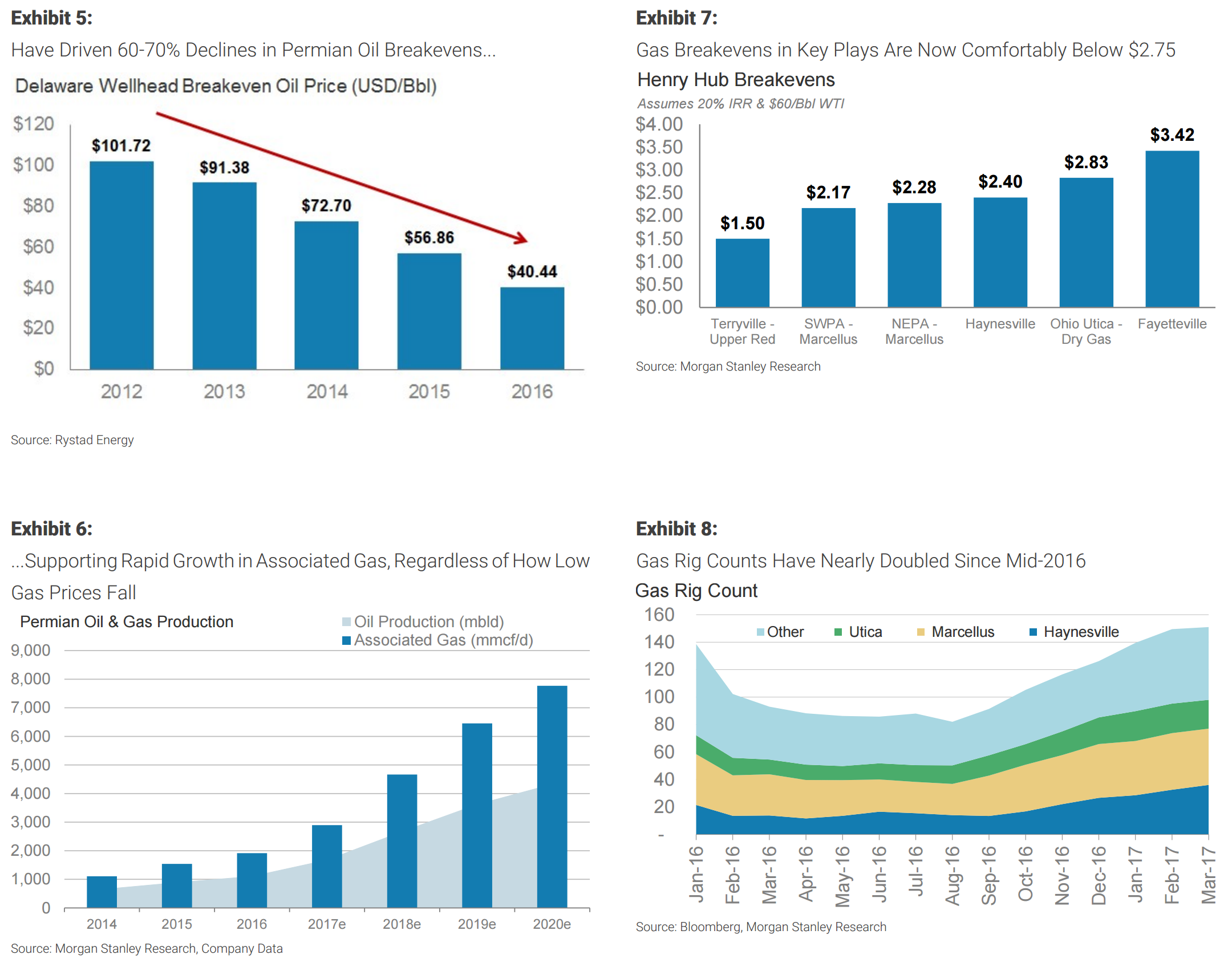

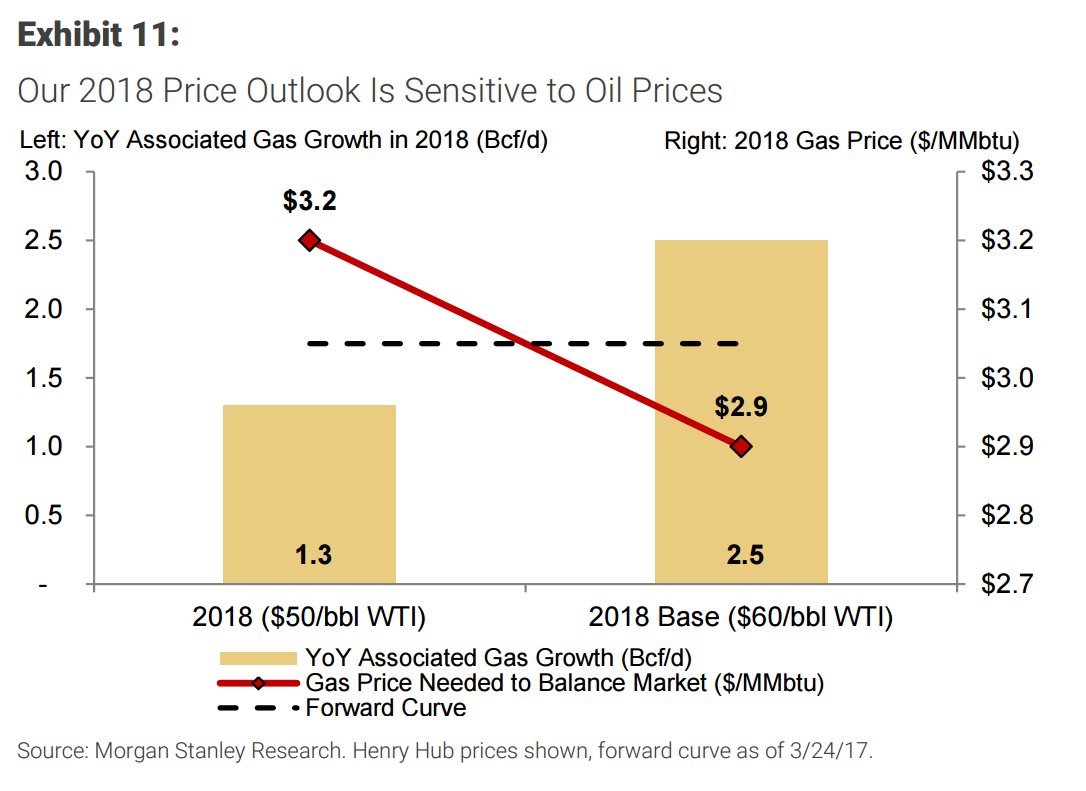

1. Oil: improving shale economics coupled with a stronger global oil market is negative for gas. Over the last several years, innovation has driven a substantial reduction in unconventional shale well costs while recoveries have moved higher. The result has been a precipitous 60-70% decline in breakeven prices for key shale plays. The most notable declines have been in the Permian in Texas, where 20-33% (lower in the Midland, higher in the Delaware) of the energy output is natural gas. In response to improved economics, rig counts have increased by 200, to 310, since mid-2016, with a shift into the gas-heavy Delaware. The result is substantial growth in associated gas, regardless of how low gas prices fall, plus potential periodic widening of local price differentials (basis) in the Gulf Coast region. In fact, by 2020 we expect total associated gas to grow by ~7.5 Bcf/day, led by the Permian and Oklahoma (STACK). This gas is roughly equivalent to all incremental planned LNG export projects, and is geographically close to demand growth in the US Gulf Coast. Our estimates incorporate $60/bbl WTI oil by 2018, in line with Morgan Stanley’s constructive oil forecast, and flat prices thereafter. That said, oil prices are a key risk to our call, as we see the two commodities as negatively correlated over the next few years.

2. Capital productivity improvements have meaningfully reduced natural gas supply costs. While recent gains have not been as impressive as oil, they are still significant. Shale breakevens have continued to trend lower, supporting production growth at lower prices. Even non-Appalachian plays have made significant gains, perhaps most notably the Haynesville (Texas & Louisiana), where breakevens now sit comfortably below $3/MMBtu. As a result, gas rig counts have nearly doubled from the lows seen in mid-2016. In the Haynesville, the rig count has tripled since September, and now sits at 35. Separately, substantial pipeline expansions in 2018 will support further growth out of low-cost basins in Appalachia, where breakevens range from $1.50 to $2.50/MMBtu. In aggregate, we forecast a reacceleration of dry-gas production growth on top of the glut of supply from associated gas, more than adequate to meet total demand growth between now and 2020 without higher prices.

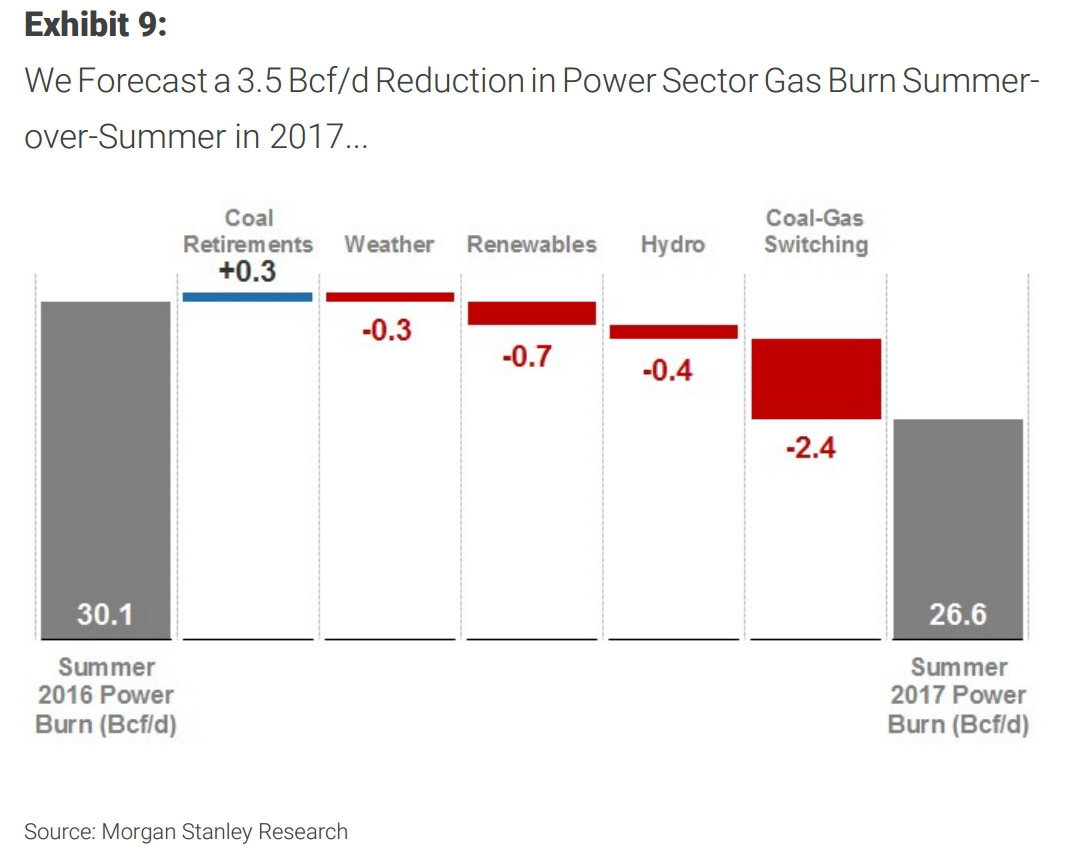

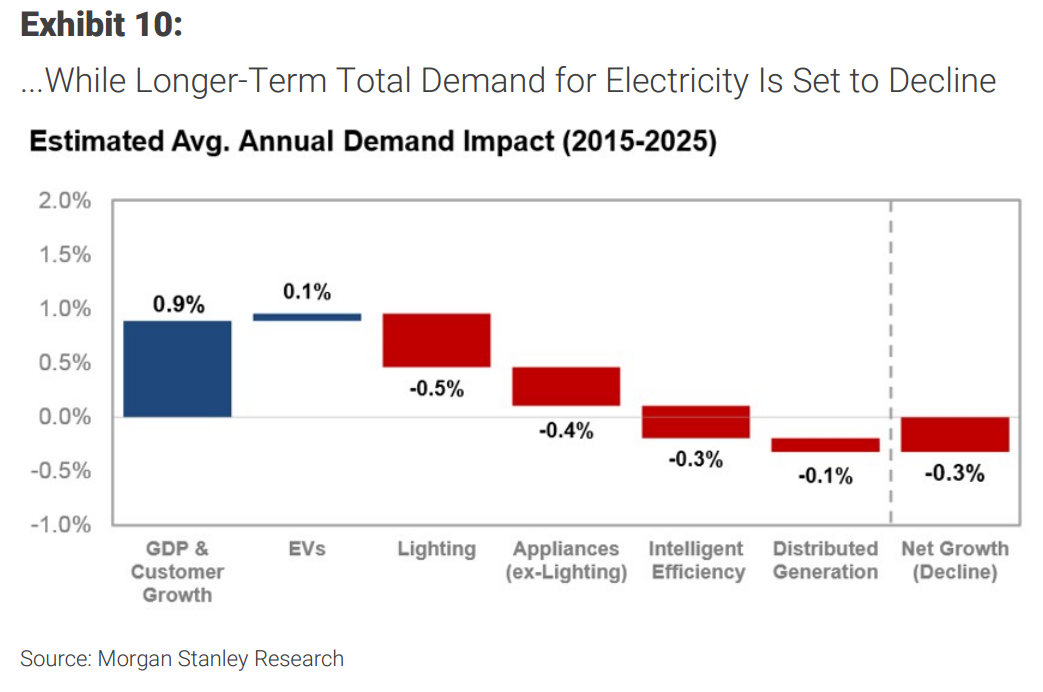

3. Power demand: mounting challenges. Gas demand from power generation remains a key balancing factor for the gas market. Going forward, total demand for electricity is not growing in the US, and in fact is likely to modestly decline. Our analysis of power demand indicates total US generation is likely to decline at a 0.3% CAGR 2015-25 due to energy efficiency, LED lighting, and rooftop solar. Gas is competing alongside coal and renewables for a shrinking pie of demand. In the short term (2017), the end of drought conditions in the western US should drive strong hydropower production, displacing gas. After years of drought, wet winter conditions have driven substantial increases in reservoir levels across much of the western US. Furthermore, snowpack in California’s Sierra Nevada mountains has now reached 180% of normal, creating a steady supply of additional water as melting occurs into the spring and summer. This will result in stronger hydropower production, which we estimate will displace ~0.4 Bcf/day of gas generation on average April-October. Longer term, renewables continue to take share from gas, offsetting much of the benefit from coal retirements. In fact, the lost gas demand from renewables year-over-year in 2017 (0.7 Bcf/d) is equal to the cumulative benefit from all announced coal retirements 2017-20. Lastly, we see downside to coal prices which could result in the need for lower gas prices to incentivize fuel switching (as coal becomes more competitive).

The Result:

Lower prices for longer: sub-$3 gas is the new normal. While the gas market remains tighter than recent history through late 2017, this dynamic is likely to be short-lived. Substantial growth in associated gas, led by the Permian Basin, will create a glut of low-cost supply near key demand growth regions in the US Gulf Coast. Beginning in 2018, pipeline buildout should unleash low-cost supply from Appalachia, narrowing differentials and pressuring Henry Hub prices. The biggest risk to our outlook, beyond weather variability (we assume normal weather), is further weakness in the global oil market, as it could significantly reduce associated gas growth. Short-term infrastructure limitations delivering associated gas from oil plays to demand centers is also a risk, and could drive a periodic expansion in Gulf Coast basis differentials over the next few years. That said, permitting new pipelines is relatively easy in the region, allowing any delivery constraints to be quickly addressed. We are cutting our near and long-term gas price forecasts:

2017: Yet another year of mild winter weather has loosened the supply-demand outlook for the balance of the year, eroding much of the near-term bull case for natural gas. We forecast average Henry Hub prices of $3.10-3.15/MMBtu for the balance of the year will be adequate to refill inventories. That said, the market remains much tighter than recent history. If rebalancing of the global oil market (and a resulting improvement in oil prices) doesn’t begin to occur, we believe gas prices could instead see a short-term rally into the mid- to high-$3 range by year-end. We expect any strength would trigger a meaningful supply response and be short-lived.

2018: By early 2018, pipeline expansions and an acceleration of associated gas production allows for low-cost supply to meet growth in demand. While early 2018 has the potential for high prices if additional infrastructure delays occur, our latest forecast calls for adequate pipeline expansion and production growth by January/February. We are cutting our forecast to $2.90, and expect prices to break into the $2.70-2.80/MMbtu by 2Q18, implying further downside to the current forward curve.

Long Term: cast by roughly 27%, from $3.75 to $2.75. The meaningful reduction in our outlook is driven by improved unconventional shale gas & oil economics and a substantial increase in Gulf Coast associated gas, which we now forecast will meet 60% of total demand growth through 2020. Net of associated gas, incremental supply needs are very modest and can be met with low cost Haynesville and Marcellus/Utica production without higher prices. Our We are reducing our long-term natural gas price foreM revised outlook assumes $2.25-2.50 prices across Appalachia. Higher levels of Gulf Coast production reduces the demand pull out of the region, allowing basis differentials to stabilize at a discount to firm transport costs. Our revised forecast is below the forward curve and what appears to be priced into many gas-exposed equities

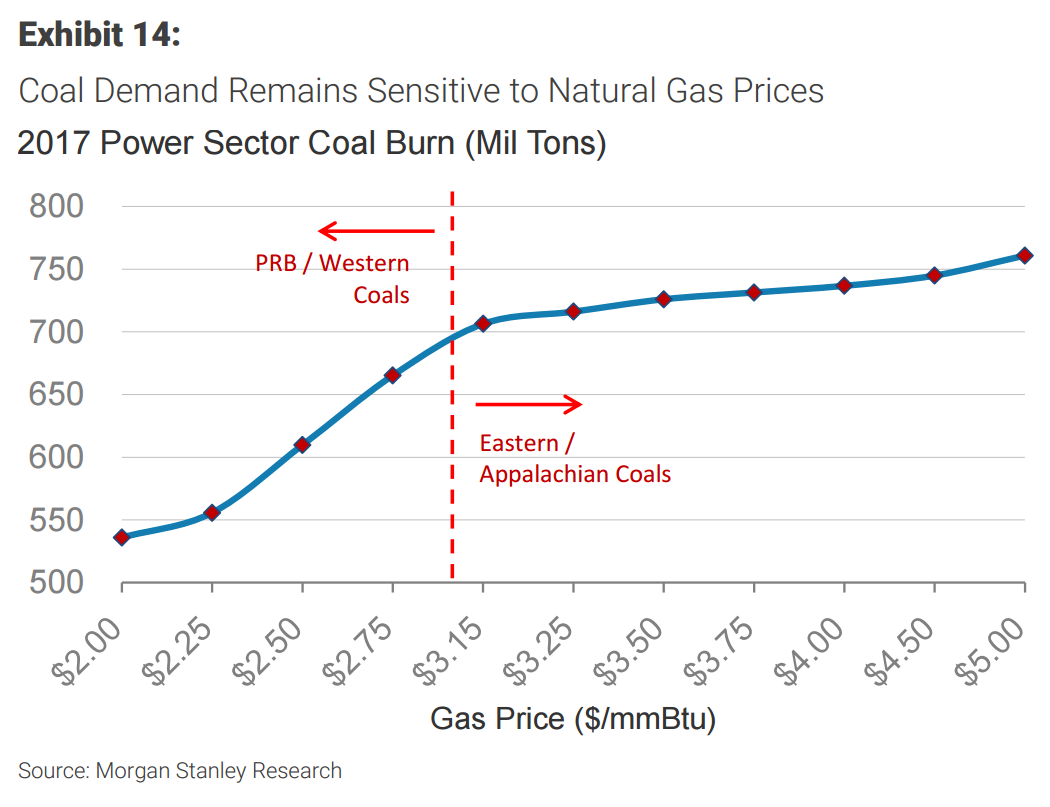

Coal’s structural decline expected to continue. We are cutting our 2017 coal burn forecast by ~28mnt, and now forecast only a 4% YoY increase in coal generation for the year, driven by higher gas prices. The majority of gains will be lost by 2018e due to ongoing competition from gas and growing renewables. Exports are unlikely to be a source of new demand due to challenged economics and state level permitting issues. Our fundamental analysis of power generation economics shows that longer-term coal simply cannot compete with natural gas or renewables (even on an unsubsidized basis), regardless of any changes made to environmental regulations. As a result, after a one-year increase in coal consumption in 2017e due to sequentially higher gas prices, we expect coal’s structural decline to resume, and see natural gas as a relative winner. Our updated supply demand estimates and price forecasts are in Exhibit 15 and Exhibit 16 , respectively.

Advertisement

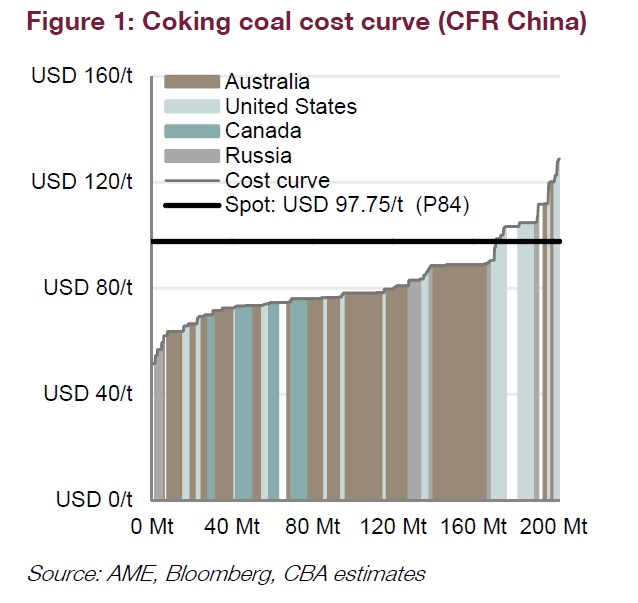

The one area that US coal might benefit, indeed already has, is coking exports where it is the marginal cost producer:

But even here the benefits will shrink over time as the ferrous complex returns to deflation.

Advertisement

Other than that, US shale is a coal killer and Trump making the former easier to extract only ensures the death of the latter.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.