The blogosphere is abuzz with Citi warning everyone to sell:

∎ Party like it’s 1999 — With spreads at post-crisis tights, equities making new highs, and new issues oversubscribed, markets are clearly exuberant. But could it be rational this time? We’re not convinced.

∎ It’s the stimulus, stupid — While the global economy is undoubtedly improving, we think market strength owes more to lingering global monetary and credit stimulus than to fundamentals.

∎ Cave Idus Martias! — While we’re not (yet!) expecting the equivalent of the fall of the Roman Republic, we are nevertheless very suspicious of the presumption that recent technical strength can continue. In a matter of weeks, the combination of a Fed hike, higher real yields, ECB tapering, reduced credit impulse from China and a renewal of European political risks could all leave the atmosphere feeling very different. Here are seven reasons we think you’re supposed to fade the risk rally – primarily in € credit but also more broadly

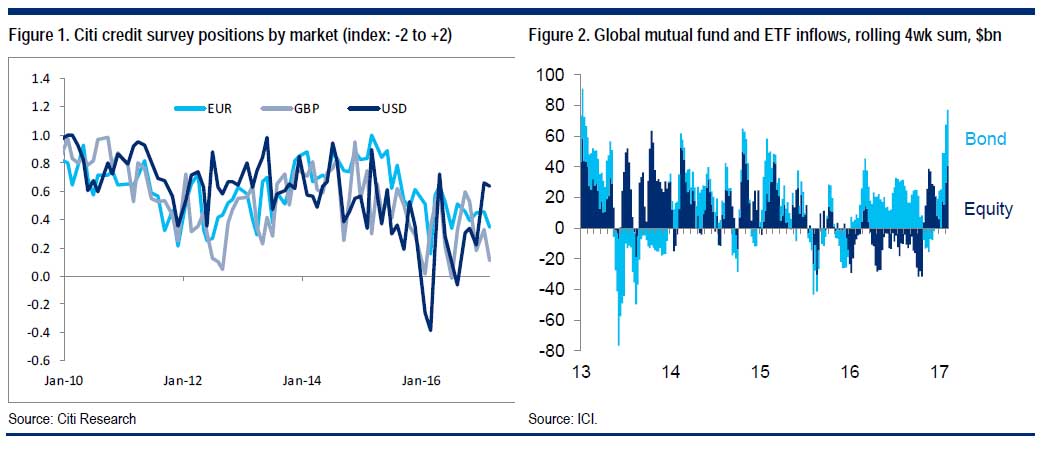

What’s a manager supposed to do when by early March your asset class has already exceeded your expectation for full-year returns? Take profit and take the rest of the year off, of course! And if it carries on rallying, go outright short! Yet somehow nobody seems to want to. Part of the reason is that the rally owes more to inflows and short covering than to institutional investor exuberance. And part is that the economic data do seem genuinely to be improving. But sell we think you should, not only in € credit (as we advised a couple of weeks ago) but also more broadly. Here are seven reasons not to trust your inner Trump: 1. The Fed may stop the inflow party Perhaps the best reason to remain long is that institutional investors seem not to be. The vast majority of the FI investors we have seen in recent weeks still believe in secular stagnation. To judge from our survey, overall positions have been creeping longer, but this is due overwhelmingly to positions among $ investors: those in € and £ credit have actually been falling (Figure 1).

Instead, the principal driver of investors’ buying seems to have been a response to mutual fund inflows. Not only equity funds but also bond (including both credit and EM) mutual funds have had their biggest 4-week run of inflows since 2013 (Figure 2). Numbers in Europe have been slightly weaker than the US-dominated global totals, but the pattern is similar. But while this too might normally be a reason for bullishness, we doubt that the current pace is sustainable. Quite apart from the historical inability to maintain this flow rate for long, there is the small problem of the Fed. While at this point a hike on March 15 has been so well telegraphed that it ought not to cause a 2013-style tantrum, we do think much of investors’ willingness to pile into risky assets stems from the lack of return on cash. Each and every additional bp in risk-free yield is likely to make investors think twice about the risk they are running in order to generate return elsewhere.

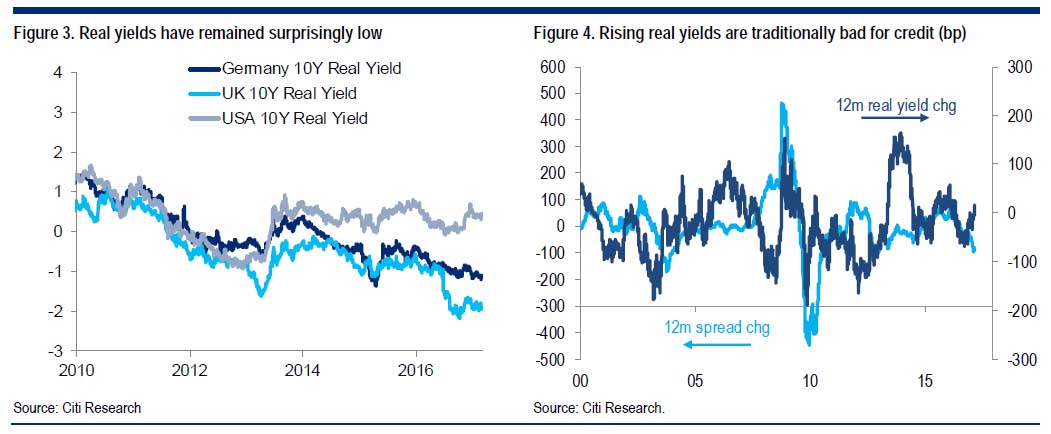

2. A rise in real yields should weigh on risk assets The second reason we think the rally has been so strong is that real yields have remained surprisingly low. Even as nominal yields have risen since the US election, almost all of the action has been in inflation (and growth) expectations (Figure 3). Traditionally this is positive for risk assets; in contrast, when real yields rise, it weighs on risk assets – albeit sometimes with a lag (Figure 4).

We suspect that what has made this move possible is the market’s willingness to focus on all the potential growth positives and yet shrug off the increasing signs of hawkishness from the Fed. Such a position seems increasingly untenable on two counts. First, rates markets have now finally adjusted to the new mood music from the Fed, and seem increasingly likely to be confronted with an actual hike; second, the rally in credit was starting to look out of whack even with today’s real yield levels, never mind following any proper adjustment to follow.

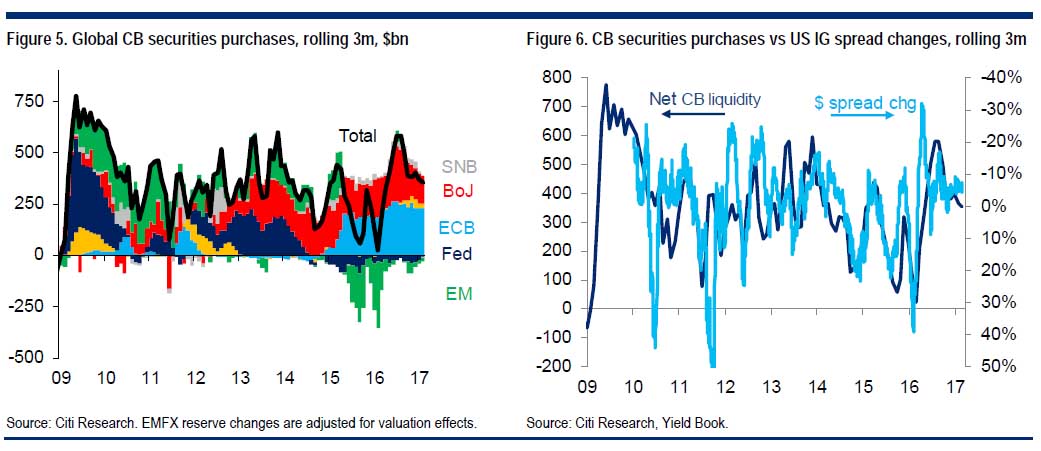

3. Central bank support is set to diminish Regular readers will know that our favourite model for markets’ behaviour in recent years is their correlation with central bank liquidity. While the scale of their purchases over the past half-year or so has been close to record highs, it is already diminishing, and set to diminish further (Figure 5).

BoJ purchases have almost halved since their shift to yield targeting; ECB purchases will be reduced by one quarter from this month on. In EM, FX reserves have held up well since February last year, and in recent months have been propped up as EM portfolio inflows have gone a long way towards offsetting a worrying trend towards net FDI outflows. But this too we suspect was aided by the Fed being on hold, and is liable to face renewed pressure as it returns to rate hikes. Besides, the extent of the rally once again seems excessive even for today’s level of CB purchases, never mind relative to its likely future trajectory (Figure 6).

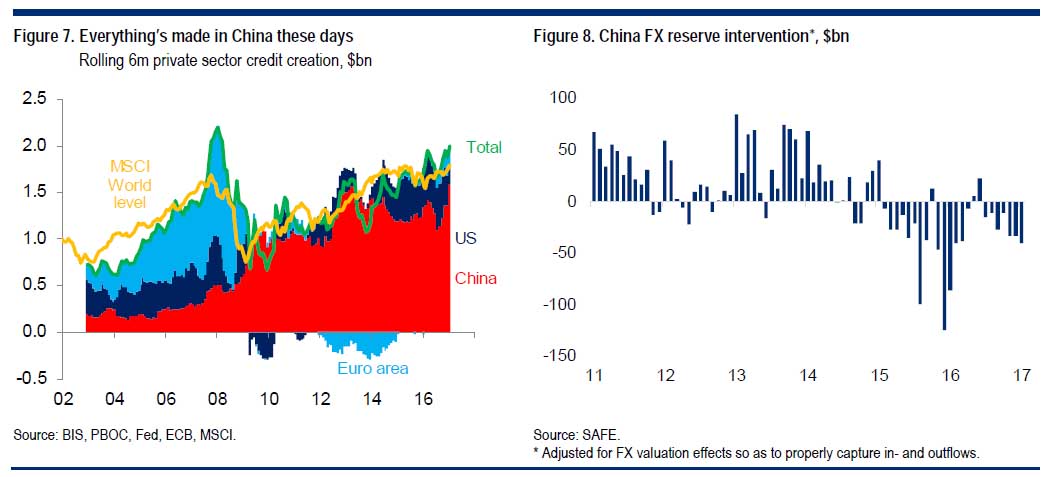

4. It’s the stimulus, stupid Continuing with the idea that market strength owes more to a wave of technical support than to fundamentals, we remain convinced that the recent explosion of credit in China – visible in the monthly total social financing numbers – is of greater global significance than is widely recognized. While this is hard to prove empirically, at an anecdotal level almost every place you visit from San Francisco to Sydney seems to be awash with stories of Chinese investment propping up prices. While most of this is in real estate (look at the recent agreement to sell London’s “Cheesegrater” to CC Land for over £1bn), we think the effects of credit creation spill over from one asset class to another, and increasingly from one region to another also. And fully 80% of the world’s private sector credit creation at present is occurring in China. The evolution of this global total bears at least a passing resemblance to global asset prices (Figure 7).

We confess we are still struggling to explain the theory as to why credit creation flows should correspond to asset price levels (as opposed to rolling changes) – suggestions welcome! One possibility is, of course, that the causation runs the other way round – with highs in equities driving credit expansion – but while there is doubtless an element of that, we’re not convinced that’s the whole explanation either.

But is this pace of credit expansion sustainable? We rather doubt it. Chinese numbers tend to reach a seasonal high in January as new lending quotas are granted but then to fall off sharply thereafter. And the positive impulse from the recent acceleration in credit creation in China will in any case be hard to sustain just because the absolute rate of growth is already so high. If anything, the recent tendency towards renewed FX outflows – even in the face of tightening capital controls – speaks to a reduction in demand for investment in China itself (Figure 8), itself encouraged by a series of measures designed to introduce brakes on lending, in the property sector in particular.

To our minds the wave of recent strong data in China, and associated run-up in many commodity prices which has itself fuelled optimism about a global reflation trade, owes less to a durable upswing in growth – and more to an unsustainable temporary resurgence in credit – than has been reported. Of course, there remains a possibility that US or DM credit stimulus is able to take Figure 9. UK and US household savings rate over even if Chinese stimulus wanes – and indeed, exactly such a hope would seem to be one of the drivers of both the rally and the improvement in much DM 16 survey data. It is exactly such a wave of borrowing and spending that has propelled the UK economy to the top of the DM growth charts in recent months, with the UK household savings rate falling close to its all-time lows (and the BoE expecting it to 10 fall lower still (Figure 9).

But while there is in principle room for household savings rates to fall elsewhere and 4 US create a new credit boom, perhaps aided by a Trump-inspired wave of global bank 2 deregulation, to us it seems unlikely. Outside the UK, household savings rates have 0 90 95 00 05 10 15 remained surprisingly high across the globe in the post-financial crisis era – even in Source: ONS, BEA places like Canada and Australia which did not experience a housing bust. Corporate balance sheets are already highly levered. Besides, the sheer scale of Chinese borrowing – $3tn/year relative to a mere $800bn in US and Europe combined – makes it difficult to see how these could substitute.

5. Just how strong are growth prospects really? But what of the counterargument to all this, namely that markets are merely responding to a marked pick-up in global growth prospects, sending secular stagnationists like ourselves scurrying for cover and raising the prospect of a longawaited return to ‘normal’ growth? There has, of course, been a pickup in both growth and inflation data, and indeed in corporate earnings. And we do buy the argument that, while corporate capex has been weak relative to profits and to GDP, in outright terms it is not perhaps as moribund as pessimists (ourselves included) sometimes make it sound. But we are much more skeptical of the likelihood of a continued and self-reinforcing cycle of growth from here.

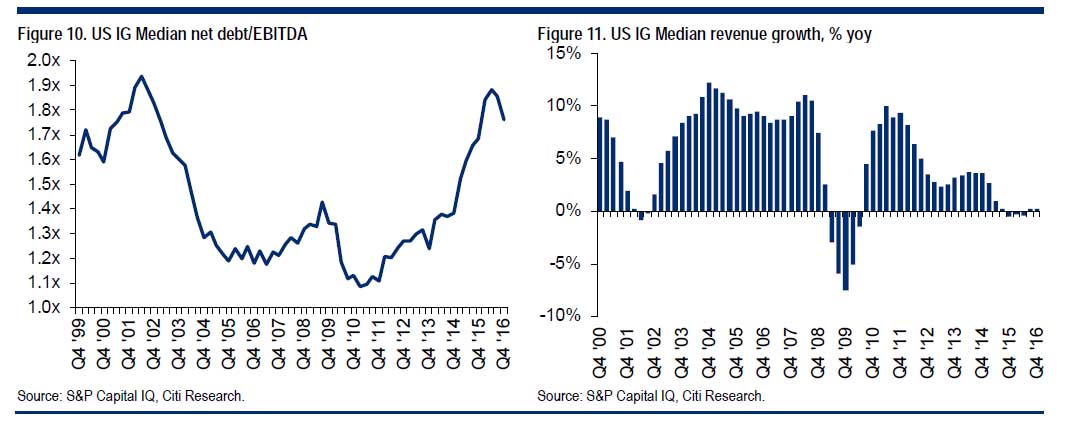

Economic surprises have a natural tendency towards mean reversion and in the US are already starting to come down. A number of commentators are starting to point to the fact that the improvement in economic numbers is heavily skewed towards survey data as opposed to actual production and consumption numbers. US jobless claims at 40-year lows in any case suggests that further hiring may begin to contribute more to inflation than to real GDP. On the corporate side, our first take on the latest US earnings numbers does point to an encouraging improvement in leverage, for both IG and HY, driven by a fall in the pace of net debt accumulation and continued modest EBITDA growth (Figure 10).

But they fail to show any evidence of significant revenue growth – one of the vital missing ingredients that could conceivably lead to an acceleration of capex (Figure 11). Perhaps revenues were crimped by $ strength, but overall this suggests that the EPS growth everyone is getting excited about owes more to further cost cutting and perhaps currency moves (helping explain why the pick-up is greater in Europe than in the US) than it does to anything that will sustainably buoy the economy.

Sadly, there are even signs that the equity market itself recognizes this likelihood. While the S&P has continued to rally at a headline level, our equity strategists have pointed out that it is again being driven by defensive sectors, not cyclicals – something historically more consistent with a rally in Treasury yields and a global reach-for-yield than with a growth-led reflation (Figure 12).

Likewise, our take on the Trump speech to Congress – with its repeated reference to infrastructure spend but general lack of detail – is that prospects for widespread fiscal reform remain so contentious, even among Republicans, that the likelihood that they drive a significant near-term boost to growth is actually dimming. Once again, this suggests that markets may be getting ahead of themselves.

6. The beast that refuses to die – European political risk To judge from the recent rally in OATs, you could be forgiven for thinking that Macron had been elected already, and that euro break-up risk was once again off the table. Without wanting to get too involved in the labyrinthine twists and turns of what is already turning out to be a decidedly antagonistic campaign, we doubt very much that this risk is gone for good. Regardless of the contentious arguments surrounding whether or not recent developments add to or reduce the still relatively unlikely probability of an eventual Le Pen victory, four factors keep us convinced European periphery risk and French domestic-law bonds are still a ‘sell’ here – and that renewed periphery widening may yet upset markets more broadly.

First, we still think there is the potential for significant nervousness among real money investors in the run-up to, and immediately after, the likely first-round Le Pen victory. Notwithstanding demand from domestic institutions for bonds that others wish to sell, experience suggests that there is nevertheless a point where domestics become full. Recent price action seems driven primarily by fast money; we remain nervous that, if there is a move to reduce holdings among the €1tn held by real money, it would be much harder to absorb (Figure 13).

Second, we still meet too many investors convinced that the ECB will somehow come to the rescue, or even that the market would shrug off a Le Pen victory in the same way as it did Brexit. We could not disagree more strongly.

Third, even a Macron or Fillon victory seems unlikely to us to consign European political risk to the dustbin of history in the way some have been arguing. Populists everywhere still feel as though they are in the ascendant – just look at the disarray among Democrats in the US, or the heated response to Sir John Major’s and Tony Blair’s stands on Brexit in the UK. With the UK likely to trigger Article 50 later this month (and £ showing renewed signs of weakness on the back of it), Geert Wilders still likely to poll well in the Netherlands on 15 March (if not to form an actual government) and Italian politics once again mired in uncertainty, we struggle to see a revitalized move towards European integration as a likely outcome here. Perhaps Juncker’s new plan for a multi-speed Europe (ironically, just the sort of Europe that many in the UK were hoping for) may succeed where previous efforts have failed, but at a minimum it faces a great many hurdles to actual implementation.

Fourth and most persuasively, almost regardless of what you think the actual probabilities of euro break-up are, we still see too little by way of premia across markets to compensate investors for the potential risks. Central banks appear to have succeeded in squashing the volatility and fear out of markets without removing the underlying risk factors themselves. The more markets rally, the greater is the potential vulnerability.

7. Valuations Last but by no means least, that brings us to valuations in general. Do you really want to be buying credit at post-crisis tights, or the S&P at a cyclically-adjusted P/E which has been exceeded only in 1998-2000 and 1929? The only metrics on which € credit does not look expensive in our regular Valuations Report are those that are survey-based.

In Asia last week, we were asked repeatedly not only whether credit could go back to 2007 levels, but even why it should not rally straight through them! To the extent that investors want such upside, we think they would be better served targeting assets that rallied less hard in the first place – albeit in small doses. And yet there, too, our outright inclination is more towards reduction and waiting for a better entry point than towards adding at current levels.

Conclusion – Memento mori To sum up, markets seem increasingly to be pricing all of the upside and none of the downside. When there was a risk premium in spreads, and when a wave of central bank and private credit creation seemed likely to carry everything tighter regardless of underlying fundamentals, we were happy to run with that. But we think that risk premium has long gone, and that markets’ strength owes more to those technicals than is widely recognized. When in the days of the Roman Republic generals were awarded the highest honour the Senate could bestow – the right to lead a “triumph”, or parade of the spoils of war, into the city – it is said that a slave was required to stand at their side and whisper constantly into their ear that they too were merely mortal. With the Ides of March approaching – and, rather neatly, coinciding both with an FOMC meeting and with the Dutch elections – we think the timing would be good for investors too to remember to what they owe their improvement in fortunes. We don’t think it’s the arrival of a new emperor.

Advertisement

Very good and all quite right. Neither do we see any structural shift out of secular stagnation, which is one reason why we have recently taken profits. But, if there is a pull back on these anxieties, then we’ll get longer again. The MB portfolio is balanced enough to offset the risks and the upside remains obvious. The US economy has a series of tailwinds:

Trumpian confidence leading into a fiscal hand-off;

slowly tightening labour markets, and

a revitalised shale boom

If the fiscal hand-off does not happen then we’ll be headed for the exit quick smart but until then it is buy the dips in the USD and S&P500.

Advertisement

We’re buying dips in gold to hedge European risk.

We’re selling rallies in the AUD and commodities, and buying short end Aussie bonds on the dip to hedge Chinese risk.

We completely accept that this is the tail end of the business cycle, not the beginning of it, and that at some point in the next year or two that the Fed will crush the Trump boom but until such a time we see an opportunity to make hay.

The key, though, is that we are liquid and ready to move on a dime. That is vital given some of the risks here are asymmetric, such as Europe, which is why we say sell property!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.