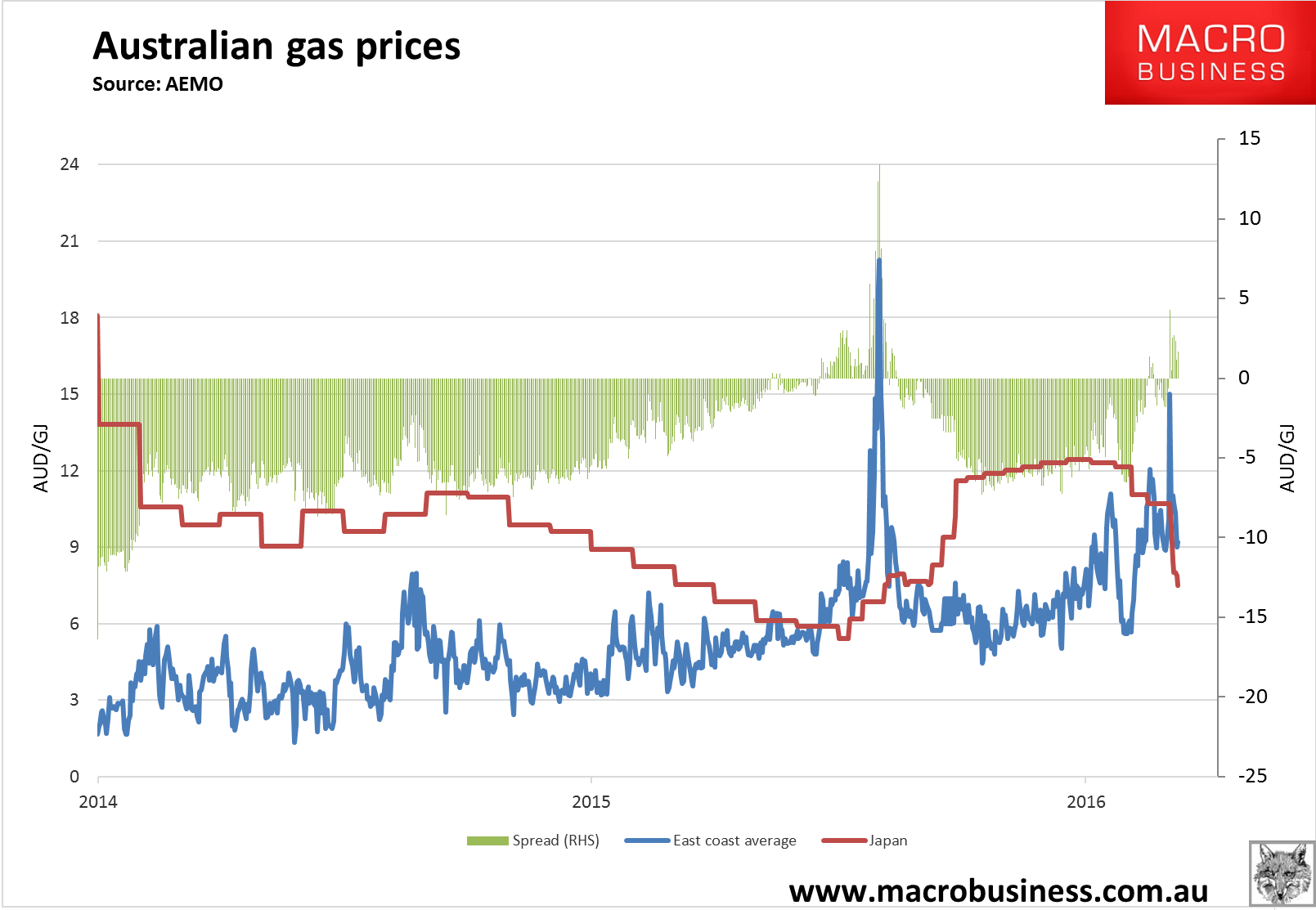

The east coast gas price retains a very healthy premium to exactly the same gas sold in Japan today:

This is despite the fact that in a functional market locals should never pay higher than export net back prices which is the Japanese price minus the cost of transport, liquifaction and shipping, which ought to be around $5Gj today. Instead it is $9.19Gj.

The shortage is turning critical in Victoria as Hazelwood closes:

Victoria’s energy security has been thrown into question, with the state facing an unprecedented 72 days of possible power supply shortfalls over the next two years following the shutdown of the Hazelwood plant next week.

Australia’s electricity grid operator has warned that the looming shutdown of the ageing plant, which supplies up to a quarter of the state’s power, could lead to breaches of the minimum energy reliability benchmark next summer.

Unit Controller John Soles will probably be forced to retire after 18 years working at Australia’s dirtiest coal-fired power plant, which officially closes at the end of March.

Its data shows 72 days of potential power “reserve shortfall”.

While the prediction does not mean Victoria is facing imminent blackouts, it does highlight the risks to the state’s power supply as the Andrews government prepares for next year’s election, with toxic state-federal relations and energy policy uncertainty blamed for inhibiting new investment.

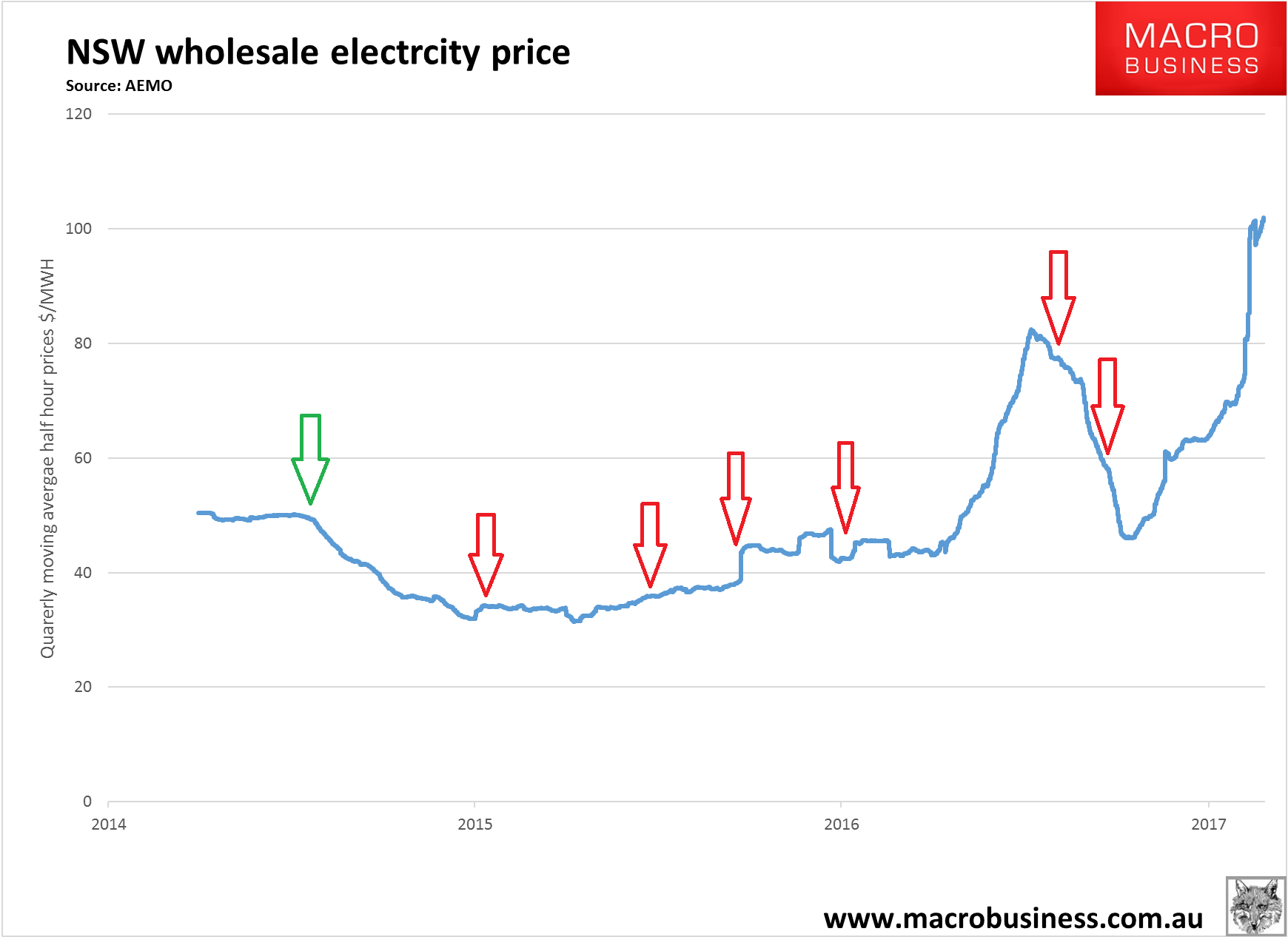

Which is one reason for skyrocketing electricity prices (the green arrow is the carbon price abolition, red is Curtis Island LNG startups):

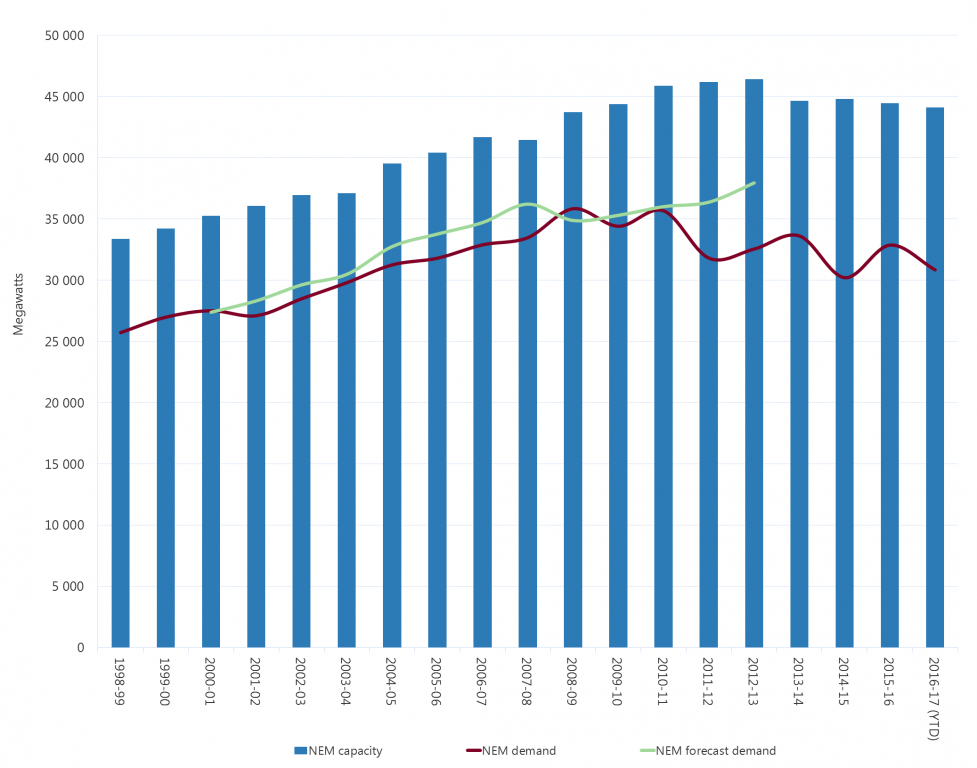

Even though there has never been more spare east coast power capacity:

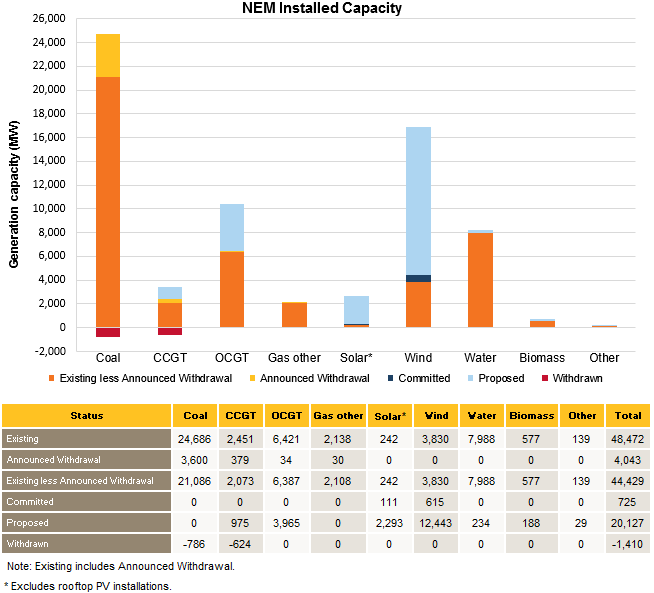

But it is all gas that can no longer afford to run:

Not surprisingly, gas-dependent manufacturers are also spewing and pointing the finger where it belongs, via the AFR:

Resentment is growing among industrial gas buyers struggling with surging prices who complain GLNG made a mistake on how much gas it could supply from its own wells and has been forced to make up the shortfall by buying on the domestic market.

“They miscalculated big time,” said Garbis Simonian, managing director of NSW aluminium scrap processor Weston Aluminium, which is paying about $12 a gigajoule for gas that cost $7 six months ago.

“You made the bad call. If you can’t get the gas, you should suffer, not make us suffer.”

…The GLNG venture originally expected to buy only small volumes of gas for its export project, but rising field costs and under-performing wells mean it will use third-party gas for almost half its production, according to some analysts.

In its environmental impact statement in 2010, GLNG said it “is not diverting gas from local markets to export markets” and argued it “has no direct implications for domestic gas prices”.

GLNG pointed out that the gas for LNG would come from “newly developed” coal seam gas fields and emphasised the volume was “very small” relative to total east coast reserves.

“It is therefore unlikely to contribute to a future shortage of gas in the domestic market,” it declared.

Quite right, as Credit Suisse argues:

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5%

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5% thirdparty gas – 20–25PJa. APLNG is self-sufficient, but as can be seen the other thirdparty gas would get extremely close to balancing the market. Clearly these things are far better done by mutual agreement from all parties, rather than a political mandate.

■ GLNG loses but can all be compensated? We estimate that, at a US$65/bbl oil price, GLNG as an entity would lose US$447m p.a. of FCF if they could no longer toll thirdparty volumes. Interestingly, if Kogas and Petronas could recontract their offtake on a slope of 12x (doable in the current LNG market) then their losses as an equity partner are all offset (not equally between the two albeit). Santos would see ~50% of its US$134mn net GLNG loss offset if the Horizon contract could move up to a slope of 8x from 6x. The clear loser would be Total. We wonder whether cheap government debt, a la NAIF, could be provided at the (new, lower volume) project level or even to take/fund an equity stake in it? In reality all parties (domestic buyers included) have some culpability in the situation, so a sharing of pain does not seem unreasonable 02 March 2017 Australia and NZ Market daily 31.

What will it cost us to not fix it?

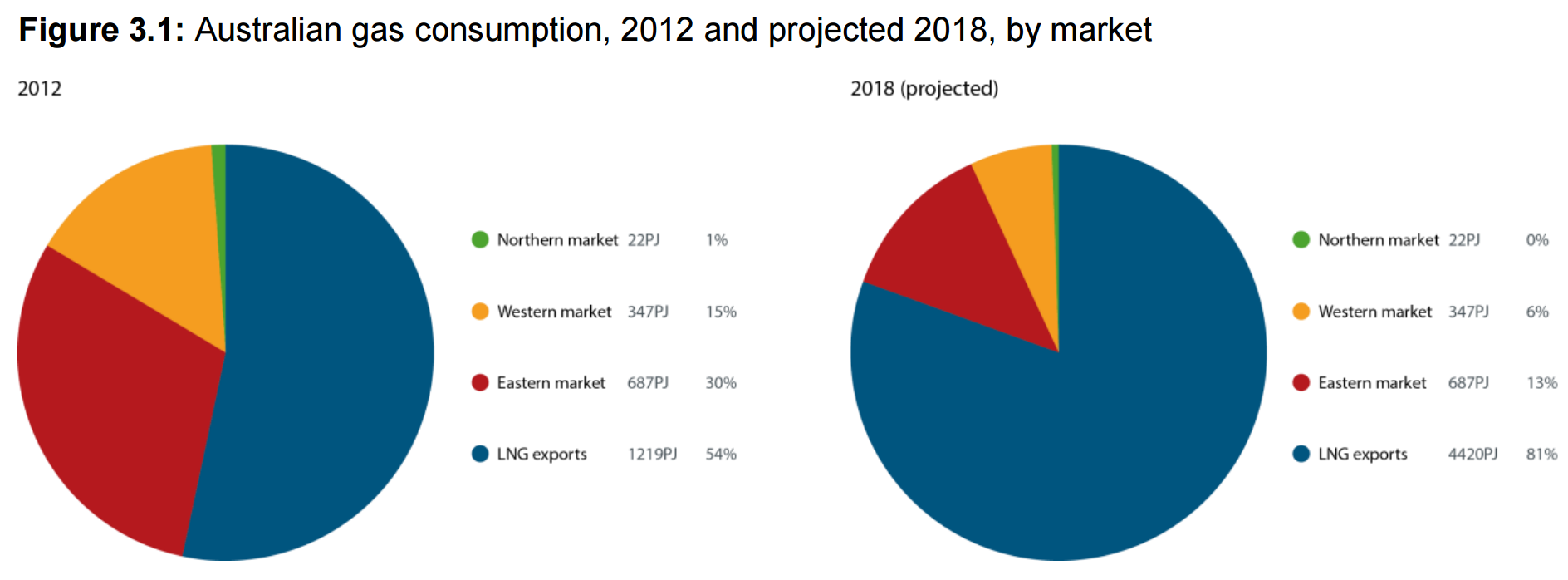

We need to hold back a tiny 160Pj of gas to balance the domestic market. That amounts to a fantastically paltry 2.9% of total national demand or 3.6% of total export volumes in 2018. 80% of Australian gas production would still go to Asia.

At current rates of consumption, east coast gas of 1100PJs will cost $13.2bn at $12GJ. If we held back the 160Pj we could halve that. Electricity prices have also doubled to $100mWh on the gas price and we currently pay out roughly $5bn for our two terrawatts of electricity consumption. So that’s another $2.5bn saving if we can halve it. It is the effective equivalent of a $9bn tax (before we consider the knock-on effects of further capital mis-allocation) levied on east coast households and industry by the foreign shareholders and governments that own Curtis Island LNG. Pure economic rents siphoned off just because they can be.

But that’s not the end of it. These same firms and governments lose money on every tonne that they ship offshore. They buggered up their investment metrics so horribly that when you include the cost of capital for building the plants, they are losing money hand over fist. This even includes the west coast LNG plants. As a result they can claim huge depreciation and write-offs on massively inflated investments and they pay no tax.

Australian LNG blew an enormous bubble that has now burst. It did it all by itself. The fallout is being redirected onto the east coast economy via a cartel gouge which is shuttering manufacturers and artificially turning huge electricity market spare capacity to shortage, jeopardising the energy security of the entire east coast of the country.

The only rightful place for the pain is the LNG projects themselves. Anything else is manifestly insane.