From the AFR:

Shell has responded to the intensifying squeeze on east coast gas with a commitment to provide 10 per cent more gas for the domestic market thanks to a $500 million investment to drill more wells in south-west Queensland.

“Project Ruby”, by Shell’s QGC business, represents the next chunk of investment that was required after a $1.7 billion tranche of spending in 2015 to maintain gas supply for its $25 billion export project in Gladstone.

…Shell Australia chairman Andrew Smith said the investment was “a further vote of confidence in Queensland’s onshore gas industry”, comparing the state favourably against NSW and Victoria where drilling has stalled and jobs lost.

QGC committed at last week’s meeting to sell more gas into the domestic market than it buys, and on Tuesday Shell said it would sell more than 75 petajoules – net of gas it buys from the market – to customers in Australia this year.

Queensland Premier Annastacia Palaszczuk said…”As we know, this and other projects around the state are needed to grow the economy,” said Ms Palaszczuk, who just returned from India where she looked at new LNG import plants.

…Mr Smith criticised the other states for their policy on gas exploration and development, particularly Victoria’s “particularly stupid” ban on all onshore development.

A 10% improvement on 75Pj is nothing. Moreover, why is Shell bashing Victoria when it has no onshore gas reserves? Shell needs to develop Arrow in QLD, 17% of east coast reserves, not fart a little extra gas into the system. Politician turned parasite, Ian Macfarlane of course agrees:

Queensland Resources Council CEO Ian MacFarlane also welcomed the deal, saying supply issues for gas federally would be partially offset by the new wells.

“The QRC is pleased that Queensland is leading the way when it comes to working to address the problem of the east coast gas shortage,” Mr MacFarlane said.

The new wells will be drilled in 2017 and 2018 in QGC’s existing land, with deals currently being negotiated with neighbouring landholders for access and compensation.

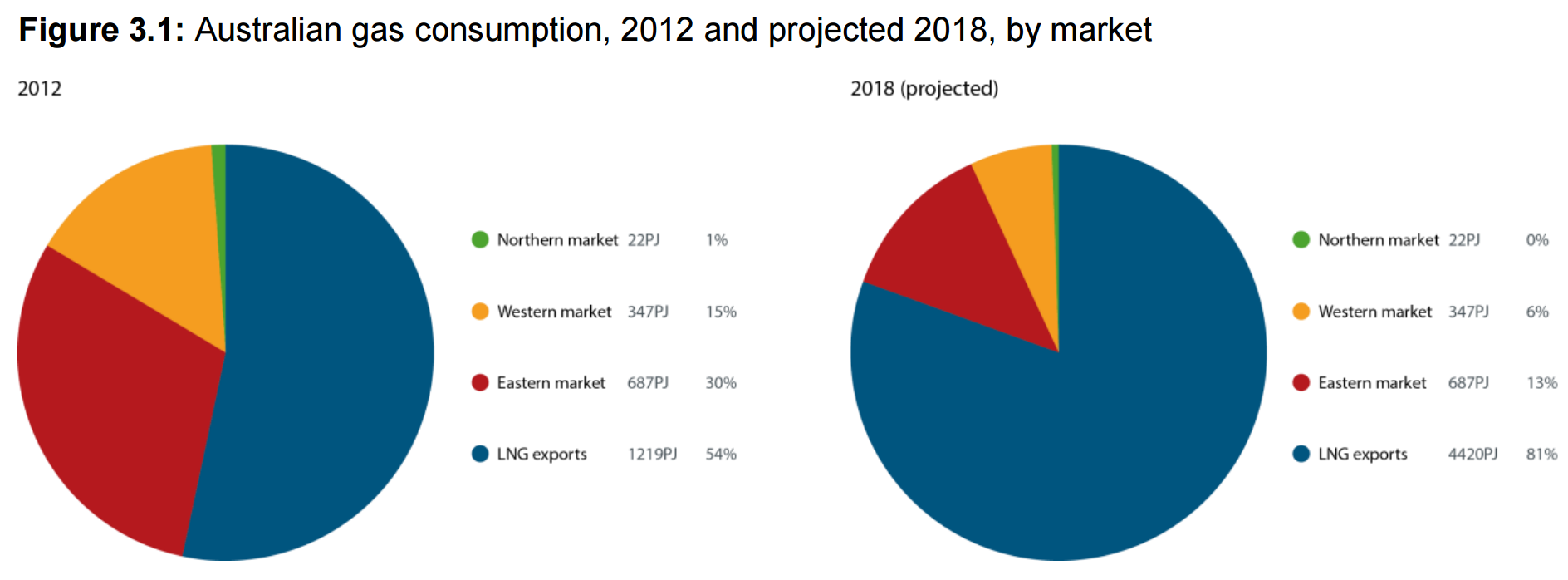

The shortage is 160-200Pj not 7Pj. What will it cost us to not fix it?

We need to hold back a tiny 160Pj of gas to balance the domestic market. That amounts to a fantastically paltry 2.9% of total national demand or 3.6% of total export volumes in 2018. 80% of Australian gas production would still go to Asia.

At current rates of consumption, east coast gas of 1100PJs will cost $13.2bn at $12GJ. If we held back the 160Pj we could halve that. Electricity prices have also doubled to $100mWh on the gas price and we currently pay out roughly $5bn for our two terrawatts of electricity consumption. So that’s another $2.5bn saving if we can halve it. It is the effective equivalent of a $9bn tax (before we consider the knock-on effects of further capital mis-allocation) levied on east coast households and industry by the foreign shareholders and governments that own Curtis Island LNG. Pure economic rents siphoned off just because they can be.

But that’s not the end of it. These same firms and governments lose money on every tonne that they ship offshore. They buggered up their investment metrics so horribly that when you include the cost of capital for building the plants, they are losing money hand over fist. This even includes the west coast LNG plants. As a result they can claim huge depreciation and write-offs on massively inflated investments and they pay no tax.

Australian LNG blew an enormous bubble that has now burst. It did it all by itself. The fallout is being redirected onto the east coast economy via a cartel gouge when the only rightful place for it is the projects themselves.

Time to hand it back. The answer is obvious, from Credit Suisse:

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5%

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5% thirdparty gas – 20–25PJa. APLNG is self-sufficient, but as can be seen the other thirdparty gas would get extremely close to balancing the market. Clearly these things are far better done by mutual agreement from all parties, rather than a political mandate.

■ GLNG loses but can all be compensated? We estimate that, at a US$65/bbl oil price, GLNG as an entity would lose US$447m p.a. of FCF if they could no longer toll thirdparty volumes. Interestingly, if Kogas and Petronas could recontract their offtake on a slope of 12x (doable in the current LNG market) then their losses as an equity partner are all offset (not equally between the two albeit). Santos would see ~50% of its US$134mn net GLNG loss offset if the Horizon contract could move up to a slope of 8x from 6x. The clear loser would be Total. We wonder whether cheap government debt, a la NAIF, could be provided at the (new, lower volume) project level or even to take/fund an equity stake in it? In reality all parties (domestic buyers included) have some culpability in the situation, so a sharing of pain does not seem unreasonable 02 March 2017 Australia and NZ Market daily 31