At the AFR, manufacturers are howling:

Shell-shocked businesses are reassessing investments and jobs after being slugged by huge increases in their electricity bills driven by the imminent closure of the giant Hazelwood power station combined with hot weather and rising “green” power costs.

As commercial customers go to renew their power supply contracts, they are seeing a direct hit from the spike seen in forward prices for electricity in recent months. The Hazelwood closure, set for the end of March, has also heightened worries about the risk of blackouts on a grid with reduced access to baseload power.

Hardware manufacturer Alchin Long Group in Sydney’s west has had to agree to a near-doubling of its electricity price and may rethink plans to shift work back to Australia from China as a result, said Graham Lee, national operations manager. The price of the new two-year contract from Origin Energy has surged from $55.30 per megawatt-hour to $109.70 .

“We have yet to see an invoice, they will be coming in the next few months, but I’m bracing myself for a huge increase,” said Mr Lee. Prices offered by rival suppliers ranged up to $129.96/MWh.

“We are in the process of reviewing bringing back work to Australia out of China due to the cost increases there, [but] with a large rise in our primary input costs maybe we need to reconsider.”

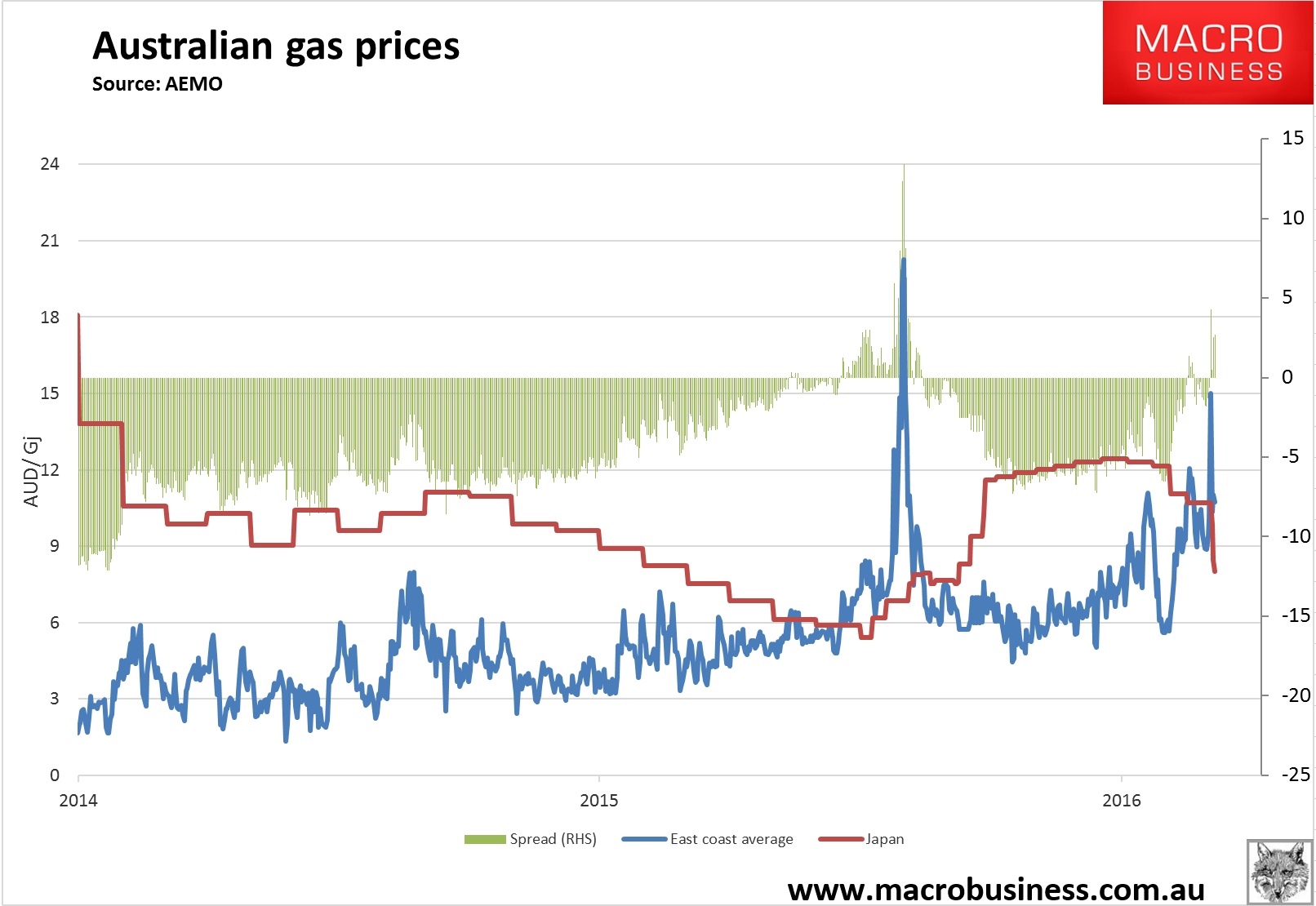

The price rises are coming from the east coast gas price which sets the marginal cost of electricity in national electricity market (NEM). The economic answer is very simple. Address the gas price. The east coast average price is above $10.70Gj while the exactly the same gas is available in Japan for $8Gj:

Thus the locals are paying $2.70Gj more than the Japanese are in spot markets. In 2014 locals were paying -$12Gj less than the Japanese.

If the market were operating efficiently (that is, at all), the local gas price would be set at the export net-back price, which would be the Japanese price minus the cost of liquifaction and shipping. That would be roughly around $6Gj. The mispricing is possible because a gas cartel has formed and is gouging the local market even as it ships loss-making gas to Japan. Cartel members include Origin, Santos, Shell, BHP and Exxon:

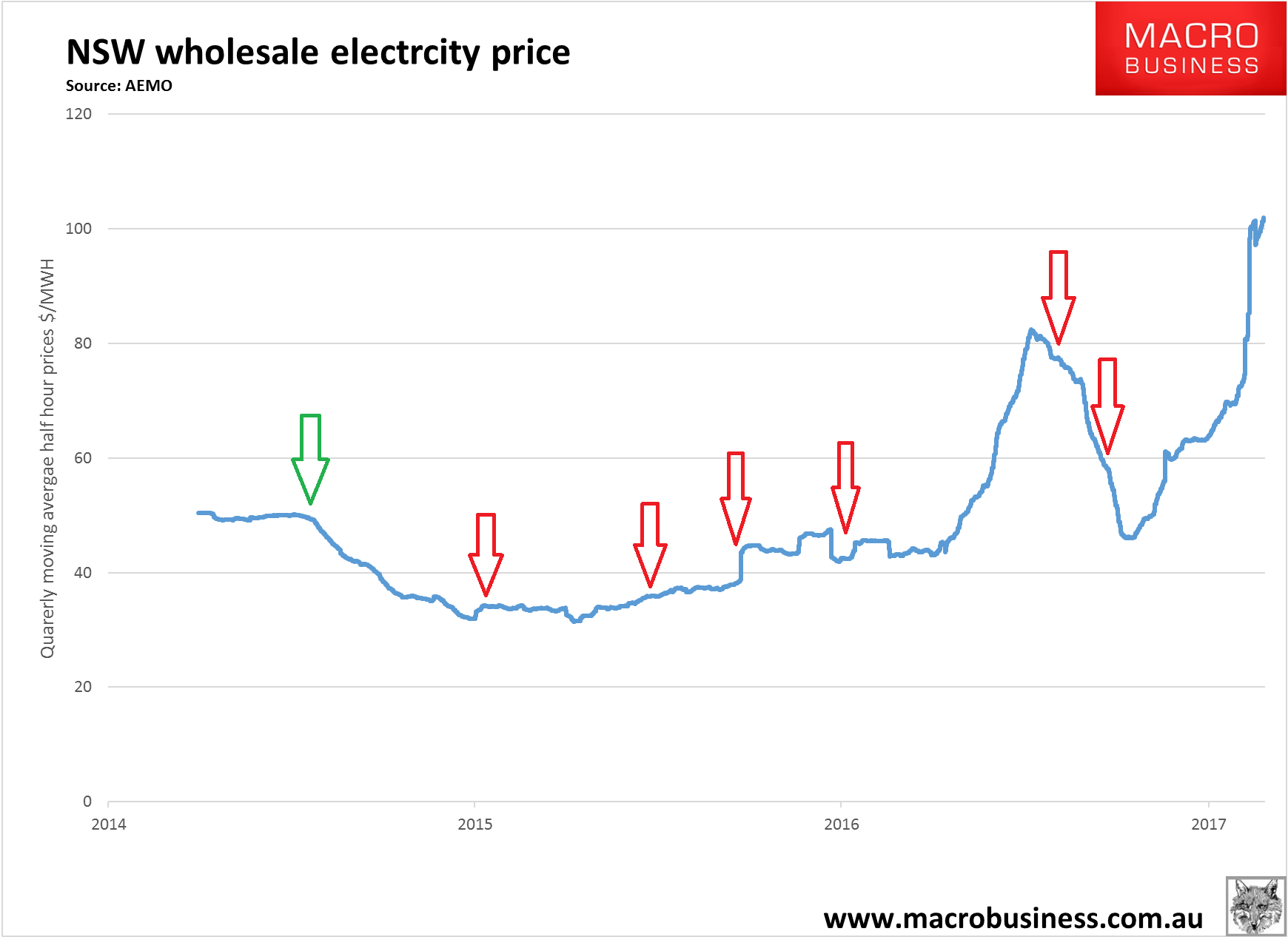

The result is this for power costs:

The green arrow is the carbon price cut. The red arrows are the gas cartel LNG plant startups.

But no, says the Do-nothing Government, via The Guardian:

The resources minister, Matt Canavan, says adopting a national policy where a proportion of natural gas would be reserved for domestic use would not deliver “a very good outcome” because rationing doesn’t work in other markets.

Canavan, a Queensland National, used a steak analogy on Monday to make his point. He said Australian beef producers currently exported a significant quantity of steak, and that practice didn’t create a domestic shortage of prime cuts in butchers and supermarkets.

“We don’t make sure we have enough scotch fillet in the supermarket by telling farmers they can’t sell their beef or cattle to overseas markets,” the resources minister told Sky News on Monday.

“We let them sell to a wide range of markets which gives them confidence to invest which gives them a good return when they can get a good price – and we have plenty of steak.”

A shortage of gas in eastern Australia, and surging prices, has reignited public debate about whether a portion of gas supply should be quarantined for domestic use. Currently in Western Australia, 15% of the gas produced by each liquefied natural gas project must be kept for domestic purposes.

Canavan’s comments on Sky News follow a call last week from the Victorian Nationals MP Andrew Broad, for serious consideration about whether 15% of gas supply should be reserved for Australian manufacturing rather than exported.

What can I say? He might as well be talking about alien anal probes for all the economic sense that he’s making. Canavan wants to build a coal power plant in QLD that will do nothing to drop power prices given its output will be even more expensive than the gas.

This has nothing to do with steak and everything to do with pork, to see off One Nation in the LNG and coal seats of Dawson, Flynn and Capricornia in northern Queensland, as well as keep alive the energy crisis right down the east coast to attack Labor with by blaming renewables.

This now holds an uncanny parallel with the Enron debacle in the US at the turn of century. For those with memory longer than yesterday, which cancels out most of Australia’s political economy, it is useful to recall that the US west coast experienced a torrid time at the turn of the millennium as a friendly company called Enron ran riot in power markets, via Wikipaedia:

The California electricity crisis, also known as the Western U.S. Energy Crisis of 2000 and 2001, was a situation in which the United States state of California had a shortage of electricity supply caused by market manipulations, illegal shutdowns of pipelines by the Texas energy consortium Enron, and capped retail electricity prices. The state suffered from multiple large-scale blackouts, one of the state’s largest energy companies collapsed, and the economic fall-out greatly harmed Governor Gray Davis‘ standing.

Drought, delays in approval of new power plants, and market manipulation decreased supply. This caused an 800% increase in wholesale prices from April 2000 to December 2000. In addition, rolling blackouts adversely affected many businesses dependent upon a reliable supply of electricity, and inconvenienced a large number of retail consumers.

California had an installed generating capacity of 45GW. At the time of the blackouts, demand was 28GW. A demand supply gap was created by energy companies, mainly Enron, to create an artificial shortage. Energy traders took power plants offline for maintenance in days of peak demand to increase the price. Traders were thus able to sell power at premium prices, sometimes up to a factor of 20 times its normal value. Because the state government had a cap on retail electricity charges, this market manipulation squeezed the industry’s revenue margins, causing the bankruptcy of Pacific Gas and Electric Company (PG&E) and near bankruptcy of Southern California Edison in early 2001.

G.W. Bush backed Enron to the hilt in its assault on Democratic held California and it helped get Arnold Schwarzenegger elected. Do-nothing Malcolm is now doing exactly the same thing down the entire east coast of Australia for political gain.

The answer is simple. The gas cartel built too may LNG plants and are now making everyone else pay for it. They must carry the cost, as Credit Suisse said last week:

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5% thirdparty gas – 20–25PJa. APLNG is self-sufficient, but as can be seen the other thirdparty gas would get extremely close to balancing the market. Clearly these things are far better done by mutual agreement from all parties, rather than a political mandate.

■ GLNG loses but can all be compensated? We estimate that, at a US$65/bbl oil price, GLNG as an entity would lose US$447m p.a. of FCF if they could no longer toll thirdparty volumes. Interestingly, if Kogas and Petronas could recontract their offtake on a slope of 12x (doable in the current LNG market) then their losses as an equity partner are all offset (not equally between the two albeit). Santos would see ~50% of its US$134mn net GLNG loss offset if the Horizon contract could move up to a slope of 8x from 6x. The clear loser would be Total. We wonder whether cheap government debt, a la NAIF, could be provided at the (new, lower volume) project level or even to take/fund an equity stake in it? In reality all parties (domestic buyers included) have some culpability in the situation, so a sharing of pain does not seem unreasonable 02 March 2017 Australia and NZ Market daily 31

■ If these contracts were then all diverted domestically, at US$65/bbl oil, they should deliver gas at Wallumbilla at $7.50 gj. This is highly competitive gas in the current environment we think and should certainly not be considered unreasonable by domestic buyers

■ Importing LNG: AGL has now very publically disclosed its plans to look at using floating regas to import LNG into Australia. Whilst many believe this is just a negotiating tactic with buyers, we are less convinced. That said, with AGL rightly unlikely to want to take price risk, this might be more about targeting seasonal markets than providing 10-year supply agreements with industrial buyers. Even if one contracted off Henry Hub and used a long-run price of US$3/mmbtu, it would be landing in Australia at >A$10/GJ. Post transportation costs this could again be unmanageable for many domestic buyers of flat, term contracts. Importing LNG could be key in targeting seasonal (winter) spikes though

■ Reducing red tape, lifting moratoriums and stricter use it or lose it policies: Policy has an enormous role to play, partially short term, but in particular long term. Projects need to be made cheaper and quicker to bring to market and companies need to be forced not to sit on assets

■ The ultimate aim, from a national perspective, has to be to get the domestic market in surplus again. As witnessed in the US, the multiplier effect of having cheaper, relatively stable and plentiful gas supply has a material multiplier effect on the economy. Clearly producers would rather a tight, even undersupplied market, but with the right frame work in place (which it clearly isn’t at the moment) a more equitable and profitable industry could exist for all parties. Even with a sledge hammer, breaking the camel’s back appears the hardest thing at this stage

More here.

If this were done then the east gas gouge would stop, electricity prices would fall and Australian decarbonisation via renewables would resume quite comfortably as the gas peaking plants currently idled would resume output.

I am pretty cynical these days but I have to tell you that this implicit alliance between the gas cartel and the Do-nothing Malcolm government really takes the cake.