The excellent Credit Suisse today offers some deep thinking on the subject of domestic gas reservation:

For many years now we have been talking about the challenges faced by the East Coast gas market. It is certainly fair to say that we have not seen universal agreement from others on our view.

Despite our doubters, we remain more convinced than ever about the perilous nature of the situation. With each day that goes by with no resolution the challenge only grows greater too (with it greater potential ramifications for the stocks that we cover).

For this note we have leaned on one of Aesop’s fables to analyse the situation. In his wellknown fable The Ass, the Cock and the Lion, a lion is scared off hunting the ass by the crowing of a cock (a sound that, it is said, a Lion has a singular aversion to). Misled by the fear it saw in the Lion from the mere crowing of a cock, the Ass decided to in fact attack the Lion. Unfortunately, once out of hearing range of the cock’s crowing, the Lion found its courage once again and tore the ass to shreds. As with all of Aesop’s fables, moral interpretations are partially in the eye of the reader. However, the generally accepted interpretation for this one is that presumption begins in ignorance and ends in ruin.

Huge levels of presumption have beset the east coast gas market along the way, from corporates, politics, gas buyers and market analysts alike. We still believe that no one (no matter how pretty your spreadsheet – and we can, and do, build them too) can definitively say what supply will be. A confluence of well performance variability (particularly in CSG), availability of capital and political red tape on new molecules make it impossible. What we do believe is that the east coast gas market is perhaps hearing the last few decibels of crowing, before a deeply uncomfortable realisation on how hard it is to fix it all (and the implications from it not being fixed).

We are still not quite naïve enough to think that what we write is as easy to implement as it is to dream up. Curtis Island is the perfect case study of common sense failing to prevail. However, what we do know is that the time is fast approaching where no resolution will lead to very real, and likely irreversible, consequences for domestic buyers and producers. In this note, we update our

In this note, we update our supply side assumptions, with the net effect being some moderate improvement in supply (30–50PJa, albeit it is extremely unclear how sustainable the 33PJa incremental from APLNG is as well performance deteriorates). We then look to the possible resolutions and try and pick through the rubble for equity market implications:

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5%

■ Our preferred option is to reclaim the third-party gas currently being exported: Aside from the Horizon contract between GLNG and Santos, there was no evidence in the EIS or FID presentations that more non-indigenous gas was required. As such, one could argue reclaiming what has only been signed due to a scope failure, is equitable. Including the Horizon contract GLNG will be exporting >160PJa of third-party gas in the later part of this decade. Whilst we get less disclosure these days, BG previously said that after an initial 10–20% in the early days (now gone) QCLNG would use ~5% thirdparty gas – 20–25PJa. APLNG is self-sufficient, but as can be seen the other thirdparty gas would get extremely close to balancing the market. Clearly these things are far better done by mutual agreement from all parties, rather than a political mandate.

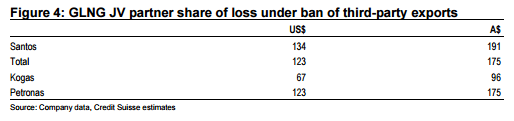

■ GLNG loses but can all be compensated? We estimate that, at a US$65/bbl oil price, GLNG as an entity would lose US$447m p.a. of FCF if they could no longer toll thirdparty volumes. Interestingly, if Kogas and Petronas could recontract their offtake on a slope of 12x (doable in the current LNG market) then their losses as an equity partner are all offset (not equally between the two albeit). Santos would see ~50% of its US$134mn net GLNG loss offset if the Horizon contract could move up to a slope of 8x from 6x. The clear loser would be Total. We wonder whether cheap government debt, a la NAIF, could be provided at the (new, lower volume) project level or even to take/fund an equity stake in it? In reality all parties (domestic buyers included) have some culpability in the situation, so a sharing of pain does not seem unreasonable 02 March 2017 Australia and NZ Market daily 31

■ If these contracts were then all diverted domestically, at US$65/bbl oil, they should deliver gas at Wallumbilla at $7.50 gj. This is highly competitive gas in the current environment we think and should certainly not be considered unreasonable by domestic buyers

■ Importing LNG: AGL has now very publically disclosed its plans to look at using floating regas to import LNG into Australia. Whilst many believe this is just a negotiating tactic with buyers, we are less convinced. That said, with AGL rightly unlikely to want to take price risk, this might be more about targeting seasonal markets than providing 10-year supply agreements with industrial buyers. Even if one contracted off Henry Hub and used a long-run price of US$3/mmbtu, it would be landing in Australia at >A$10/GJ. Post transportation costs this could again be unmanageable for many domestic buyers of flat, term contracts. Importing LNG could be key in targeting seasonal (winter) spikes though

■ Reducing red tape, lifting moratoriums and stricter use it or lose it policies: Policy has an enormous role to play, partially short term, but in particular long term. Projects need to be made cheaper and quicker to bring to market and companies need to be forced not to sit on assets

■ The ultimate aim, from a national perspective, has to be to get the domestic market in surplus again. As witnessed in the US, the multiplier effect of having cheaper, relatively stable and plentiful gas supply has a material multiplier effect on the economy. Clearly producers would rather a tight, even undersupplied market, but with the right frame work in place (which it clearly isn’t at the moment) a more equitable and profitable industry could exist for all parties. Even with a sledge hammer, breaking the camel’s back appears the hardest thing at this stage

Updating Supply/Demand movements

We wanted to just acknowledge the movements that have occurred in supply and demand dynamics since we last published.

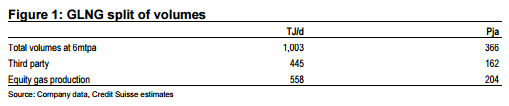

The most obvious changes have been at GLNG, where the demand call has been reduced by Santos lowering its steady state production guidance to 6mtpa, optically a ~73PJa reduction in demand versus 7.2mtpa.

If one takes the midpoint of third-party gas volumes (which have all been disclosed by Santos), you can back out an implied level of equity gas production of 204PJa as per Figure 1.

This is obviously a net GLNG number. Whilst we don’t know the expected split of this equity production between Fairview and the other fields, we assume that Fairview stays broadly flat at current levels of ~450TJ/d (running a bit above that recently), leaving ~110PJa from Roma and the other fields.

Grossed up at Fairview, this would see the GLNG fields producing ~247PJa. Interestingly this is exactly 73PJa below the 320PJa we were previously assuming the GLNG fields produced. As such the net impact on the market is zero. Interestingly it is also 20PJa below the bear case we ran in our previous notes on the East Coast Gas market – perhaps a warning about other assets’ ability to disappoint.

There have been a couple of potentially positive moves on the supply side, with APLNG’s FY18 production guidance 33PJa above the 650PJa we had earmarked for them. To what extent this is sustainable, or even achievable, is unclear, but it does have the potential to add a bit more volume to the market.

Meanwhile, Cooper Energy has guided that it is planning to FID the up to 25PJa Sole project offshore Victoria. So there is the scope for a net 50PJa improvement in supply, in the short term at least.

It is entirely true to say, as we have discussed before, that the GBJV could supply more gas shorter term and even the Cooper Basin if the economics were improved. However, there is little sign either are likely to deliver materially more gas.

So whilst perhaps the extremes of our range for the supply shortage (to meet current demand) have come in a touch, to perhaps 80–250PJa, we are running extremely low on viable assets that could further impact that balance materially in the 2018/19 window.

Hence we come back to the same argument that whilst supply undoubtedly needs to come, and be both incentivised and made easier to come, the issue is going to have to be largely tackled from the demand side.

What are some possible solutions?

With APA CEO Mick McCormack commenting this week in the AFR that “every petshop parrot has a view on the problem and the answer” in relation to the East Coast gas market, we may well be walking into our next round of lambasting.

However, we continue to believe that this is an important issue for the equity market to understand and that views taken by those who have no vested interest in any given outcome can at least bring a modicum of rationality to the debate.

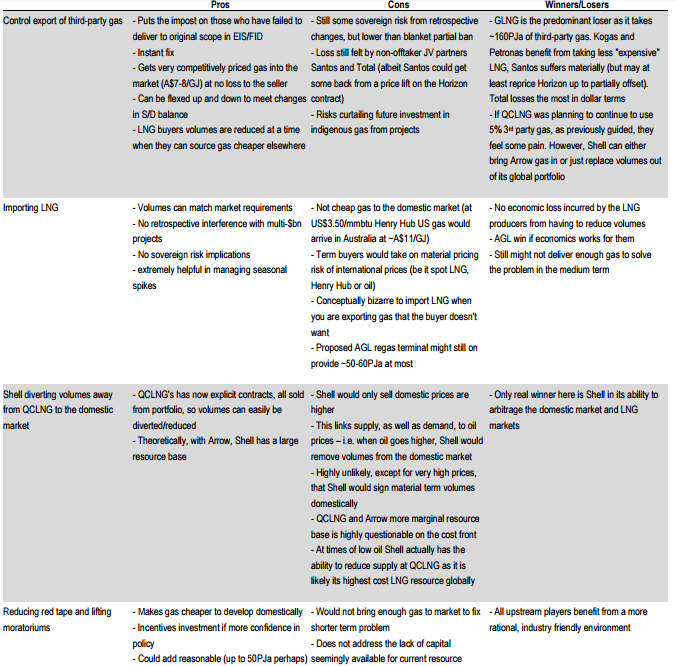

We have laid out in Figure 2 the obvious solutions we see for managing the next few years of the domestic gas market (the challenges faced in the middle of next decade is a whole larger debate). In reality a combination of many of these solutions may be required.

In terms of the options that can materially address volumes into that 2018/19 window it is only importing LNG that would materially impact the supply side of the equation, not demand. Reducing red tape, lifting the moratoriums and implementing use it or lose it policies would help at the margin but, given the lead time of getting gas to the market, would see the greater benefits felt early next decade (where the supply shortage only widens, if demand is steady).

We’ll discuss it in more detail through the note, but optically the most palatable solution could be to put a temporary restriction on the exporting of third-party gas through the LNG projects. Aside from the Horizon contract into GLNG, which was disclosed at the time of FID, we struggle to find any reference in either the EIS or FID documents of any of the projects where it was discussed that further third-party gas would be needed.

Therefore, in effect, what you are doing is only punishing those who failed to deliver to their submissions and targets set to their investors. This is not banning gas that had always been earmarked for export, it is preventing gas that theoretically was never intended to go overseas from going overseas.

GLNG is the vast bulk of the third-party gas buying, at ~160PJa in 2018, with QCLNG potentially another ~20PJa from QCLNG – combined close to balancing the market.

Controlling/banning third-party gas exports seems the most palatable

We do think that the wrong word often gets bandied about when people call for a reservation policy on the east coast. Whilst that is something that might also need to be addressed in future, when you are retrospectively stopping gas from being exported, which has been contractually agreed to be exported, it is in reality an export ban.

The scenario of a blanket partial export ban (say 15% of all volumes out of Queensland) carries huge sovereign risk, is clumsy in that it would punish APLNG which is entirely selfsufficient at this stage and enforces a large economic loss (potentially close to A$1bn p.a.) which either needs to be borne by the corporates or subsidised by the government. Certainly whilst other potential resolutions exist, this seems unpalatable.

However, in the scenario of preventing the export of non-indigenous gas to the LNG projects, whilst the domestic shortage exists, in effect the export projects are only being punished for failing to deliver to their EIS’s and FID releases to the market. The one contentious bit of volume here is Santos’ Horizon contract into GLNG, which was announced with FID, but ironically that is the one that Santos itself would likely be most keen to see diverted domestically (as it could get a higher price).

The maths of diverting third-party gas back to the market at GLNG

We will focus this work on GLNG, in the most part because it is the predominant buyer of third-party gas for export on the east coast, but also because it is most relevant for our listed coverage and also because we no longer get any disclosure on QCLNG third-party gas use expectations.

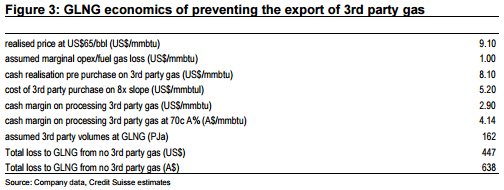

In Figure 3 we have run the economics at the gross level for GLNG. To be clear on our assumptions, we have assumed that the marginal cash cost of processing third-party gas (opex and fuel gas) is ~US$1/mmbtu. As can be seen, if no third-party gas was allowed to be exported then the gross loss to GLNG at US$65/bbl oil would be ~US$450mn.

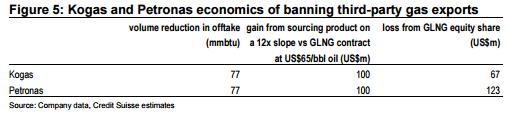

However, the true economic cost to the JV partners is not equal. Kogas and Petronas, which own 15% and 27.5% of that loss, respectively, get the benefit back on the other side as LNG buyers who are no longer buying what is relatively expensive gas.

For simple maths here we just assume that they both just go out and recontract the volumes on a 12x slope, versus currently a ~14x slope. In reality they may well be overcontracted and so not want the volumes at all (making their NPV improvement relatively higher). However, even on these numbers they are collectively about square (with Kogas better off due to its lower equity stake).

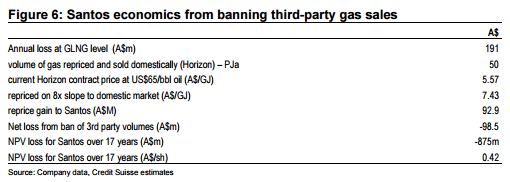

Santos too has some remediating economics, if the Horizon contract is treated the same as other third-party gas (in our view it should be). If this contract were allowed to move up to a more traditional price for these third-party volumes of a ~8x slope, then you can see in Figure 6 that they would claw back ~$93mn p.a. of cash flow from this. That does still leave them with a ~A$99mn p.a. loss versus the status quo, which over 17 years equates to an NPV of ~A$0.42/sh. However, whilst this is by no means the fault of current management, some culpability is needed by the upstream producers. Indeed, as part of this all, the government could likely introduce other policies/steps which could further mitigate this impact for Santos.

The greatest challenge in this all is dealing with Total, a large investor in Australia not just on the East Coast. It is sitting there with no offsets to its US$123mn p.a. loss on our numbers under this scenario. We are not politicians, nor have all of the details in front of us, but do assume there are options open to provide compensation for Total through other avenues to help implement something like this.

The key is that any reduction in export volumes could simply be imposed as, when and if the gas is needed domestically. If domestic demand falls, or supply rises, then the gas can readily be made available for export again.

The challenge remains in getting the gas to the buyers. Interestingly, in the state versus federal debate on policy, much of the gas is needed in NSW and Victoria, states that have made development so hard, and would be supplied from the accommodative states of South Australia and Queensland. Perhaps some kind of centralised buyer (even state run) of these third-party volumes could become the intermediary between the third-party gas suppliers and the end customers.

We know – this is easy to say, very hard to do

Again, our political knowledge is somewhere less than zero. How these kind of policies mechanically get implemented between state and federal politics is above our pay grade and knowledge. However, what we do feel, having sat down (on our perches as those pet shop parrots) and thought harder about a resolution, is that this appears the most obvious of near-term solutions to put a band aid on the market, certainly with the smallest political and financial loss in totality.

Sure it is a change of terms retrospectively, but it is relatively easy to argue that this has only come about because of the inability of the project(s) to deliver to their promises. No gas which is indigenous to the projects would need to be reserved necessarily.

One potential option to appease Total (again easy to say, harder to get competing egos to agree on) is to do the very obvious and run the lower contracted volumes (post this) on Curtis Island across 5 Trains. The sounds of collaboration appear quieter now than they were at <$30/bbl oil unfortunately.

Government funding could help provide a solution

The concept for concessional government funding to help provide a resolution for something such as this dilemma is not entirely alien to Australia. The Northern Australia Infrastructure Facility, passed last year, aims to provide $5bn of concessional financing to build infrastructure in Northern Australia.

As can be seen on the map in Figure 7, Gladstone only misses out on being part of Northern Australia, by NAIF’s definition, by less than 50kms. Darn that Tropic of Capricorn…

In reality NAIF is supposed to be concessional financing for the construction of new infrastructure, not to help with existing, challenged infrastructure. However, the broader framework is there and reasonable and passable road map seems to exist.

Interestingly NAIF is able to take equity stakes, or provide concessional debt, to projects. A similar structure for GLNG could see a NAIF equivalent, maybe aptly named GIT (Gladstone Infrastructure Trust), either take an equity stake off those more disadvantaged by reducing volumes (Total in particular, but perhaps Santos too) at a competitive price, or provide some concessional project finance. To be fair Total already benefits from access to extremely cheap debt, so this might be a less palatable option for them. Various gyrations of debt or equity involvement could be considered though.

There is of course the CEFC (Clean Energy Finance Corp) as another potential route for consideration as a funder.

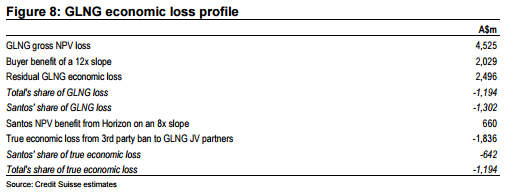

The gross hit to the project itself from removing third-party volumes, on our estimates, is around A$4.5bn of NPV. As in Figure 8, you can see our (by no means perfect) estimate of the share of this loss.

We won’t even begin to explore the machinations of how this could all be structured in this note, we have no doubt at all that it is complicated beyond our wildest dreams. We would just note that there is a clear economic loss for some parties (offsetting a far greater economic loss to Australia more broadly if supply isn’t returned to the domestic market) and a seeming mechanism for some form of government support to soften the blow.

State versus State of course makes this hard

One of the greatest challenges in any form of direct intervention in the market, without corporate agreement, is the battle of the states. The reality is that the states in greatest need of gas are Victoria and NSW, with the donors being South Australia and Queensland.

It is safe to say with all the moratoriums and political shenanigans in Victoria and NSW that they haven’t exactly made the development of gas easy on producers. To an extent asking an accommodative state to bail out one that has been so anti the gas industry is a hard ask. Again, well above our pay grade, but reaching agreement at the federal, and maybe more importantly corporate, level is the key one suspects.

Other options appear more radical or insufficient

The call for a blanket reservation policy, which if it is to deliver more gas is in fact an export ban, carries with it huge sovereign risk consequences. It also most likely financially punishes the project, in the shape of APLNG, that at this stage at least is able to be 100% self-sufficient.

Importing LNG is a very real scenario in our minds, but certainly in AGL’s initial plans is unlikely to be sufficient volumes alone at 50–60PJa. Whilst it might also make fantastic economic sense for AGL in particular from a seasonal perspective, targeting the higher volume (and likely prices in a tight market) in winter, there is very risk that imported LNG is still very expensive gas for term buyers of volume. Even Henry Hub of US$3/mmbtu would see US gas land in Australia at little shy of A$11/GJ. This could price many industrial users out of the market, particularly when overlaying transportation costs and a return on their investment for AGL.

Where importing LNG has a particularly important part to play may be in the seasonal spikes seen during the winter months. In reality, even if the third-party gas from LNG was diverted domestically, a large amount of the domestic gas market is very seasonal (so wouldn’t sign up to a flat, term contract). Imported volumes can accommodate that winter spike (and of course for their economics target the higher prices).

Removing the red tape (not just the moratoriums, but the onerous costs that potentially excessive regulation imposes) is key to lowering the cost of future gas. At the margin this could help short term too, most notably in the Cooper Basin but perhaps in the Gippsland Basin too. It is all the more important for the greater challenges that will be felt through the next decade though, as the mega fields (Cooper, Gippsland and Fairview) all reach the later part of their useful life.

A clear, enforceable use it or lose it policy is also key in our minds. Ironbark is perhaps the most obvious asset here. In reality, if Origin had capital, that asset should have already been sanctioned. The perversity is that it arguably gets more valuable every day that it isn’t sanctioned, as the market gets tighter. Should that be allowed when there are now cashed up players like Senex or Beach which would seemingly be keen put the accelerator down on these assets.

Relying on Shell/QCLNG to balance the market is too risky

There has been plenty of comments from Shell about its ability to divert volumes domestically, but we think it would be perilous to rely on this as a sustainable source of supply for the domestic market (certainly at a palatable price).

It is entirely true that Shell is the only one without definitive contractual obligations out of Curtis Island as the gas goes into portfolio. If they have enough capacity in their global portfolio there is theoretically therefore no reason why QCLNG couldn’t stop exporting gas entirely.

However, the reality (justifiably) is that Shell will only sell into the domestic market when it believes prices are higher there than for LNG. So when the spot price spikes to >A$20/GJ like it did last year, of course they will supply.

The challenge about any meaningful reliance on this as a supply source is that there is a double negative as the oil price rises. Not only do domestic prices in general go up, with the linkage to oil in many contracts now, but supply will also be restricted as it becomes rational for Shell to export more.

We would also caution that, at certain prices, given its portfolio capabilities, Shell may also be economically rational to just produce less at QCLNG, not supply the domestic market and honour its LNG contracts from portfolio.

What can I say? CS, you’re hired. Get on the blower to them right now, Do-nothing Malcolm.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.