From Gerard Minack exclusively for MB.

The housing boom prevented the 2014-15 bust in mining from pushing Australia into recession. Now, just as housing may start to fade, it seems that the mining Santa is coming back. Actually, it’s not. The rise in commodity prices will not provide the same boost as in the last cycle, and Australia remains vulnerable to a turn down in housing. This is not a setting where the RBA will be hiking rates.

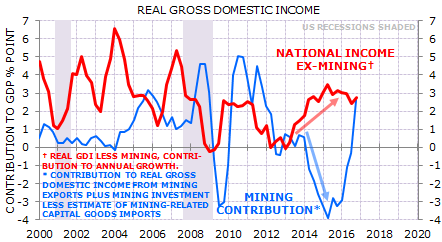

I didn’t expect this: the bust in Australia’s once-in-a-century mining boom didn’t cause a recession. That is impressive: a bone-crunching fall in mining was offset by strength elsewhere (Exhibit 1).

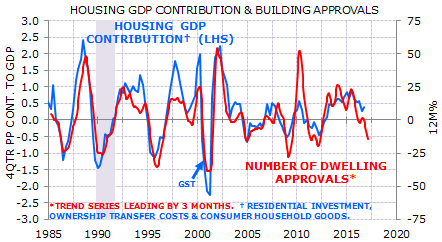

Two things provided the just-in-time offset to mining weakness. First, the A$ fell from US$1.11 to $0.68, boosting non-mining exports (such as tourism). Second, housing boomed. Housing was the more important offset in my view. The direct impact of housing – building, furnishing and trading homes – went from a small drag on growth in 2012 to adding 1 percent to GDP at the peak (Exhibit 2).

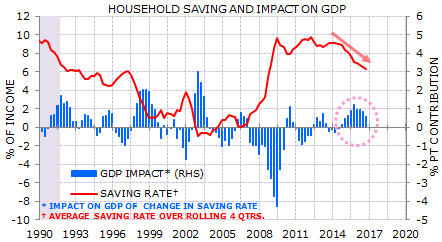

There was an indirect wealth effect as house prices rose. Australians felt richer, so they saved less. The change in the saving rate likewise turned from a small drag to adding 1 percent to GDP (Exhibit 3).

So the total housing contribution to growth did a 2-2½ percentage point turnaround just as mining became a major drag. Looking ahead, however, it seems that housing will fade through 2017 and likely be a drag on growth by early 2018: building approvals signal that the direct contribution will turn negative later this year (Exhibit 2), while house prices are likely to soften nationally through the second half of this year, damping wealth effects.

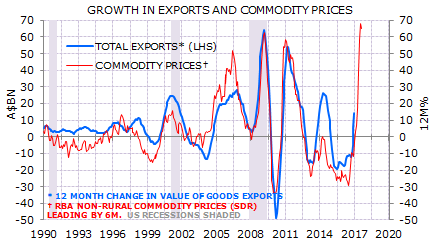

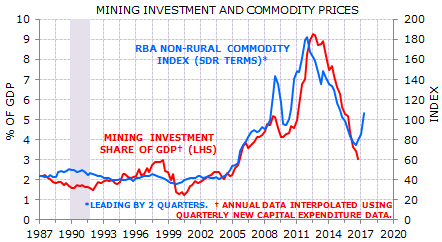

But it seems – just in the nick of time – the mining boom is back: non-rural commodity prices are rising faster now than at any stage in the prior cycle (Exhibit 4). Don’t be fooled: I don’t expect this ‘boom’ to last. More importantly, even if it did persist it is not likely to have the same flow-through to the domestic economy as occurred in 2003-08.

There are two main ways the last commodity boom boosted domestic activity. Neither seems likely to be repeated now. The first is that the mining sector lifted its investment spending as commodity prices increased (Exhibit 5). Now, however, mining investment is likely to continue to fall (although most of the declines have been seen).

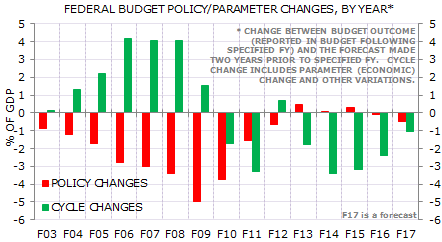

The second way the mining boom filtered through to domestic activity was via fiscal policy. The boom provided a windfall for governments. For the Federal Government the windfall was several percent of GDP (the green bars in Exhibit 6). Almost all the revenue windfall was used to fund a discretionary loosening of fiscal policy (the red bars in Exhibit 6). With the budget now in deficit I expect the Federal Government to trouser the latest windfall. (Yes, there will be political pressure on a behind-in-the-polls-government to spend more, but the countervailing political fear is that to spend the windfall now would lead to a politically damaging downgrade to Australia’s sovereign rating.)

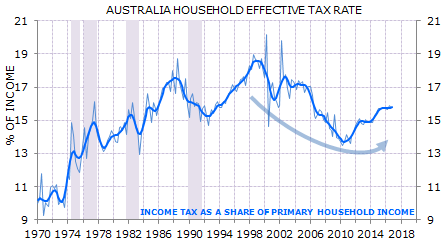

The largesse from the last boom allowed the government to reduce the effective tax rate on household income to 30 year lows (Exhibit 7). Now it has relied on bracket creep to help manage budget repair. I expect that to continue.

In short, I don’t expect this latest mining ‘boom’ to persist and, even if it does, I don’t expect it to have a material impact on domestic activity. That leaves the domestic economy in below-trend growth, with exceptionally low growth in nominal labour income pointing to anaemic consumer spending.

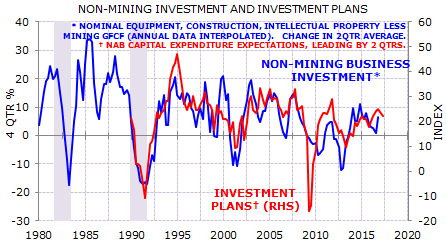

The most important potential for upside surprise is stronger investment outside mining. So far, however, leading indicators remain soft (Exhibit 8).

Nothing in this outlook points to an RBA rate hike. If the RBA moves this year it will be down, not up, in my view. However, the compelling case for RBA rate cuts will come when employment weakens, and that looks more likely in 2018 than 2017.