Macquarie stating the obvious today (but still before most others):

As good as it gets: Hedging our bets

Most questions we encounter are about why commodity stocks shouldn’t be lower rather than why they should trade higher. The bears have been on this track for more than 6 months, so we are cautious about putting more weight on the same noise. Stocks are higher and this makes the risk reward more favourable for the bears even if the story hasn’t changed. We would prefer to ask the following two questions: 1) how much downside exists if the trade begins to roll over? And 2) what is the catalyst for this to occur? The idea that there is tactical profit taking in the trade appears to be supported by momentum.

We are pairing back our commodity sector overweight preferring not to chase the greedy gains at this point. It is not a clear-cut decision, but it is becoming harder to identify upside catalysts and the hurdle for surprise is becoming much greater with expectations already incorporating a lot of the positive momentum around growth expectations (in particular China) as well as the continued support from supply side reform.

We are not negative on the sector. Total return prospects on a 12-month basis remain appealing against a market where returns will remain capped by valuation constraints, modest earnings upside and a potentially disruptive rise in the discount rate. However, there are signs emerging that point towards fatigue in the commodity trade with the sector having reached an extreme overbought level and commodities not being a big beneficiary of the pro-business (tax and regulatory) stance coming out of the US where we prefer to play this via banks as regulatory and yield curve steepening beneficiaries, JHX given its US housing exposure and LLC.

The data is not yet pointing to a roll over in the commodity trade. On the other hand, there is little evidence that Chinese growth momentum is likely to get stronger. If we are wrong, than it will probably be because commodity prices stay at current levels rather than taking another leg higher. However, bottom-up earnings expectations have played catch up throughout the entire rally and we would expect that they forced to upgrade well after the turn in commodity prices as simply arithmetic would suggest.

We could hold off cutting our allocation until there is clear evidence that commodity prices are beginning to turn down on a sustainable basis. There is support for this view including, an improving global growth backdrop, little evidence that China is slowing meaningfully, continued supply side constraints and bottom up forecasts which have further mark to market upside. On top of this there is little valuation concern for commodity stocks and in fact they currently offer some of the best cash yields across the market. Suffice to say, valuations are not a reason to sell the sector but neither are they a reason to buy it. We are more focused on what is embedded in expectations and where the momentum may go from here as signals for profit taking.

The bear points:

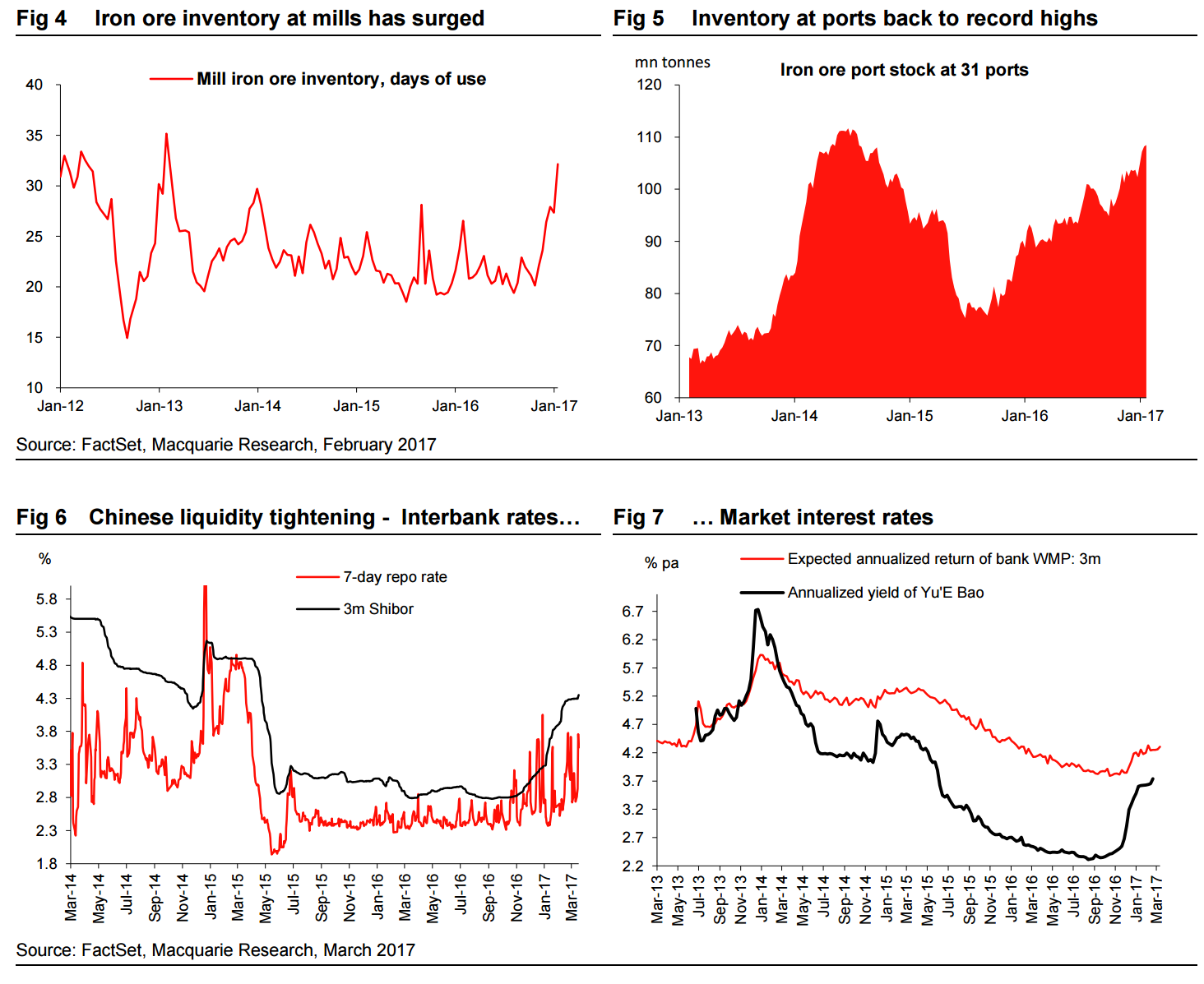

1. Chinese growth & supply side reforms unlikely to get much better: Chinese growth momentum is unlikely to strengthen much past 1Q17 due to a number of drags: 1) the property sector begins to exert a larger negative drag; 2) credit aggregates are already slowing (both M1 and M2 have already peaked); and 3) monetary policy moves remains tuned towards containing financial sector risks (the PBoC has not yet started tightening but the increase in reverse repo rates takes aim at deleveraging the bond market) rather than boosting growth. In addition, now that the CNY holidays are over, iron ore supply is abundant. Indeed, before the holidays iron ore inventory at mills had surged to highs not seen since early-2013, (Fig 4), while port inventory is back at record highs seen in 2014 (Fig 5. Full-year Chinese trade data shows the scale and origin of the supply response from the seaborne iron ore market. China’s total iron ore imports rose 71mt, or 7.5% YoY, to 1.025bn tonnes, while we estimate iron ore consumption rose by less than 1% last year (Commodities Comment: Iron ore supply continues to rise, Feb – 17).

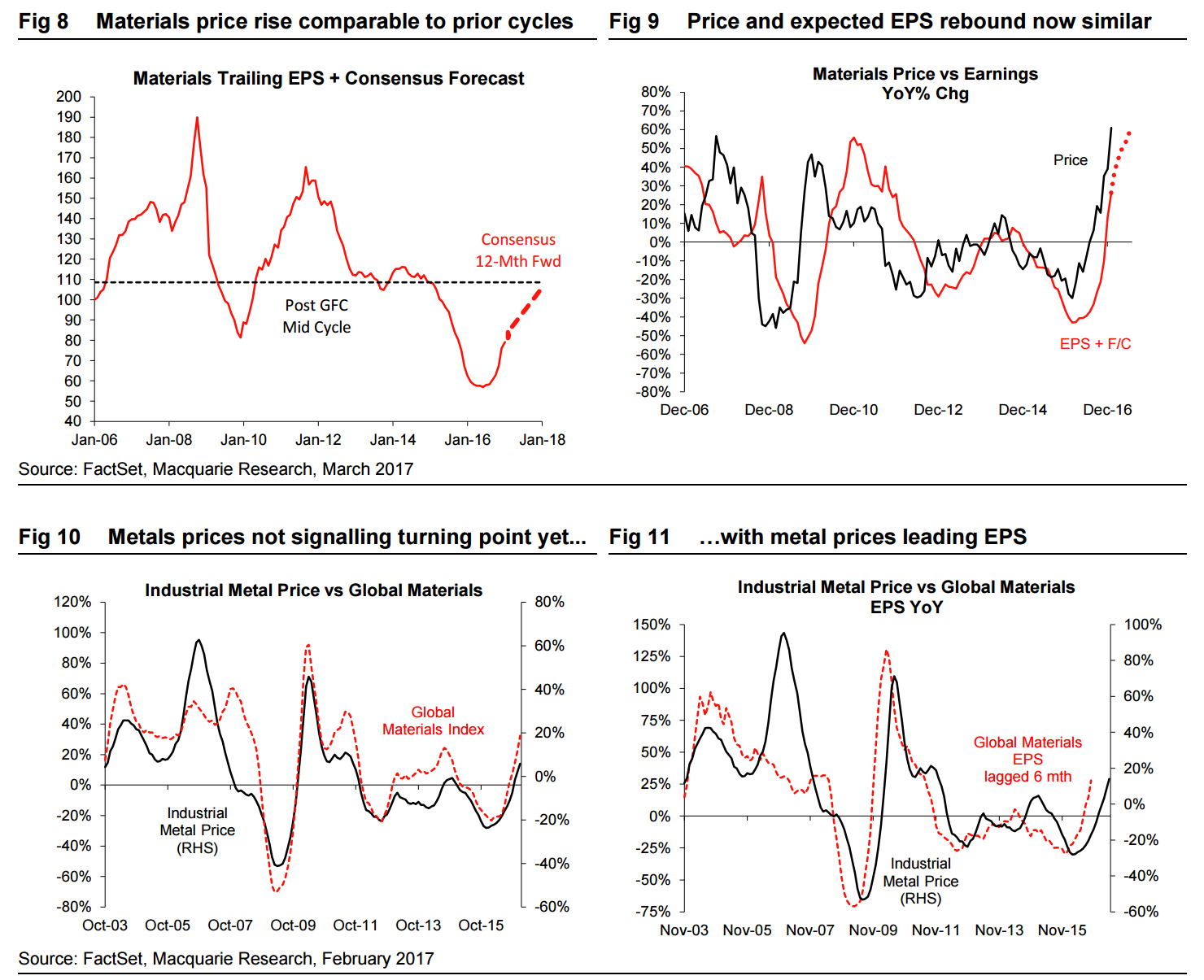

2. Stocks turn with commodity prices regardless of where earnings are headed: There is a strong correlation between commodity stocks and commodity earnings but the correlation works with a 6 month lag and historically requires both a substantial and sustained improvement in commodity prices. If momentum around commodity prices is flattening, earnings may continue to be upgraded, but stock prices on average lead the turning point (at the top and the bottom) by between 3-6 months. From a more technical perspective, the Materials sector is now running year on year at its highest ever gains – exceeding even the bull market (2003-2005) and the recovery coming out of the GFC.

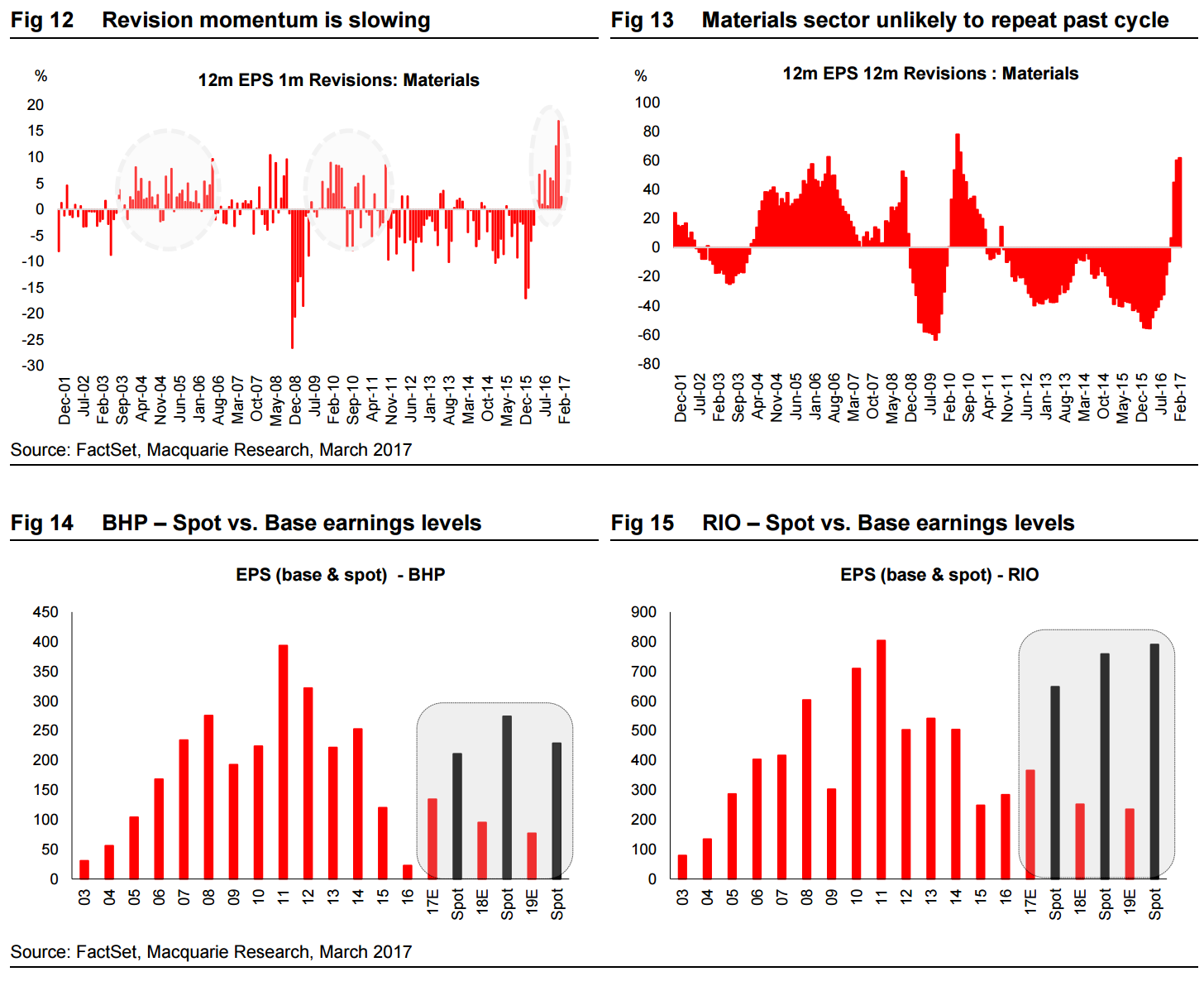

3. Earnings revision momentum slowing despite continued upgrades: February marked the 11th month of consecutive earnings upgrades for the sector with December the strongest month ever recorded. Based off the current 12 month forward expectation, earnings are now less than 10% below the long term mid cycle level. Analysts still need to catch up to spot commodity prices and the mark to market game that has been ongoing for a year will continue even if prices begin to decline. It’s simple arithmetic that unless we go from spot back to the average forecast instantaneously that it will still drive upgrades. More relevant, we now need to assume that this cycle will begin to replicate the scale of recovery seen during the commodity bull market (2003-05) and/or the post GFC rebound (2010/11) in order to keep the earnings story going.

4. Positive surprises required to keep momentum going: Strong operational results, dividend increases and potential capital management are already in expectations (as RIO showed). Upside surprises are becoming increasingly necessary to carry current price momentum even if stocks do not look expensive. Gains from cost cutting have already peaked and we expect only a small uplift in capex spend over the next 12 months (BHP, RIO, STO) which is helping to support cash flow dynamics going forward. In the short term (6 – 12 months), we expect the current pipeline of projects to remain relatively stable with the market unlikely to be surprised with announcements of new and material resource projects (projects in the pipeline were announced in the latest quarterly round) although it is also unlikely that management are talking about increasing capital spend at this stage. The trend is now increasingly towards cost cutting technology (rather than focusing on production volumes) and these benefits are we are early stage of the adoption curve.

Portfolio Changes

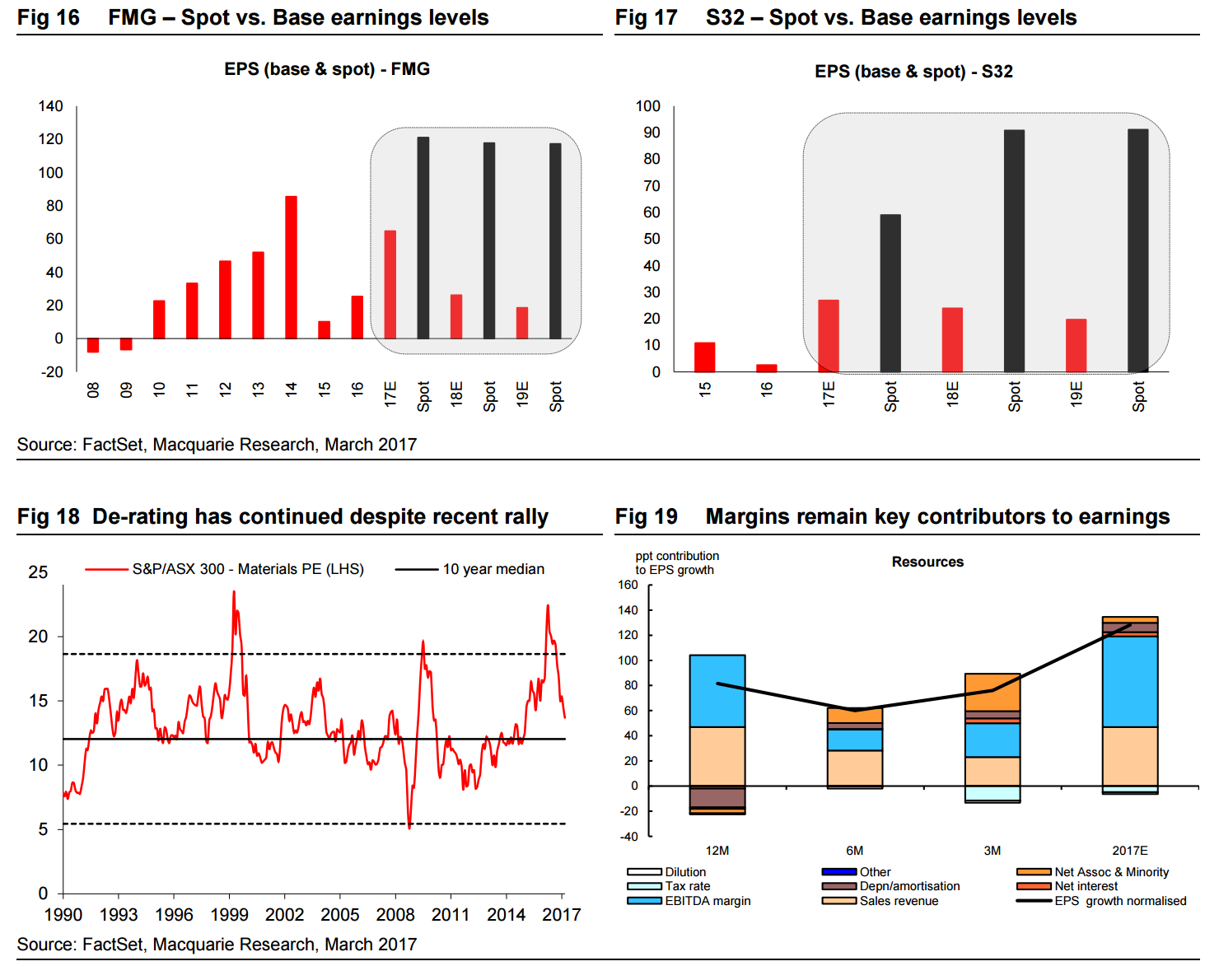

We have reduced our overweight position in the miners. We take some profits on and reduce our holdings in Rio Tinto (RIO AU, A$61.60, Outperform, TP:$76.00, Hayden Barstow) and Fortescue Metals (FMG AU, A$6.62, Outperform, TP:$6.80, Hayden Barstow). We are finding it harder to identify broader upside catalysts that are not already factored into expectations, which is raising the hurdle for positive surprise. Our preference (and bigger bets) within the sector is for BHP (BHP AU, A$24.64, Outperform, TP: A$30.00) for its solid cash generation, and as the miner has stepped up its dividend payout ratio and is now well placed to fund its organic growth projects, and South32 (S32 AU, A$2.72, Outperform, TP: A$3.70) as another strong cash generating quarter creates upside risk to the S32 interim dividend.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.