The Australian property bubble has grown so absurdly large, and is so connected from the sad little economy beneath it, that it is consuming everything in its path.

The latest example comes from economist Saul Eslake, who will address the Conference of Major Super Funds today, whereby he will warn that Australia faces a looming rise in pension costs, as many people who are set to retire over the next 10 years will use their superannuation to pay off their mortgage rather than to fund their retirement. Eslake says home ownership has fallen to its lowest level since the 1950s, noting that there has been a growing trend for people aged 55-64 to still have a mortgage. From The AFR:

“This is a group who over the next 10 years is either going to become retirees who still owe something on their mortgage or, more likely, retirees who’ve used their super to pay off their mortgage and will go on the age pension”…

He said a “hidden assumption” of the system was that people’s housing costs in retirement would be low because they owned their own homes.

But demographic and economic shifts were making that assumption less valid…

“The overall home ownership is the lowest it’s been since 1954. And it’s not just young homebuyers, but middle-aged adults among whom ownership has been declining as well”…

The number of homeowners aged 55 to 64 with a mortgage tripled to 44 per between 1995-96 and 2013-14…

“If people use their superannuation to pay down their mortgage then they are obviously not going to have as much superannuation and may not have any at all, and will therefore quality for the pension.”

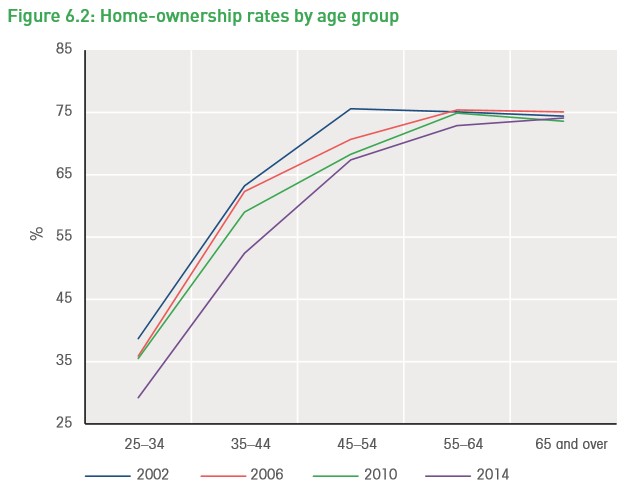

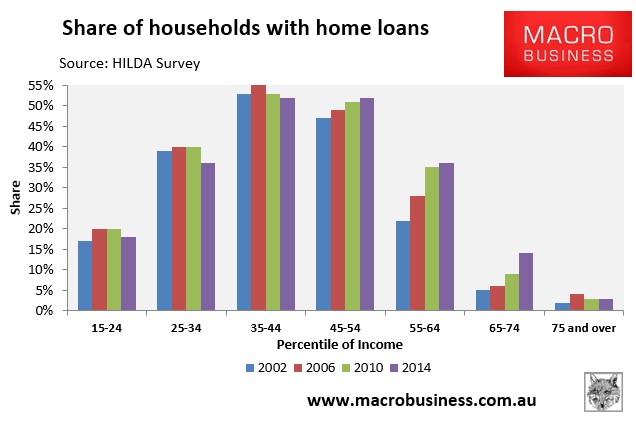

Here’s are the charts confirming Eslake’s argument.

First, note the decline in overall home ownership. While the decline has been greatest among younger cohorts, it has affected the middle-aged as well:

Worse, note the sharp rise in over-55s with a mortgage:

Elsewhere, Saul Eslake backed MB’s call for APRA to immediately lower its investor loan speed limit to 5%.