Hello, APRA, anyone at home? 2.0

Hello, APRA, anyone at home?

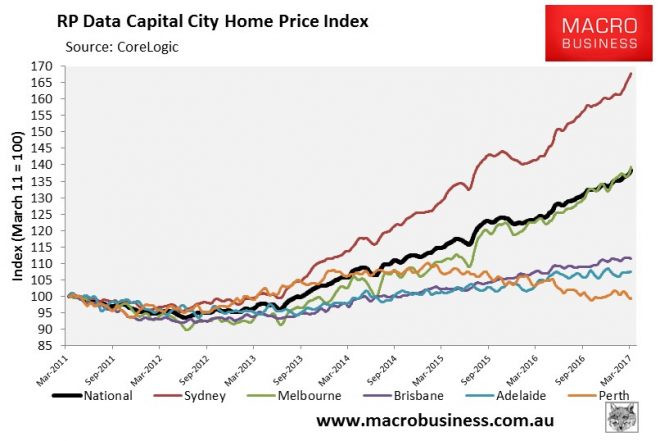

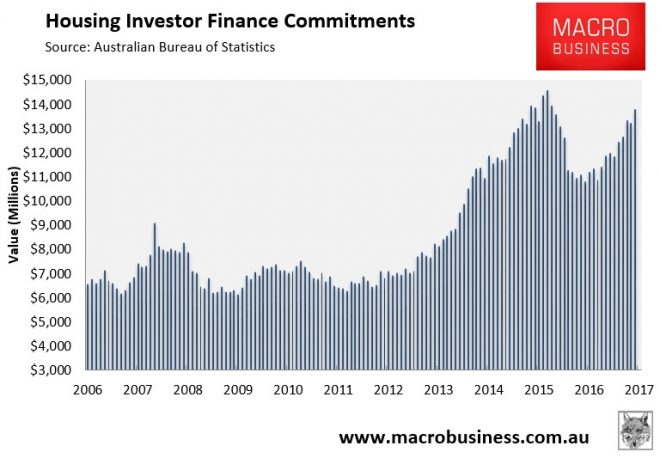

And the driver? 27.5% year on year growth in investor loans, out today:

The bubble is back, APRA, and you need to tighten right away.

There is no reason for the RBA to tighten vis inflation. It should actually be cutting. The economy also needs lower rates. But you can’t sail on into a financial catastrophe, either.

It’s blindingly obvious that APRA needs to cut the investor loan speed limit to 5%. With three quarters of investor lending pouring into Sydney and Melbourne, it will implicitly be geographically targeted. The RBA can then cut again and the dollar will sink like a stone into the 50s cents. That will prevent any bust and accelerate the real exchange rate adjustment that we need, less credit and more tradables.

The only other targeted option is fiscal tightening, like cuts to capital gains or negative gearing tax concessions. Perhaps APRA is waiting for the Budget. It shouldn’t. Whatever it is it will not be enough.

The alternatives are clearly worse. If the RBA is forced to tighten until the bubbles pop then we’ll very likely see a recession. The 2002 double-hike combined with house price jawboning hammered Sydney house prices. Doing that as the dwelling boom comes off will be seriously pro-cyclical.

If neither the APRA nor the RBA move then we could see this run another two years then blow sky high when the Fed pops the Trump boom. That is the financial stability worst case.

Someone needs to tighten now. There is no other responsible choice. As Dr Hewson wrote late yesterday:

…our whole system is at risk of a significant drop in house prices as, indeed, was the US/global financial system in the run up to the global financial crisis, where the mountain of debt was built on a US sub-prime housing loan, which was simply a punt on house prices not falling.

Our banks are, today, heavily exposed, having become essentially building societies that also issue credit cards. These exposures are over and above their considerable climate exposures – not just to mortgages on coastal properties, and to fossil fuels, but more broadly.

The risks being run actually dwarf those of the GFC. If it goes bad, the government will be called on to intervene.

Hello, APRA, anyone home?