GMO / James Montier hit on a lot of the themes near to my heart with a recent piece on secular stagnation and the rise of populism:

The rise of populism has been one of the broad themes to emerge over the last few years. This has left many within the establishment scratching their heads as to the cause of their fall from grace. From our perspective, the rise of populism has its roots in the same sources that have given rise to socalled “secular stagnation.” That is, a broken system of economic governance. This system – which we will hereafter refer to as “neoliberalism” – arose in the mid-1970s and was characterised by four significant economic policies: the abandonment of full employment as a desirable policy goal and its replacement with inflation targeting; an increase in the globalisation of the flows of people, capital, and trade; a focus at a firm level on shareholder value maximisation rather than reinvestment and growth; and the pursuit of flexible labour markets and the disruption of trade unions and workers’ organisations.

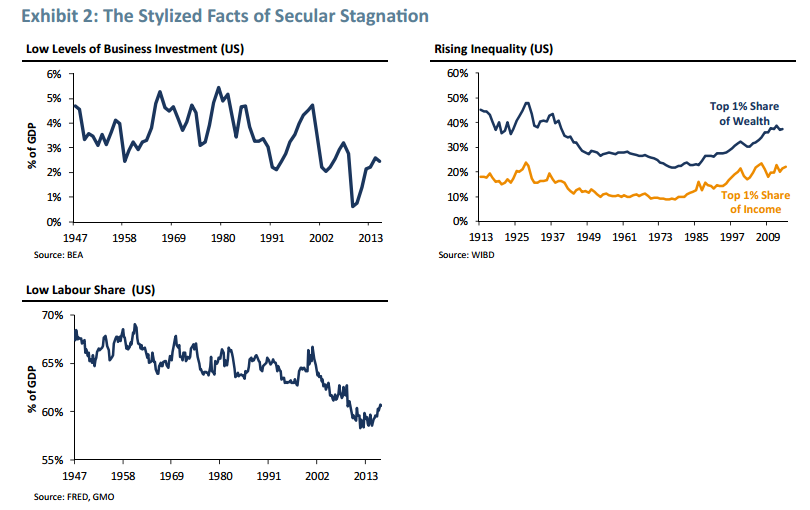

The long-term themes are very similar to my “6 mega-trends” and have rising inequality at the heart of the lack of demand.

Rapid increases in debt hide the lack of demand for years at a time – and a debt-funded Trump boom will be no different. But the underlying weak demand trend re-emerges after each boom and I expect if the proposed Trump tax cuts and infrastructure spend go through that the US economy will boom, but that it will also bust leaving it in a worse position with the trend in tact.

So, I agree with most of the diagnosis.

The GMO solutions? Not so much.

Inflation Targeting and the NAIRU: Policymakers have been telling central bankers to steer the economy using monetary policy while always keeping an eye open for the non-existent NAIRU in order to shirk responsibility for maintaining full employment. This is no longer acceptable. Fiscal policy is a far more effective tool to maintain full employment… …The government offers a fixed wage for any labour that is forthcoming. This wage acts as the de facto minimum wage, below which no labour will be forthcoming to private sector employers. When unemployment is high, workers will flow into the government scheme, and when the economy starts to grow, private employers “hire off the top” of the scheme by offering a wage above the NAIBER wage. The workers can be outsourced to private charity groups to do any number of jobs that are currently not done. They might clean rivers, help the disabled, care for the elderly, clean up graffiti, plant public gardens… the list of potential useful things these people might do is boundless.

Globalisation and Trade: The best way to deal with this problem is for governments to run a beefed-up policy of import substitution. Import substitution works by governments identifying the products that are currently imported from abroad that could easily be produced domestically. So, for example, cheap Chinese toasters are probably substitutable, while foreign diamonds are probably not. The government then offers significant direct subsidies to companies that are willing to produce these goods. The subsidy is then passed through to the consumer as a lower price, which will render the product competitive with the cheaper foreign good.

Shareholder Value Maximisation (SVM): SVM is not the result of a policy choice. It is the result of a shift in how corporations govern themselves – a corporate choice, not a government one, if you will. It can easily be stopped if corporations take it upon themselves to stop engaging in it. As we have seen above, doing so will probably render them more profitable and more competitive. Beyond that, we would simply say that while we do not think of SVM as a policy choice, a government in the future may begin to think of it in these terms if corporations do not get their own houses in order. If they value their independence they might heed this warning now before it is too late. Populists have policies too, you know.

Flexible Labour Markets: The NAIBER policy mentioned above will give workers a far stronger bargaining position as they will no longer be as fearful of unemployment. It will also implement a de facto minimum wage that will be impossible for unscrupulous employers to evade. In addition to this, a serious import substitution and industrial policy will help return high-wage, (often) unionised jobs to developed countries. But none of this is a substitution for governments promoting reasonable, equitable policies to allow for unionisation.

Unfortunately mostly a suggestion to return to the 1960s/70s.

None of these are unlikely to see the light of day without a crisis: ending inflation targeting, government intervention in the labour markets to re-target full employment, adding a variant of trade protectionism, ending shareholder value maximisation (I suspect this one is up there with “World Peace” in terms of likelihood), increasing unionisation.

The full employment suggestion is the most interesting of their propositions to me – especially as increasing automation in manufacturing, logistics and transport is going to see a big increase in unemployment over the next 20 years.

There are any number of ways to reverse the building inequality, some of the GMO suggestions should be in the mix. However, the bigger issue is that no one is seriously trying anything to reduce inequality at the moment. In fact, the opposite is happening.

Sadly, we will need a major crisis before the 99% resume protesting and governments pay lip service to addressing the issue while really making things worse seriously consider the issue. Until then, your Asset Allocation should reflect an eventual return to secular stagnation.

Damien Klassen is Chief Investment Officer at the MB Fund launching in April 2017. Register your interest now (if you haven’t already):