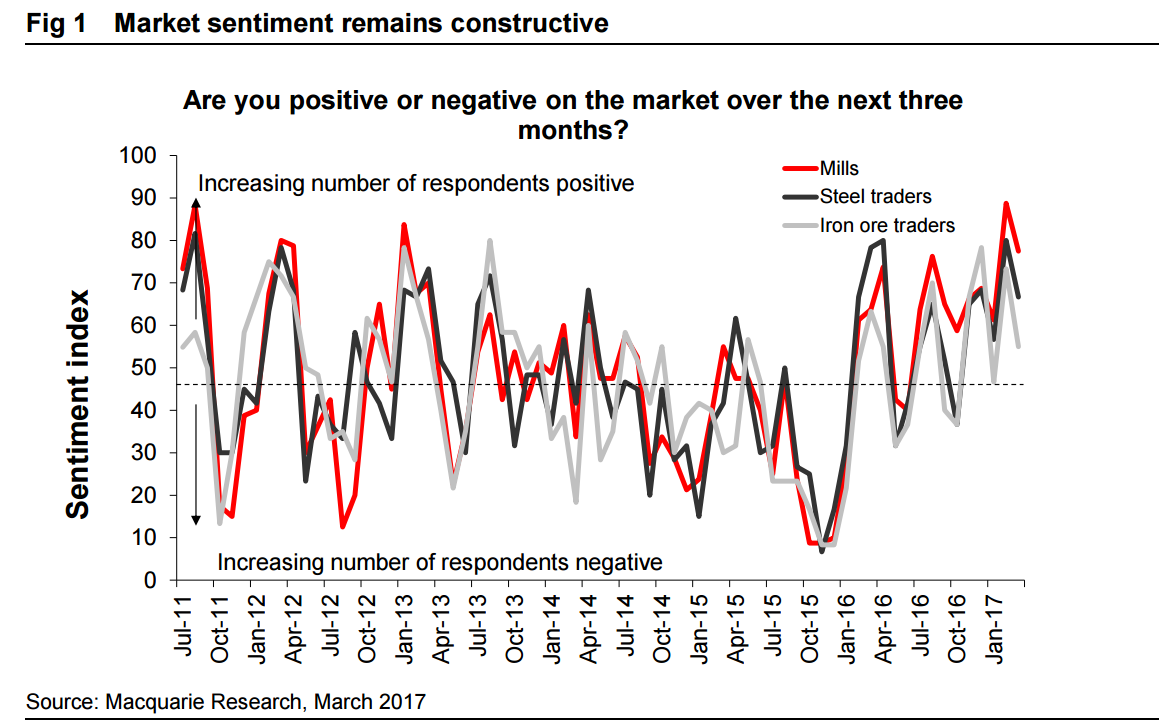

Steel sentiment softened slightly from five-year highs but remains at historically elevated levels, especially among steel mills. Mill profitability is extremely high, and production is starting to lift, led by medium-sized mills. Seasonal norms are well under way, with construction and infrastructure demand picking up into the spring construction season and steel inventory on the decline accordingly. The overall outlook for the steel market remains constructive; however, the restocking cycle in iron ore appears to be nearing an end, with iron ore traders the least optimistic group in our survey.

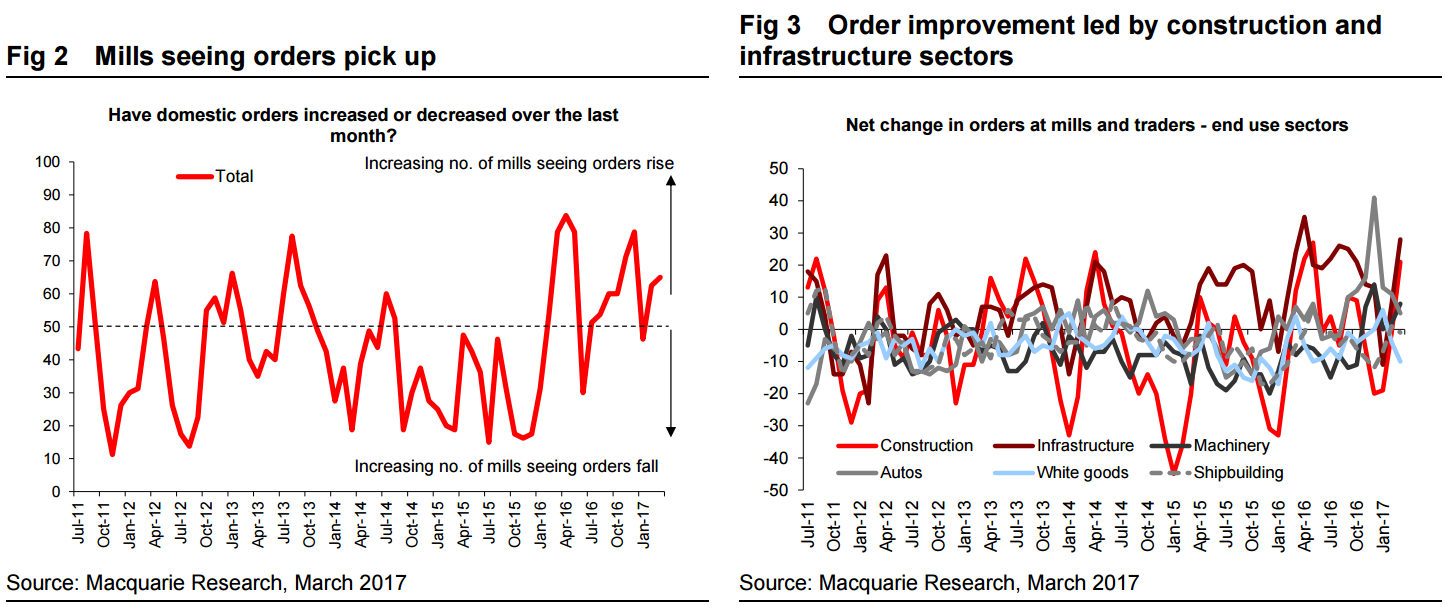

Orders and sales: The post Lunar New Year pick-up in orders is starting to come through as expected, with infrastructure and construction sectors leading the upturn, as usual. Orders from the appliances sector have weakened a little, while the pace of improvement in orders from autos has slowed, which is only be expected given the slowdown in auto sales to 7% YoY growth in the first two months of the year versus 15% for 2016.

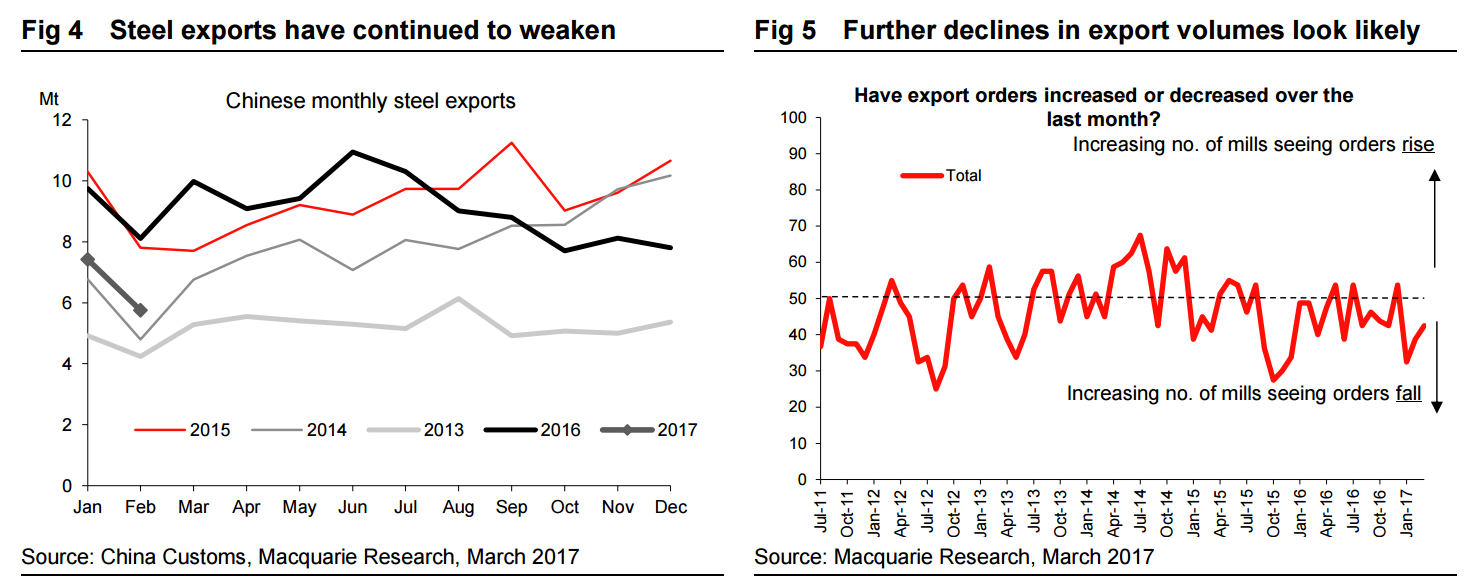

Steel exports: As expected, Chinese steel exports continued to fall in February, down to 5.75mt, their lowest level in three years. Mill survey respondents indicate that export orders remain weak, which is largely to be expected given the high steel prices in China. As we wrote recently, Chinese steel exports have become increasingly uncompetitive, especially versus EAF production elsewhere due to low scrap prices, and we expect Chinese steel export volumes to remain weak until steel prices domestically fall back.

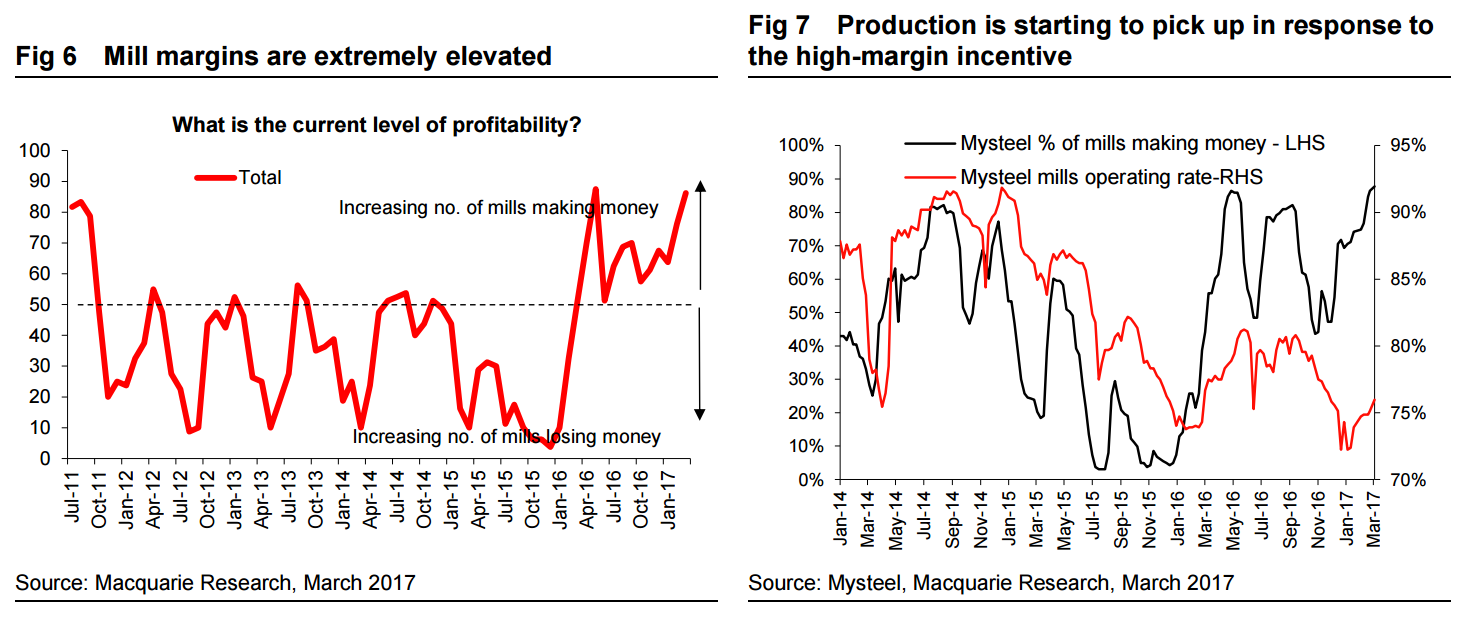

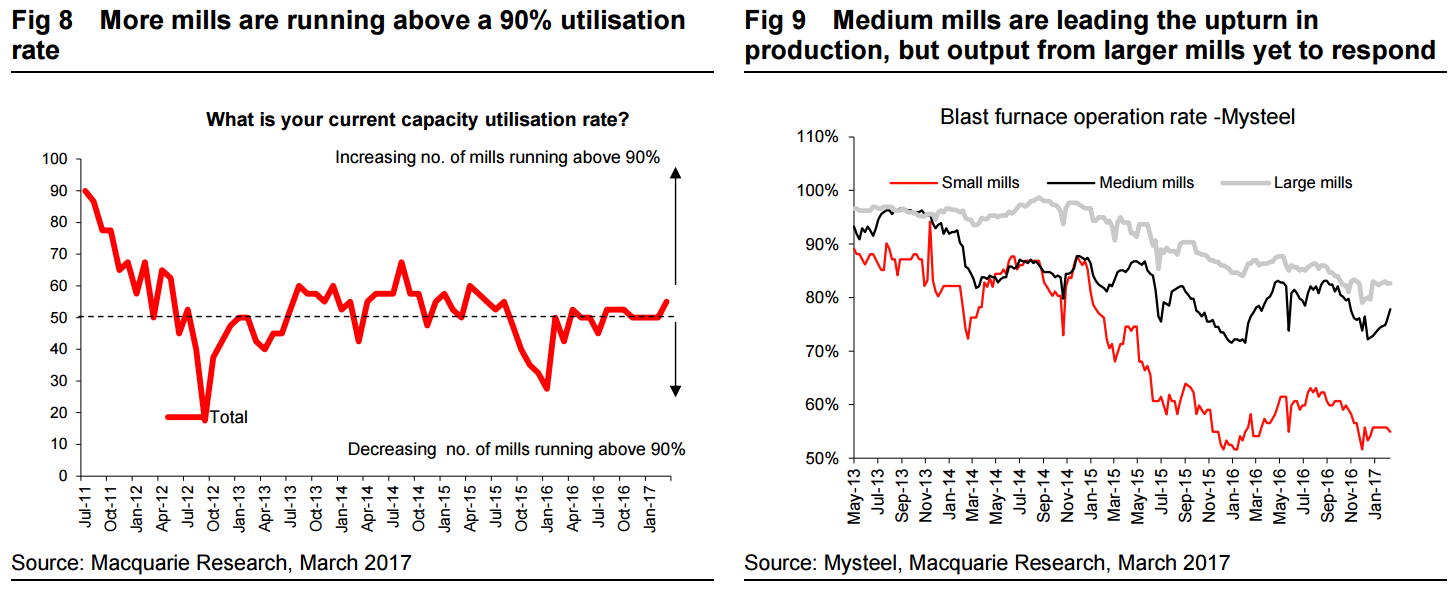

Production and profitability: With profitability high, steel mills have begun to lift steel output following the holiday period. The key questions for steel prices over coming weeks will be whether steel mill output only keeps pace with steel demand or starts to accelerate ahead of it. Mysteel data shows capacity utilisation rates are picking up from extremely low levels, with medium-sized mills leading the way. With the margin incentive currently so high, we expect mill output to jump sharply in coming weeks, as steel output remains well below a level at which capacity would start to look constrained.

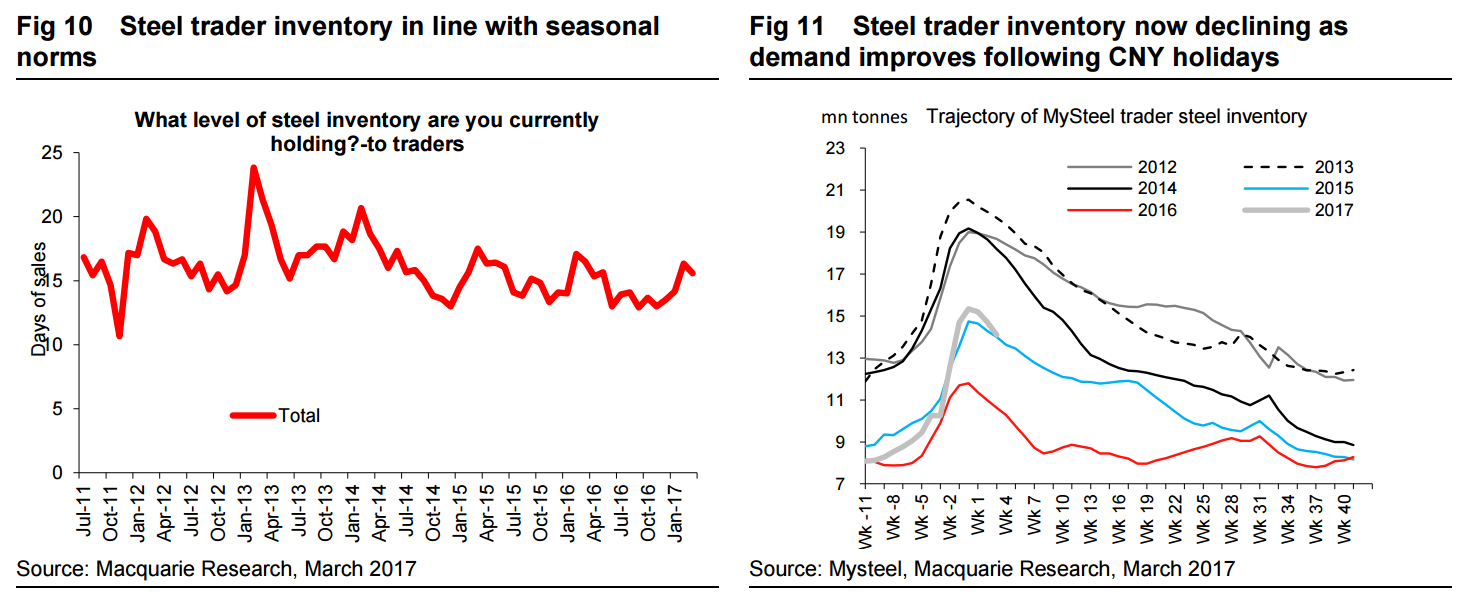

Inventory: Steel inventory at traders looks to be behaving in line with seasonal norms, coming off in recent weeks as demand picks up post the holidays. The fact that steel inventory is falling while steel prices remain elevated suggests that the inventory drawdown is demand-driven rather than traders being eager to sell. Only when steel production starts to rise ahead of demand will we likely see steel prices come under pressure.

Raw materials: Iron ore restocking appears to be easing, as steel mills look well covered for their forthcoming ramp-up in steel output. Steel mills are not yet planning to cut iron ore purchases, however, and iron ore prices should continue to be supported while steel prices remain elevated.

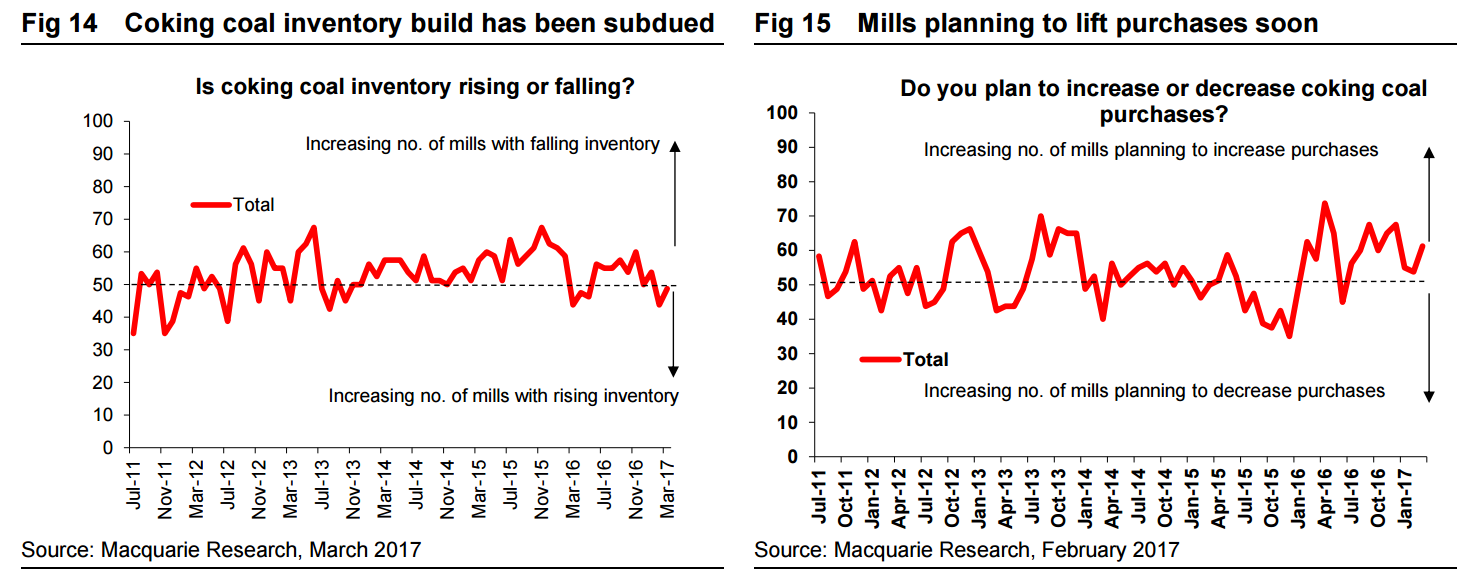

Mills are looking to raise coking coal purchases more so than iron ore; however, this is more due to inventory already being at lower levels rather than any great desire to restock. It is becoming clearer that there will likely be no restrictions on coking coal output in China from the end of March, as we heard on our trip to Shanxi recently, and this is likely to dampen mills’ eagerness to build coking coal inventory to too elevated levels.

That accords precisely with my current assessment of the market:

mill output and orders solid;

steel prices too good to last;

inventories high, especially factoring in easing macro;

coking coal in need of more restocking, and

iron ore has only one way to go but will be supported a little until coke restocked.

I’ll guess that we’ll be sub-$70 by mid-year and sub-$50 by year-end but as said before it all hangs on sentiment and the overall restock.

Advertisement

Credit Suisse has an interesting counter-take:

Despite the NDRC being hostile to further steel price increases, there is potential upside from capacity closures that may greatly raise capacity utilisation.

Mysteel reported the news as follows: “Is the shutdown of substandard steel capacity counted in the 50 million tonnes of overcapacity cut target in the government work report this year?” “It is not!” Being deluged with these questions after a news conference on March 11, Miao Wei, minister of Industry and Information Technology, gave a resolute negative answer.

50Mt is the existing capacity cut – induction furnaces are extra

To put this in context, the government’s steel capacity closure target for this year is 50Mtpa, as affirmed from the NPC. This was in line with the street’s expectations, as part of the 150Mtpa of capacity closures due before 2020. Last year 65Mtpa of steel capacity was closed. Late last year, we also heard about induction furnaces. Premier Li was reportedly surprised to learn that steel mills had erected unapproved furnaces that melt scrap and were producing low quality steel as construction products. The induction furnace route apparently allows little quality control. The composition and therefore strength of the steel products is unknown, and thus they are clearly unsuitable as structural components. The government vowed to shut these furnaces down.

Mysteel thinks there is about 100Mtpa of induction furnace capacity

We were assuming that the induction furnace closures would be part of the 50Mtpa to exit this year. We don’t know how much induction furnace capacity exists – we doubt anybody does – Mysteel last year termed it “secret capacity”. However, a common estimate in the street is somewhere around 30Mtpa. Mysteel disagrees: “According to incomplete statistics, the output of the subpar steel products could amount to almost 100Mt, the crackdown of which will certainly tighten the supply of steel products, especially rebar used in construction”.

If Mysteel is right – 2017 steel capacity closures could reach 150Mtpa

So Mysteel believes China will need to close down 100Mtpa of low quality capacity – due to be completed by 30 June – and then find another 50Mtpa of steel capacity to close to meet the NPC target. In total, 150Mtpa of capacity is to be exited. There is debate about what China’s actual steel capacity currently is. But irrespective of this, utilisation is set to become a lot tighter again in China this year if Mysteel’s estimates are correct. And most of that should occur in 1H – the period when steel output is greatest. In fact, there is now a risk that China overshoots the steel capacity tightening and does a “met coal” to the steel price. Trina Chen wrote about that risk in a number of industries…

After last year’s coking coal policy debacle and pull back is it really a reasonable proposition that they do it again in steel? You have to assume a lot of stupidity.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.