The (nearing) end of private sector deleveraging in DM

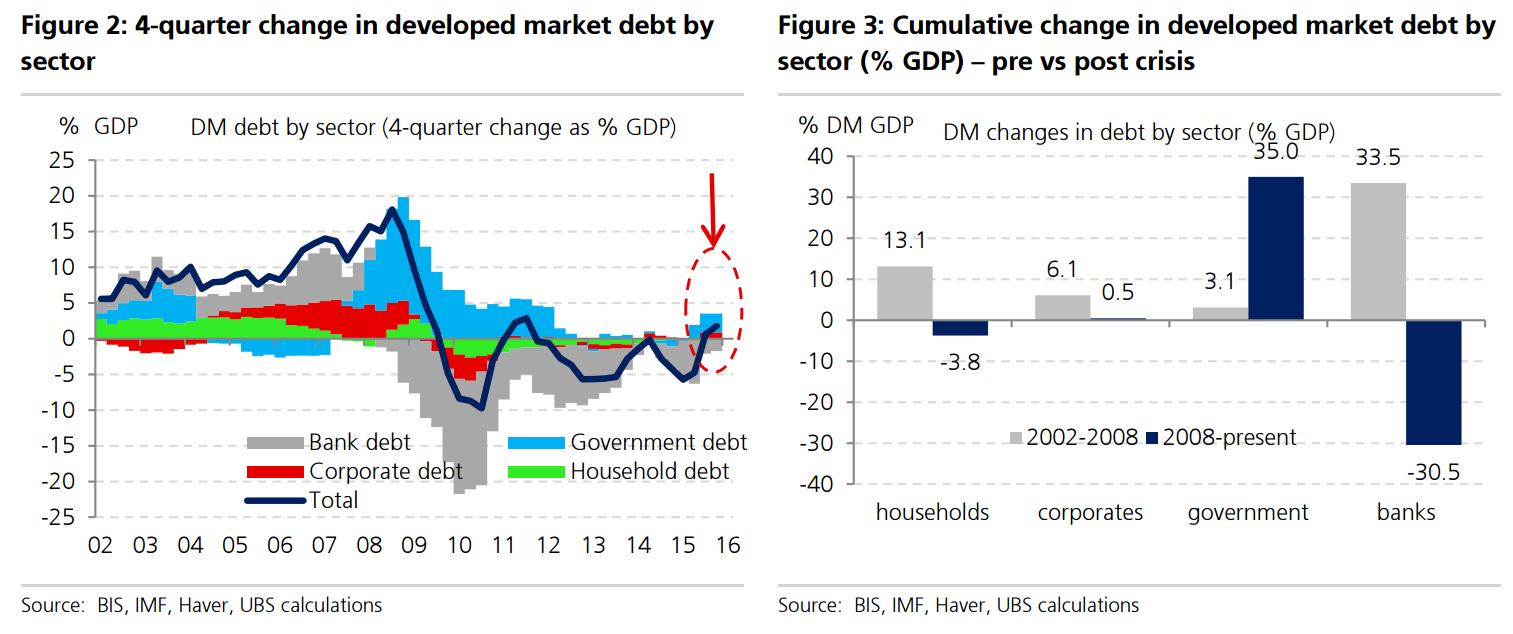

Conventional wisdom is that there has been little post-crisis deleveraging. And that is true, if one looks only at households, corporate and government balance sheets: the combined debts of these sectors globally went up 35% of global GDP between ’02 and’08 and then another 73% of global GDP after the global financial crisis. If we include the financial sector, the pre-crisis build-up in debt rises to 55% of global GDP, and the post-crisis debt build-up declines from 73% to 51% of global GDP. But that post-crisis debt increase still doesn’t make for very pleasant reading if one is a proponent of the debt-super-cycle theory of how growth is ultimately supposed to recover1 And history suggests recovery from crisis is slower when multiple indebted sectors are involved.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.