The US dollar fell hard Friday after more jawboning from the Trump administration:

Commodity currencies rebounded:

Gold held on:

Brent is still stuck:

Base metals firmed:

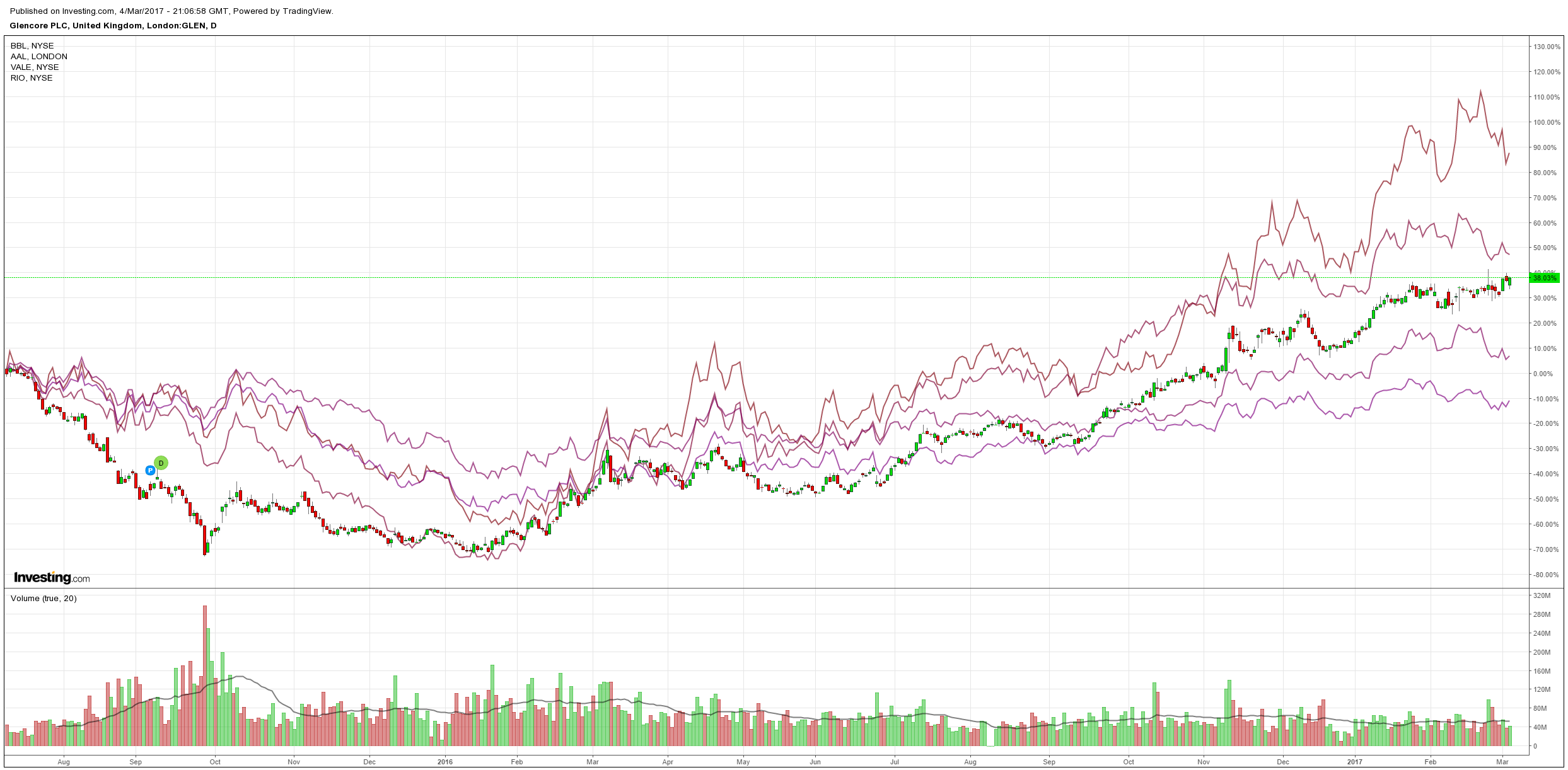

Big miners too:

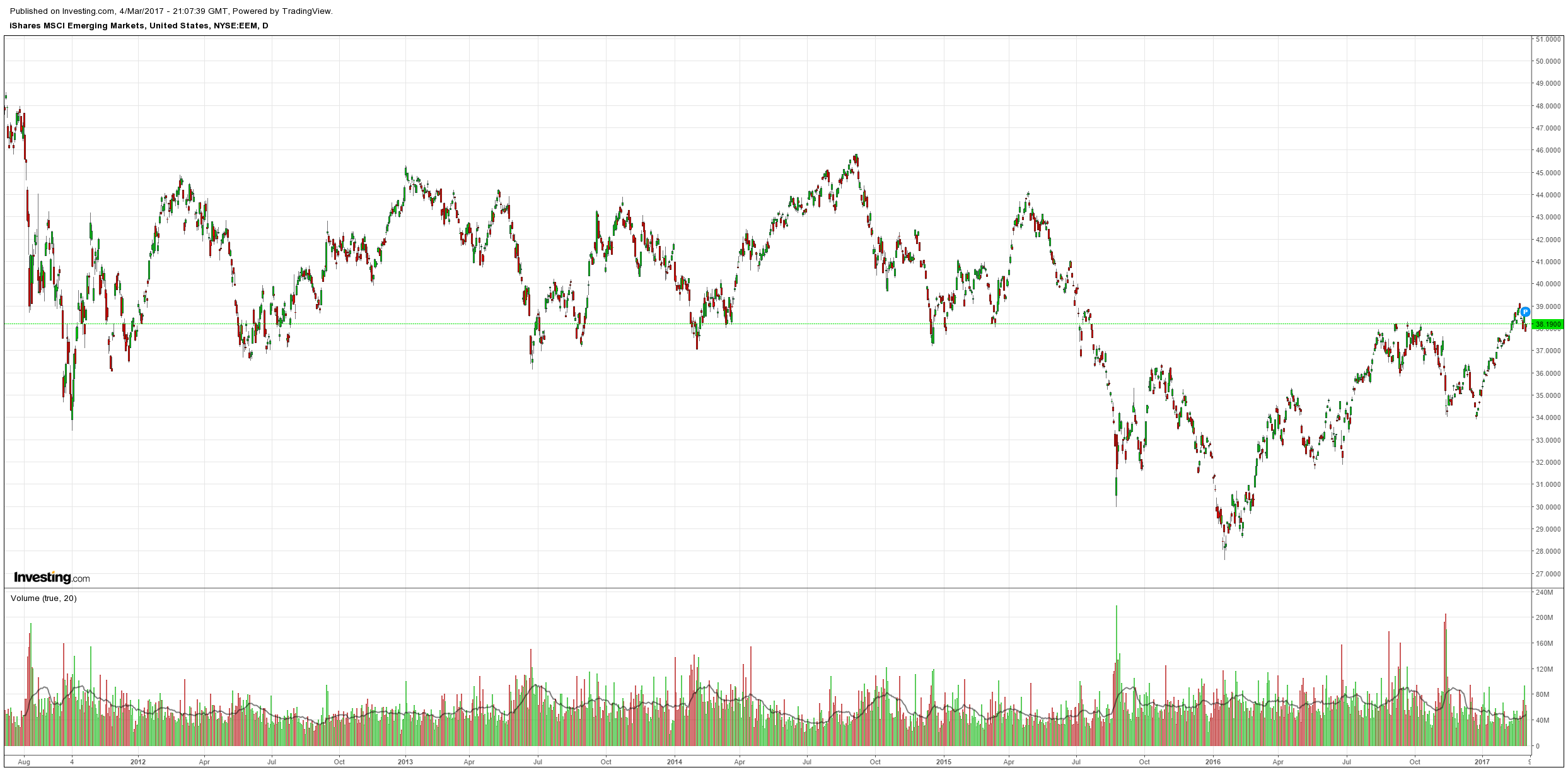

EM stocks rebounded:

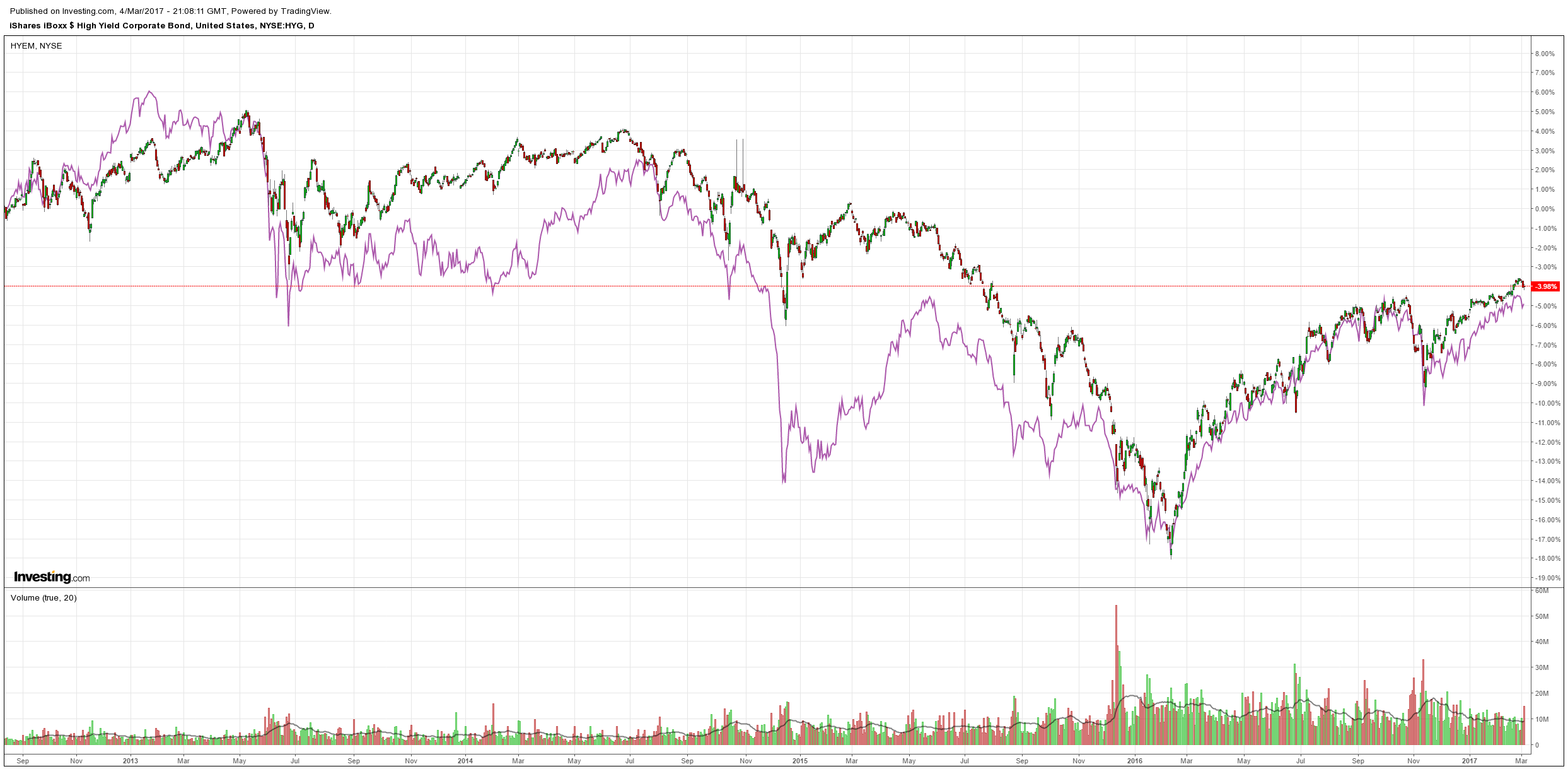

And high yield:

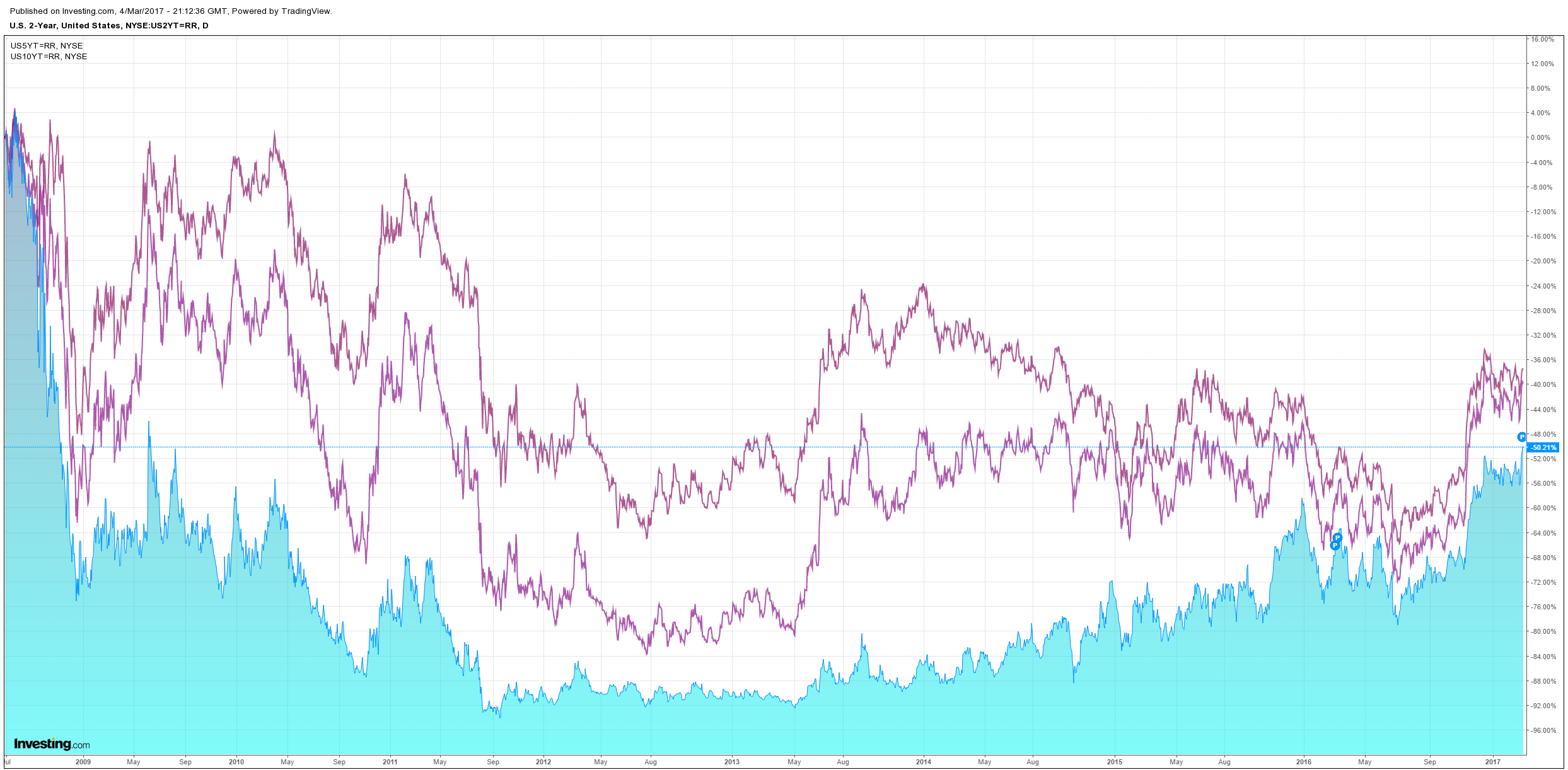

US bonds were hit:

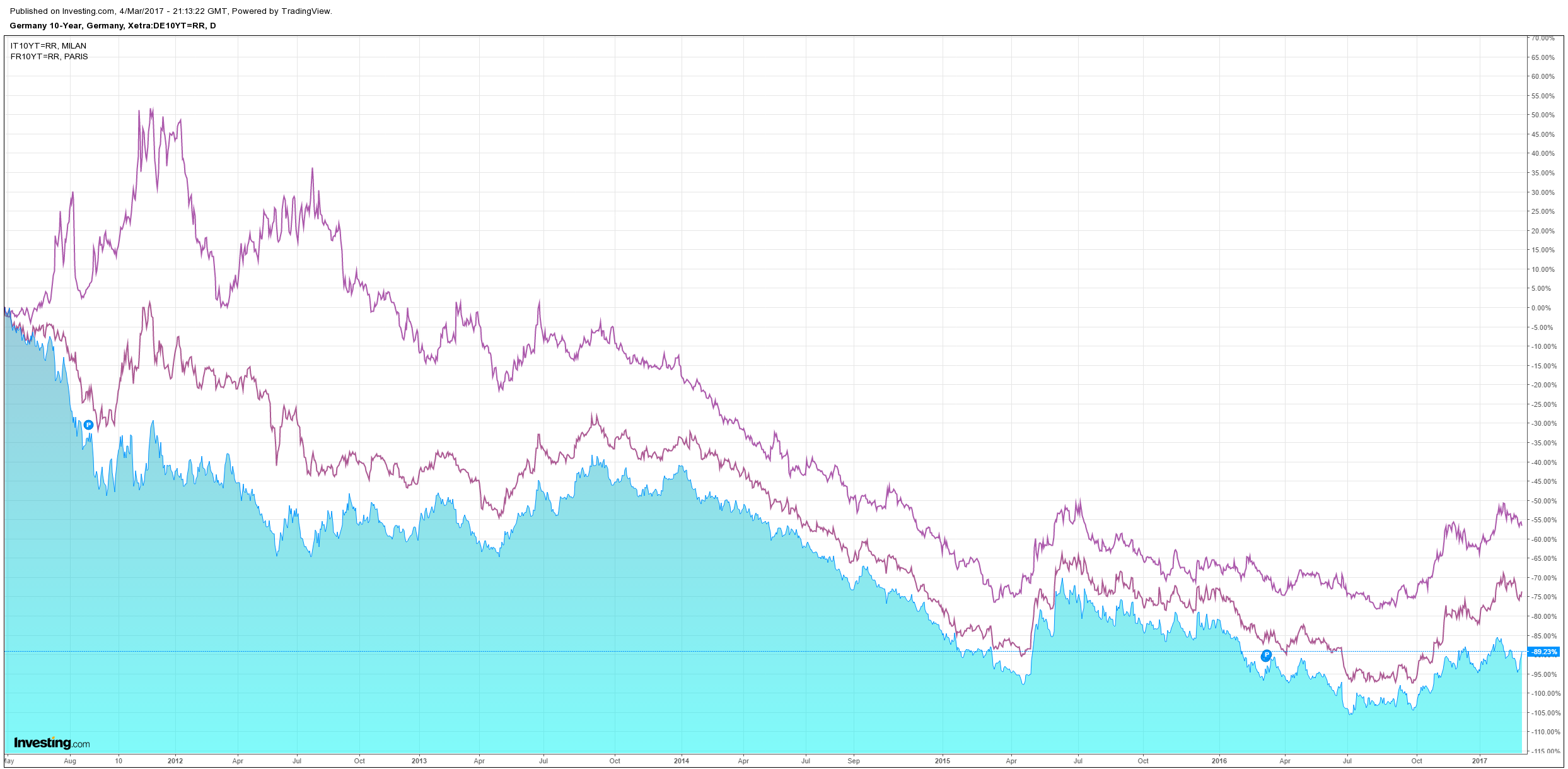

European spread were mixed:

And stocks flat:

Janet Yellen confirmed the March hike:

[W]e currently judge that it will be appropriate to gradually increase the federal funds rate if the economic data continue to come in about as we expect. Indeed, at our meeting later this month, the Committee will evaluate whether employment and inflation are continuing to evolve in line with our expectations, in which case a further adjustment of the federal funds rate would likely be appropriate.

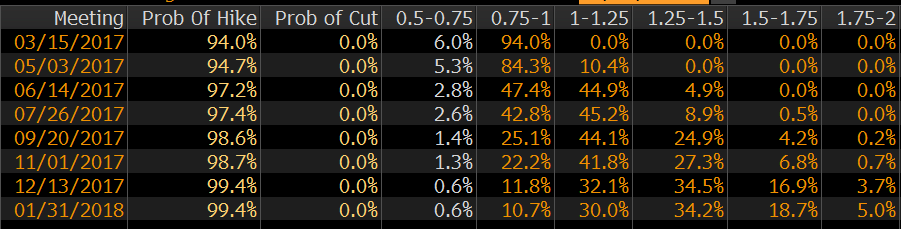

Fed funds futures priced a 94% chance for March, followed by favourites for July and December:

The die is set. We’re going to see an ongoing struggle between Trump fiscal policy and the tightening Fed driving up the USD on one hand, and the Administration trying to talk it down on the other. Markets ought win in the end.

More and more Aussies apparently agree, via The Australian:

Spurred by swelling optimism in the US economy, Australia’s wealthiest investors are increasingly shuffling their cash into US-dollar-denominated accounts.

In part a Trump effect, investment bank Citi logged a “sizeable” $US100 million ($132m) — or 20 per cent — surge in US dollar cash deposits from November 1, 2016, until February 1, 2017, among its local high-net-worth clients.

The majority of the money flow came across December and January as investors digested the potential of the so-called “reflation” trade and the prospect of Trump’s promised $1 trillion spend on US infrastructure projects.

“Our US dollar balances have generally been growing. But in this instance we’ve seen substantial growth from November to now,” Citi investment strategist Simson Sanaphay told The Weekend Australian.

As Sanaphay explains, the switch into US dollars represents an acceleration of a trend to diversify the cash component of portfolios beyond the Australian dollar in light of the unit’s underperformance in recent years. He pointed to three reasons driving the uptick in US dollar demand.

• The convergence of pay-offs in Australian and US-dollar-denominated investments, with similar returns now seen across fixed-income products.

• A growing expectation of expansionary fiscal policy and rate hikes in the US, or “monetising the Trump-Fed factor”, as Sanaphay puts it. This compares to the anticipated neutral monetary and fiscal policy in Australia for the coming year or two.

• A deeper trend to view currency as more than just a speculator’s domain.

“Investors are now beginning to see the advantage of overlaying currency positions to their investment allocations because currency does actually provide an ability to hedge for the local currency, which we’ve seen underperform, but also potentially amplifying returns as well … And that’s what we’ve been seeing, particularly in this instance when a lot of the market is expecting the US dollar to strengthen.”

Well…we do have a surprisingly powerful readership…

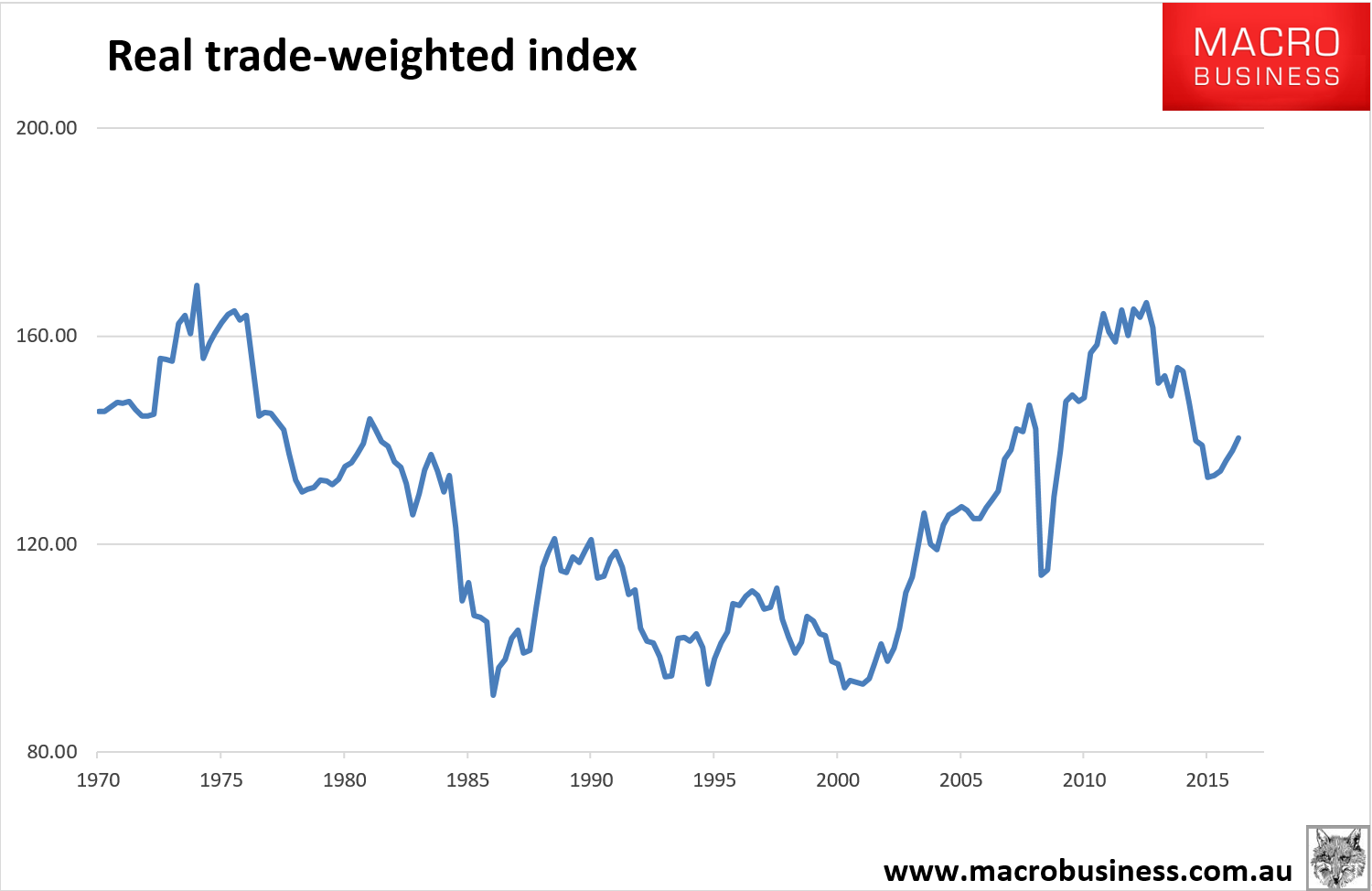

An associated question is how long should one stay long the USD? Hard to say given the Trump uncertainties. It’s been rewarding trade for MB since we turned bearish AUD in early 2012 and we still see big downside for the local currency over time (to sub-50 cents). The post mining boom adjustment is far from over with the real trade-weighted index far too high for Australia to compete in anything other than dirt:

But, there will come a time when the trade will turn and money be brought home (or at least be hedged). Deutsche gives us a glimpse of when that might be:

We use recent analysis by the Fed Board staff to calibrate the Fed’s reaction function to a recession in the next several years. This work considered how the Fed would respond to a severe recession, similar in magnitude to the financial crisis with the unemployment gap rising 5 percentage points, and with the fed funds rate already at 3%. Using the Fed’s model of the US economy, FRB/US, this work concluded that the fed funds rate should be cut significantly below zero to provide enough accommodation to the economy in response to the recession. With the actual fed funds rate constrained by the zero lower bound, the paper finds that the Fed could provide similar accommodation by a combination of another QE program and strong forward guidance about the future path of the fed funds rate. The size of the required QE package is significant: $2tn.

In some ways this scenario seems too pessimistic. The magnitude of the downturn considered is likely to be more severe than the next recession for several reasons: (1) they consider a recession in line with the financial crisis, (2) there is limited evidence of substantial imbalances or overheating in the economy which should limit the depth of the next recession, and (3) monetary policy is still accommodative. Instead, a milder recession appears more likely. Conversely, it may be optimistic to assume that the fed funds rate is able to reach 3% before the next recession occurs, suggesting that the Fed could have less scope to ease monetary policy by cutting rates and therefore may have to resort to a larger QE program.

We consider an alternative scenario in which the economy enters a more mild recession in 2020 as the Fed has raised the fed funds rate to just above 3%. We assume that the recession causes the unemployment rate to rise 2.5 percentage points.

Using the results from the Fed staff’s work, and assuming that there results can be extended linearly, a recession that is half as severe would require the Fed to undertake a $1tn QE program in 2020. We assume that this occurs through Treasury security purchases, with the maturity distribution of these purchases consistent with QE3. Finally, in this scenario the Fed reinvests the proceeds from its maturing MBS securities in 2020 and 2021, but does not increase its holdings.

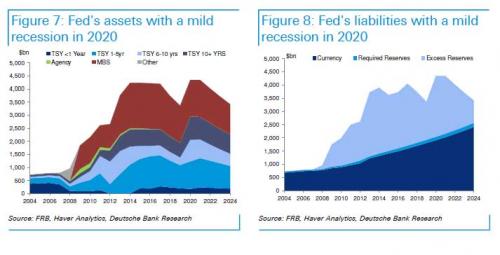

Securities are allowed to naturally roll off beginning in 2022. In this scenario, the size of the Fed’s portfolio rises above $4tn, near its record high, and it does not normalize by the end of 2024, which is the end of our horizon (Figures 7 and 8). Excess reserves remain elevated at around $800bn at that time, suggesting that it could take another three to four years – or about a decade from now – for the Fed’s balance sheet to normalize under this scenario.

That would do it! For now allocations remain:

- buy dips in the USD and S&P500;

- sell rallies in AUD and commodities;

- buy dips in short end Aussie bonds;

- buy dips in gold miners for portfolio insurance;

- sell property!