Add a third huge bubble city to your Aussie bank risk list

CoreLogic has released its latest New Zealand Property Market & Economic Update, which paints a disturbing picture of Auckland’s housing market.

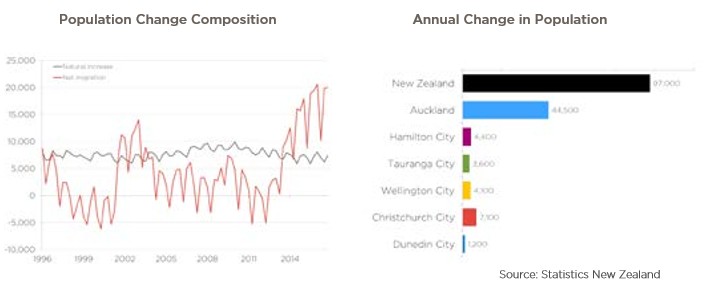

First, population growth into Auckland has been extreme – driven by immigration – with the city’s population growing by 44,500 over the past year, accounting for nearly half of New Zealand’s total population growth of 97,000:

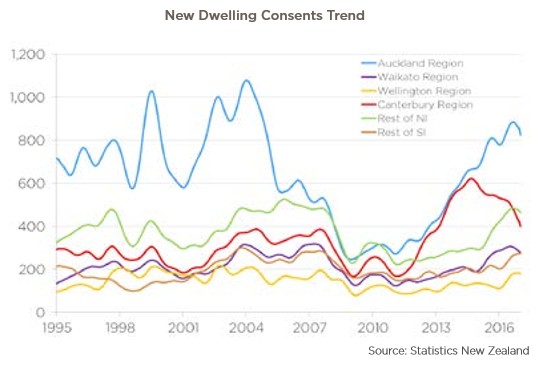

At the same time as Auckland’s population is surging, dwelling consents remain weak:

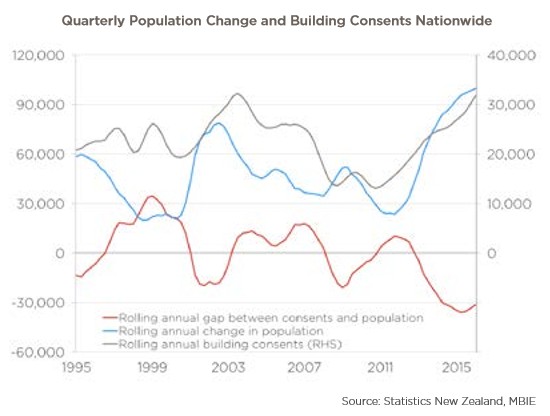

Which has led to a worsening shortage of homes across New Zealand, concentrated in Auckland:

According to CoreLogic:

Statistics NZ’s trend series for building consents showed a dramatic turnaround when January’s figures were released. December’s figures have been adjusted down and almost all areas are now trending downwards, with Auckland’s drop of particular interest.

This continues to raise serious concerns about whether the rate of building in Auckland is progressing as quickly as it needs to…

In order to build enough houses in Auckland to meet current and future demand, the level of current activity needs to increase then hold for several years.

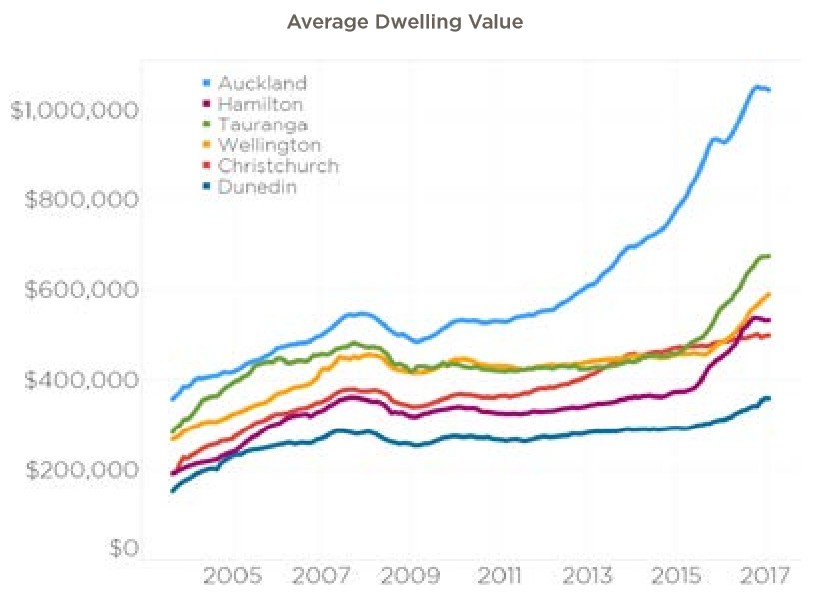

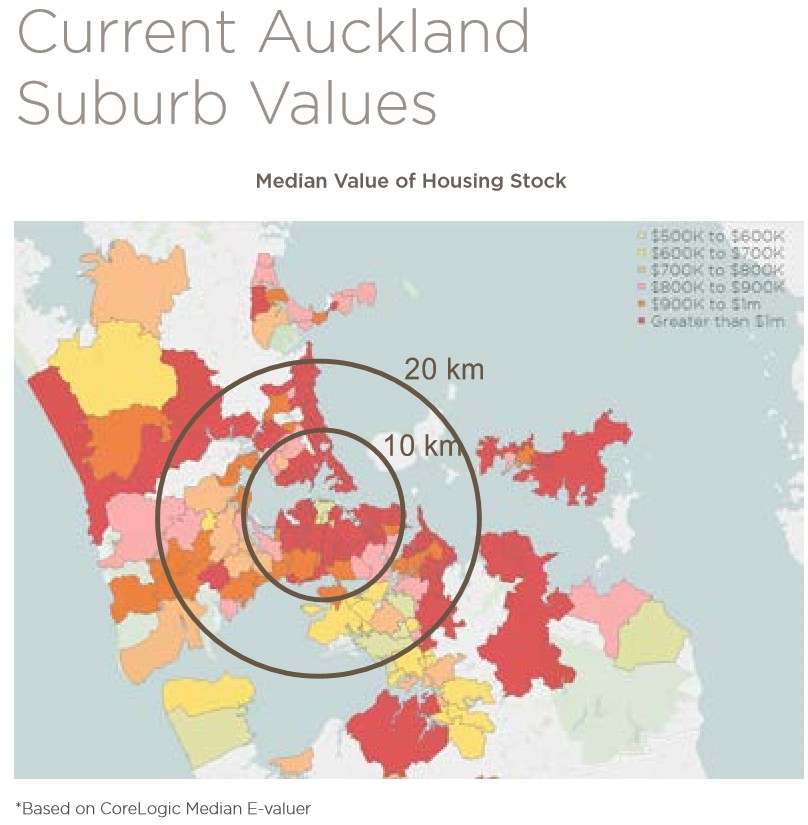

Next, we can see that Auckland’s median dwelling value was an extraordinary $1,043,680 as at end-February 2017:

And there are now precisely 100 suburbs across Auckland where the average value of the housing stock is over $1 million:

Yet, despite the exorbitant cost, investor participation in the Auckland housing market is at a record high 44%, whereas first home buyers have crashed to 19%:

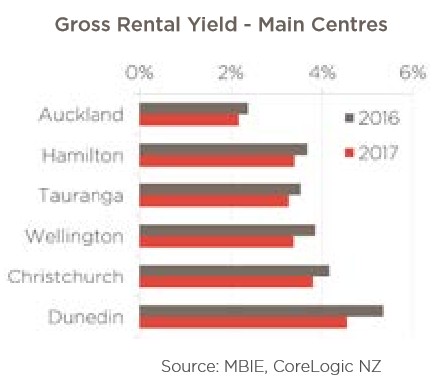

And this record investor participation comes despite Auckland rental yields crashing to just over 2% – meaning new investors are incurring big rental losses in the hope of cashing in on future capital gains:

In short, Auckland’s housing market is an immigration and investor-led bubble like few others.

unconventionaleconomist@hotmail.com