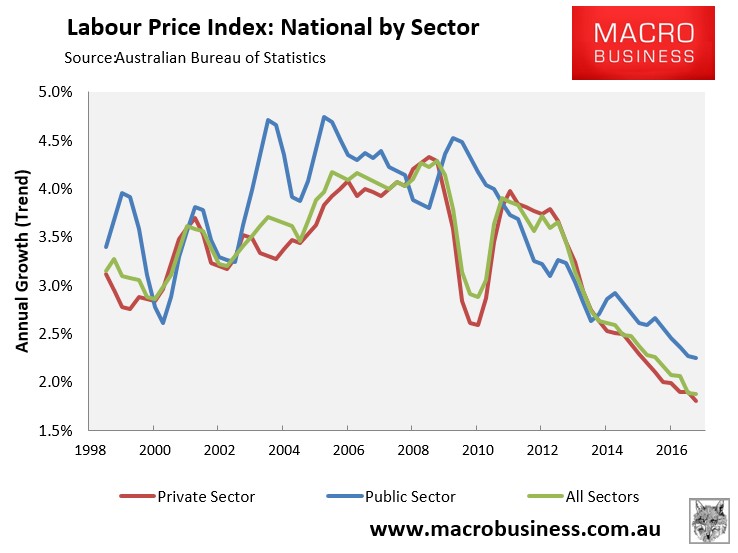

As covered today by Leith here and here today’s ABS release confirms what most of us suspect, that wage growth in the long term is looking pretty bleak. I won’t cross swords with the other fellas here on mega mortgage repayments and employments prospects but I thought I could chime in with some planning considerations.

Typically in the formation of long-run financial projections, the advice industry will use (in my experience) a figure of around 4% for projected wage growth, along with similar (or less) for expected inflation. Largely it has been accepted as a reasonable figure, in fact historically, you could call it pretty conservative!

We will leave inflation for another time, and concentrate on a potential ramification of over-egging wage growth when it comes to your financial plan.

A major concern relates to the projection of super contributions – A -2% annual variance in what you get paid may not feel like a lot at the check out, but has the ability to seriously throw out long run (when I say long run I mean 20 years, much more than that is pretty unreliable) projections. Over this period of time, expect to have contributed over 18% less than you thought you might have. On a starting portfolio of $100k at 5% growth this means a $56k black hole at year 20. Not sheep stations, but perhaps worth a rejig given that barring an Australia wide economic boom of some description, wage increases look to be lower for longer.

So what to do about this?

- Get out the spreadsheet / ring up your adviser and double check you haven’t assumed your income will double in 19 years (unless you are quite certain!) – winding down wage increases means you are either being realistic, or setting yourself up for a pleasant surprise down the track. In comparison to the alternative, this is smarter.

- Perhaps consider bumping up your concessional contributions (salary sacrifice) a touch. My back of the envelope calcs reveal that about 1.8% should cover a 2% income growth deficit over 20 years. For most people, you can get the proverbial cake and eat it too situation with both a lower annual income tax position, and confidence you are keeping yourself on track, regardless of what the future throws at you.

- Have a chat to Mr. Sukkar about a higher paying job.

Tim Fuller is Head of Operations at the MB Fund launching in May 2017. Register your interest now (if you haven’t already):