Mainstream media is in a panic about Donald Trump. Financial markets are pretty calm. So, what would it take to spook financial markets?

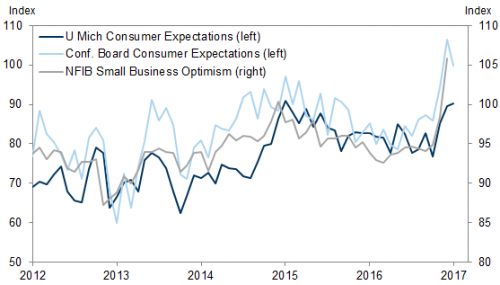

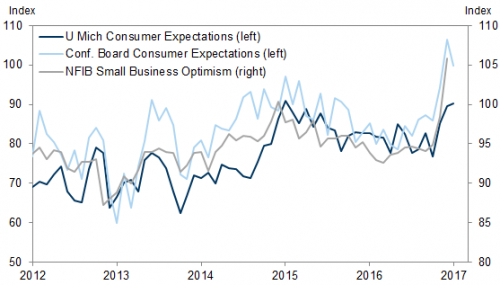

US consumers / US small business owners are the key

My take is that the small business sector is the key driver of US employment, the US consumer is the key driver of demand. When sentiment leaves those sectors it’s time to panic.

I wish that the average American small business owner was more worldly and understood that if you abandon (or even threaten to abandon) NATO allies then you lose trust for decades. And your other allies begin to doubt your sincerity. But the average American small business owner doesn’t care.

I wish the average American consumer understood that you can’t convince totalitarian regimes to improve human rights when your own country is breaking the Geneva convention by torturing people. And even the US military says that torture doesn’t work. But the average American consumer doesn’t understand – torture has close to a 100% success rate on TV so surely it works in real life.

In Australia and the liberal press in the US, Trump insulting “Trunbull” was an outrage. In other news, the American in the street doesn’t care – they figure that Trump is in a Twitter war with Arnold Swartzenegger on a weekly basis, so what does it matter if Trump also insults the leader of the country that Arnie is from?

Building a wall with Mexico? It’s a border. Borders are meant to have something to stop people crossing.

Sudan/Iran/Iraq visa bans? All “bad guys”. Except for those that are playing in the NBA for a local team – better make sure that they can still play.

Withdrawing funding from foreign charities who help with abortion? Someone else’s problem.

I have been looking to Fox News for perspective. While Australian newspapers led with half a dozen Trump catastrophes, Fox News was highlighting the increase in morale for US Border guards. Most Americans really don’t care what happens outside of America.

Don’t let politics cloud your investment judgement

From an investment perspective, don’t let politics run your portfolio. Japan from 1970 to 1990 coupled one of the largest economic booms in history with one of the world’s most xenophobic immigration policies. China’s own economic boom has been tightly bound with a regime that allows few civil liberties for ordinary citizens, and even less dissent.

Trump’s policies are socially divisive and will set back human rights, international diplomacy and global warming by a decade or more. Unfortunately (for society), these policies don’t affect the average Fox News watching small business owner, or the average US consumer in the short term.

Trade wars and real wars will. But, economically Trump looks like he is going to run up the credit card bill to create a debt-fueled boom. Yes, the boom will likely end badly for reasons I went into detail last month. But there are very few occasions where it works to sell before the boom even starts.

Timing

Goldman has useful take on how the Trump reform agenda will unfold:

Q: What does all of this mean for tax reform?

In our view, the last few weeks demonstrate that tax reform will take a while to enact and will probably be scaled back relative to what House Republicans and President Trump have proposed. As with many other policy issues, much hinges on the Senate. The ongoing debate over Obamacare demonstrates how difficult finding a consensus among 51 Republicans can be when there are only 52 Republican senators. Near-unanimous decisions are generally hard to reach and without bipartisan support congressional Republicans are apt to proceed more carefully since they are likely to be held accountable for the results.

The two biggest questions in tax reform are whether to include a “border adjusted” corporate tax in the proposal, which raises enough revenue to allow for 10pp reduction in the tax rate but could also result in potentially substantial unintended consequences such as price inflation of imported goods, and whether the legislation should be revenue neutral or whether it should result in a net reduction in tax liabilities. As discussed below, we assume that border adjustment will not ultimately be adopted, and that tax reform will increase the deficit by slightly less than 1% of GDP.

Q: What’s the latest on border adjustment?

We recently lowered to 20% our subjective probability that a border-adjusted corporate tax similar to the House Republican Blueprint will become law. This was mainly due to recent comments from President Trump expressing a mixed view on the proposal. That said, there continue to be what we view as good arguments for and against its eventual enactment.

We expect the proposal to continue to enjoy support in the House, since it raises a substantial amount of tax revenue—over $100bn per year, enough to finance a roughly 10pp reduction in the statutory corporate tax rate—without, in theory, reducing the long-run after-tax profitability of any industry, if the value of the dollar ultimately rises to reflect the effect of the import tax and export subsidy. It could also potentially achieve a number of long-sought goals of corporate tax reform, particularly allowing for a territorial tax system without incentivizing offshoring or imposing cumbersome protections against profit shifting. From a political perspective, some proponents of the plan also emphasize its appeal as part of an “America First” theme, suggesting that it could offset the alleged advantage that border-adjusted value-added taxes in other countries provide their domestic industries. While the last argument is unlikely true if exchange rates adjust to these tax systems, it nevertheless increases its political appeal in some quarters.

However, there are stronger reasons in our view to believe that border adjustment will ultimately be excluded from this year’s tax legislation. In the House, some Republican lawmakers appear to have misgivings. This may not be that relevant in the near term, since House Republican leaders are likely to ensure that it remains in the initial version we expect to be introduced around May, and most House members will not get an opportunity to vote to change the bill, only to approve or reject the bill in whatever state it reaches the House floor. We would not expect enough House Republicans to object strongly enough to the border adjustment provision in particular that they would vote against the Republican tax reform bill as a whole.

However, these concerns could become much more important in the Senate, which differs from the House in three important respects. First, the margin in the Senate is much smaller, since Republican leaders there can afford to lose only 2 Republican votes assuming that no Democrats support the tax legislation and Vice President Pence casts a tiebreaking vote. Second, dozens if not hundreds of amendments are likely to be considered to the Senate’s tax reform legislation, both in the Senate Finance Committee and on the Senate floor, unlike in the House, where few members will have an opportunity to change the bill. This means that each Senator’s view on border adjustment is relevant. Third, while House Speaker Paul Ryan and Ways and Means Committee Chairman Kevin Brady appear to be strongly behind the border adjustment effort in the House bill, there does not appear to be an equivalent driving force in the Senate; in fact, Senate Finance Committee Chairman Orrin Hatch and Senate Majority Whip John Cornyn, among several other influential Republicans, have made comments suggesting they have reservations regarding the proposal.

Q: If Congress does not enact border adjustment, what does that mean for tax reform?

Without border adjustment, reducing the corporate tax rate to 20% or 15% will be very difficult. We noted previously that Senate Republicans appear less enthusiastic about border adjustment than House Republicans. This would leave them with three potential options:

- Increase the deficit: President Trump’s proposal would lower the corporate rate without significant offsets, expanding the deficit instead. While one can imagine the political appeal of simply lowering the rates without raising taxes in other areas, we expect that it will be quite difficult to reach 51 votes in the Senate for tax legislation that is not roughly “revenue neutral” as defined by congressional Republicans (see below). There could be concerns among fiscal conservatives in the House as well, though that appears less likely to us to be the binding constraint.

- Base broadening: While traditional base broadening such as the limitation or elimination of various tax preferences has been less of a focus in the current debate—the House pays for most of its proposal with border adjustment, and President Trump’s plan does not raise much offsetting corporate tax revenue—various other tax reform proposals over the years have primarily relied on such changes to finance lower rates. There is a limit to how far this can go; former Ways and Means Chairman Camp’s comprehensive reform bill released in 2014 went as far as politically possible, in our view, and achieved a 7pp reduction in the statutory rate.

- Scale back the tax cut: Lawmakers might ultimately decide to scale back the size of the statutory rate reduction to avoid the first and second options.

While the situation is fluid, our expectation is that Congress will ultimately enact a meaningful reduction in the statutory corporate tax rate, potentially down to 25%, but not to 20% or 15%. This could be financed with limited base broadening, the proceeds from profit repatriation, and a redefinition “revenue neutral” as follows:

- Dynamic scoring is likely to be estimated to generate at least a few and potentially several hundred billion dollars over ten years in revenue, enough to finance perhaps a 5pp reduction in the statutory corporate rate.

- Technical factors could provide a few hundred billion of additional room for tax cuts, potentially financing another 3pp or 4pp of corporate rate reduction. The main issue in play here is the use of a “current policy” baseline, which assumes that temporary provisions will be extended rather than the traditional method of estimating against a “current law” baseline that assumes tax receipts increase when tax incentives expire.

- Deemed profit repatriation is likely to provide sufficient revenue for another 1pp of rate reduction.

- Base broadening measures, like incremental reductions in various corporate tax preferences, might provide sufficient revenue for another 1-2pp of rate reduction

Taken together this would provide sufficient room for a reduction in tax rates for around 10pp of rate reduction, or from 35% to 25%. While the rate could be slightly higher or lower, the range of possible outcomes does not seem very wide; without border adjustment, going much lower than 25% would require more base broadening or deficit expansion than we expect could pass the Senate; going much higher than 25% would result in a rate that is still among the highest in the OECD and we suspect some lawmakers might simply decide that, absent larger changes, tax reform is not worth the trouble.

Q: What ever happened to the infrastructure program?

President Trump proposed during the campaign to generate $1 trillion in new infrastructure investment, but unlike other policy areas where the President has already taken executive action, infrastructure has gotten relatively little attention, for two reasons in our view. First, infrastructure is mainly a financing issue, and spending and tax changes must go through Congress. Second, while congressional Republicans are very focused on tax reform and Obamacare repeal, infrastructure appears to be a lower priority. Congressional Democrats are quite supportive of infrastructure spending, but have shown much less interest in tax incentives aimed at public-private partnerships, as the White House seems to envision.

Our expectation continues to be that a modest infrastructure package will be enacted—we have penciled in a figure of $25 billion per year—and that it is likely to consist mainly if not entirely of tax incentives. If so, the most likely avenue for enactment will be to include it in tax reform legislation, which we expect to pass late this year or in early 2018.

Q: What happens next?

The next major milestone will be the President’s State of the Union Address, scheduled for February 28. This is likely to be followed by the President’s submission of a preliminary budget to Congress sometime in March. We are unsure of what to expect out of the budget next month but, in light of the fact that the nominee for Director of the White House Office of Management and Budget (OMB) awaits confirmation along with several other Administration officials, we expect that the forthcoming budget will probably include minimal detail.

Around this same time, in late March or April, we expect the budget resolution for the coming fiscal year (FY 2018) to be released, though the timing could be delayed if Republican lawmakers are still trying to resolve the Obamacare issue. This will be an important event for two reasons. First, it will demonstrate how congressional Republicans propose to simultaneously eliminate the budget deficit by 2027 (the end of the 10-year budget window Congress uses), cut taxes meaningfully—the Tax Policy Center estimates that the House plan would reduce tax receipts by around $3 trillion over ten years—while preserving Medicare and Social Security spending, which President Trump indicated during the campaign he did not want to cut, and increase defense spending. By contrast, the most recent House-passed budget resolution proposed spending cuts of around $6 trillion (13%) over ten years to reach balance by the end of that period, with half of the savings coming from Medicare savings and the repeal of Obamacare benefits, no reduction in tax revenues, and a modest increase in defense spending. We expect that congressional Republicans will ultimately reach an agreement and pass a budget resolution because it is a necessary step to pass tax reform legislation later this year, but the process is likely to demonstrate the limits of how much fiscal stimulus is possible given other constraints.

Once the FY 2018 budget resolution has been approved by both chambers, the House Ways and Means Committee is likely to move forward on tax reform legislation. This is unlikely to occur before May. At this point, we expect to see the first concrete policy details of tax reform in the House and, as noted earlier, we expect that border adjustment will continue to be in the House proposal at this stage. House passage looks likely by July. The Senate is likely to be on a slower track; the Senate Finance Committee may not produce legislation until the second half of the year, potentially responding to the House product with a proposal of its own. Assuming substantial differences with the House on issues like border adjustment, the two chambers will probably resolve differences in a conference committee, which will agree on one final version subject to a single final vote between the two chambers, though other methods are possible. In Exhibit 3, we show this final step as occurring sometime between October and December, but there is a fair chance that final enactment of tax legislation could slip into early 2018.

Growth vs Valuation

From a growth perspective, it looks like there has been a wholesale increase in sentiment in the US:

This will probably increase economic activity enough to tide the US economy over until the tax cuts actually kick in, so there is probably 18-24 months of growth to run.

The US forward P/E is 17.3x. Which is expensive, but add 10% EPS growth from tax cuts (see post from last month) and it looks cheaper. Regardless, we need to be selective about what we purchase – avoiding companies that will suffer from a high USD is important.

Don’t forget the risks

A major trade war remains the key risk. I’m sticking with the view that Trump’s diplomacy is the Art of the Deal: take an extreme position (check), create the appearance of unpredictability (check), then negotiate back to a reasonable position.

If we don’t progress to stage 3 then we have a problem.

The other risk is that the tax cuts don’t get put through in the expected size. This remains a risk to monitor.

The round-up

US small businesses are the key to employment. US consumers are the key to demand. That is where I’m watching for signs of panic, not the headlines.

Damien Klassen is Chief Investment Officer at the MB Fund launching in April 2017. Register your interest now (if you haven’t already):