There are a number of elements to Trump’s tax plan. Most of it involves cutting taxes on the richest and hoping that “trickle down” will sort everything out. I don’t think there will be a happy ending to that story.

However, the tax plan is more complicated than that, especially at the corporate level – there are actually some changes that have merit. There are extensive modifications to corporate incentives. There are also some changes that could spark a global trade war. Hence, there is a spectrum of possible outcomes, to put it mildly.

There are three things I’m interested in when looking at the changes from the investor’s perspective:

- The net fiscal impact

- The effect on the US economy from the change in tax structure

- The effect on individual companies from the change in structure and rates.

I have dealt with the first impact before and will undoubtedly do so again – but this post is more about the second two issues.

The Short Version

Before you read too much further, two quick disclaimers: (1) this is based on a mix of the Ryan’s & Trump’s proposals from last year, and are far from certain; (2) this is a more technical post that is probably not for everyone. If you don’t care about the detail, the messages you can take away are:

- The tax cut (35% to 15%) is not as significant as it looks due to other changes. In particular for companies with large debts or offshore production. But it is still a big cut for most companies, and will probably boost aggregate earnings by 10-15% over the first few years.

- It is likely that the corporate tax plan would bring forward company investment. One more reason to expect a boom in the short term.

- Debt funding will be less attractive for manufacturers. And potentially for most companies.

- Some of the changes are questionable under the World Trade Organization and might spark a trade war.

- Count the US investment banks as winners; there are lots of corporate structures that will need changing and lots of fees to do so.

- US exporters are also winners, but only if a rise in the USD doesn’t negate the benefits.

What are the proposals?

For companies, I’m looking at five key changes:

- Lower tax rate. Headline rate cut from 35% to 15%.

- A one-time repatriation of corporate cash held overseas.

- Immediate write-off of capex. Trump has suggested limiting this to manufacturers, Ryan’s plan is for all companies.

- Interest deductibility. This is tied to the capex write-off (and applies to the same companies) – no more interest deductibility for tax.

- Border tax. This is the most contentious and could spark a trade war. Removes tax deductibility of import costs.

Lower tax rate

The plan is simple, cut the headline rate from 35% to 15%. The actual effects are more complicated due to a range of other changes. Estimates vary, but it would seem that in aggregate corporate taxes collected by the US government will fall by 25-40%.

I suspect for the average company it will be at the lower end of the scale at the start, i.e. taxes down around 25-30%. As companies work out the most efficient ways to structure operations, there are likely to be more tax gains.

Putting that into earnings growth terms, if a hypothetical company was making $100 and paying $35 in tax = $65 in after-tax earnings. If this turns into $25 in tax and $75 in after-tax earnings that means a 15% increase in after-tax earnings.

Complicating that is that many listed companies already have foreign earnings which will reduce the overall impact. So, I’m thinking that in aggregate corporate earnings have a one off 10-12% increase, followed by a few years of earnings growth being ~1% higher than they would have otherwise been.

Maybe other countries also cut corporate taxes (its a race to the bottom!), and so earnings growth could easily be better than my estimate.

One more reason for a boom (and then a bust).

A one-time repatriation of corporate cash held overseas

The detail behind this is a bit of a long story, which I won’t go into. The net effect is that it has been advantageous for US companies to leave money in foreign subsidiaries so that they don’t have to pay tax. The most famous is Apple with over USD200b in cash and bonds. i.e. Apple has more cash than the market capitalisation of the largest company on the ASX.

Trump’s plan is to give companies a one-off chance to repatriate this money at a significantly discounted 10% tax rate.

I’m assuming that a lot of them will take the opportunity.

Whether the companies invest the money in the US or give it back to shareholders, it is likely to be a positive for the US economy.

One more reason for a boom (and then a bust).

Interest deductibility

Note: Trump has suggested limiting these to manufacturing companies but has not ruled out implementing it more widely. Paul Ryan (Republican leader of the House of Reps) has proposed applying it to all companies.

Currently, it is more tax effective to use debt rather than equity. Companies are allowed to deduct interest before paying tax, but under Trump’s plan, the benefit will be removed and equal treatment for debt and equity.

This is an interesting change that has a number of benefits and will probably lead to more equity funding and less debt funding over time. The benefit is that it would make the system less vulnerable to external shocks. There are complications in the changes in personal taxation that make the effects not that simple, but overall the plan is good for companies without much debt, bad for companies with lots of debt.

Other countries will probably lose out. Multinationals will be busy playing tax games trying to shift the debt to other countries (e.g., Europe, Japan, Australia) where debt is deductible and out of the US where debt isn’t. This will probably lower government revenues in those countries. Those countries will also see an increase corporate debt, potentially increasing the risk in their banking systems.

Currently, it is not clear how the changes will affect banks regarding tax. What is clear is that it is a negative for corporate lending growth – there will be less incentive for companies to take on debt rather than equity. There are also some accounting changes (bringing operating leases onto the balance sheet) coming in over the next few years that will have the same effect.

It is also likely to be a negative for bad debts in the short term. This is because any company that is currently struggling to make interest payments will lose any tax shield, making it harder to pay loans. I suspect that the “boom” factors from other elements of the tax changes will keep bad debts relatively low in aggregate, but there is likely to be some individual over-geared companies who go broke without a tax shield from debt.

If extended to all companies, this plan is particularly important for a range of “safe”, highly geared companies, although complicated by the tax structure of the companies. Utilities, REITs and infrastructure companies who have been using a trust structure are likely to be less affected than those who haven’t.

So, extra care needed when choosing US stocks over the next year – gearing and corporate structure more important than usual. Clearest winner to me are the US investment banks… someone is going to need to charge fees to change the debt/equity structures for multinationals.

Investment exclusion

Tied to the interest deductibility change.

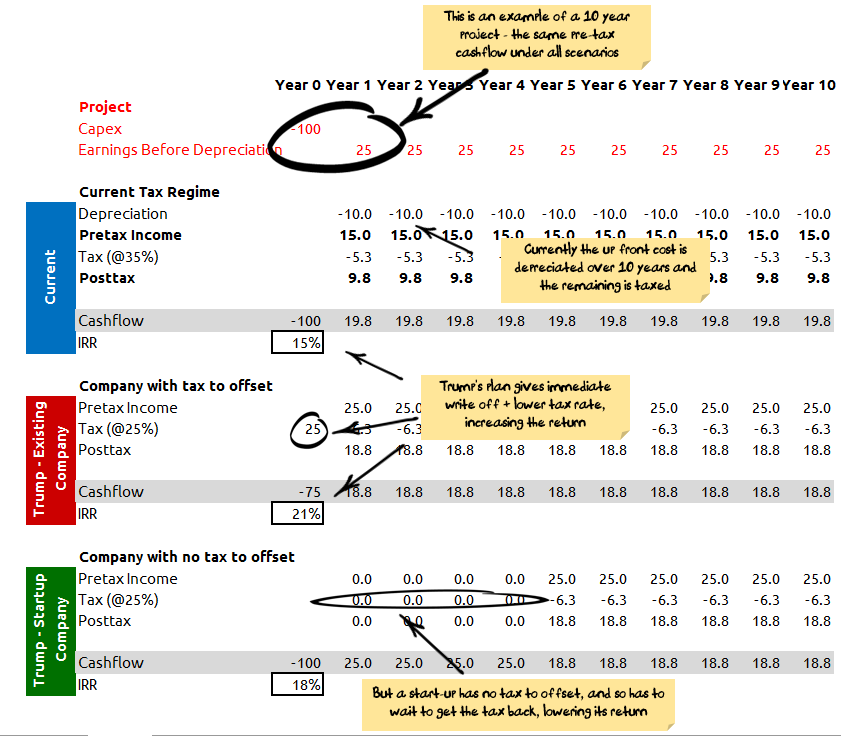

The proposal is to get rid of depreciation, converting the corporation tax from a tax on profit to a tax on cash flow. So, you get an immediate deduction for any capex.

This favours investment in long-lived assets. Which is a good thing for society. I’m a little less confident with individual companies making 20-year investments when the median CEO tenure is around six years, but let’s call it a positive for investors.

On the flip side, it favours existing companies over start-ups which might be a bad thing for the economy over time, but a benefit to any existing companies – see the table below for a worked example.

Net effect is that there is a greater incentive for companies to invest and bring forward projects (especially if companies think the tax laws will be transient).

In the long term, if investment returns are higher, then investment/competition will increase until returns are lower. So, it is probably more of a “bring forward” of investment rather than a permanent increase. In the long term, there are probably fewer start-ups under this scenario, especially coupled with the changes to interest deductibility.

The biggest winners? Probably large energy & mining companies. They get lower taxes, and if the interest deductibility gets extended to all companies then smaller resources companies will both struggle to raise debt, and won’t be able to get the same returns (see table above).

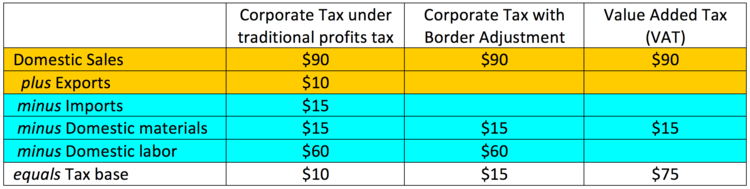

Border adjustment

This is the most contentious change. It changes the tax rules so that import costs are also no longer a tax deduction and export revenue is not longer taxed.

A good illustration, comparing it to a Value Added Tax (Australian GST is considered a Value Added Tax) is below:

Source: Stephen G. Cecchetti and Kermit L. Schoenholtz, Money & Banking

It clearly makes production in the US more tax advantageous than offshoring.

It may or may not be legal under World Trade Organization rules. If legal, it flouts the intent of World Trade Organization rules, and so there are probably retaliatory tax changes in the offing.

A short term gain for the US employment market and US government revenues is likely. Over the longer term world trade is a good thing for all of the countries involved, and so this is liable to be a bad thing for the US through lower productivity.

There are lots of individual companies affected, outsourced production in Asia (semiconductors in particular) are probably the biggest losers. The biggest winners are US exporters, to the extent that the US dollar doesn’t increase and take away all of the benefits.

Damien Klassen is Chief Investment Officer at the MB Fund launching in April 2017. Register your interest now if you haven’t already.