For close to 15 years, Residex has reported house and unit price growth using a combination of repeat sales technology, hedonic technology and median/stratified median index technology. Residex’s founder, John Edwards, explained this methodology way back in February 2012:

It is some ten years or thereabout since Residex published a pure repeat sales index. The Residex Index is non-revisionary unlike all other indexes and is released much earlier than all others [not any more since CoreLogic began its daily index]…

So what is the Residex Index which we publish?

It is an index calculation developed by Residex over the last 20 plus years where we use the best of the Repeat Sales Index technology, the best of the Hedonic technology and Median/Stratified Median index technology. The result unlike all others is that we use all data available and discard nothing in the development of the index number.

The Residex Australian Property Index Methodology website page also dedicates significant space espousing the virtues of its methodology:

Residex Australian Property Indices cover the full market

Residex indices consider all properties in a market to determine market movements — recently sold (median price index), established and previously sold properties (repeat sales index) and properties with detailed attribute data (hedonic index). This is vital in preventing skewed results that could overshoot or undershoot true market movements and values. Without full market coverage, you’re not getting the full picture.

Residex Australian Property Indices are accurate

Housing markets have a natural “true” volatility as markets do not grow at the exact same rate from month to month. However, true volatility is often swamped by “index calculation volatility” — the volatility introduced solely by the methodology used to generate the house price index. Residex has undertaken research that measures the amount of true volatility in a market and the amount of index calculation volatility that is caused by using a variety of different index calculation methods. The Residex Australian Property Index has been constructed in such a way that the volatility caused by the index calculation method is removed, leaving an accurate and true representation of the underlying market movements…

Residex Australian Property Indices are non-revisionary

There is no revision of Residex’s calculations of market growth. Some other indices (most notably the repeat sales index) require constant revision due to the calculation method. While in most cases the revision is relatively minor, it is preferable to use an index that gets it right first time.

Residex Australian Property Indices are long-term

Residex indices go back to the 1970s for the large Australian states. Capital city data goes back as far as 1975.

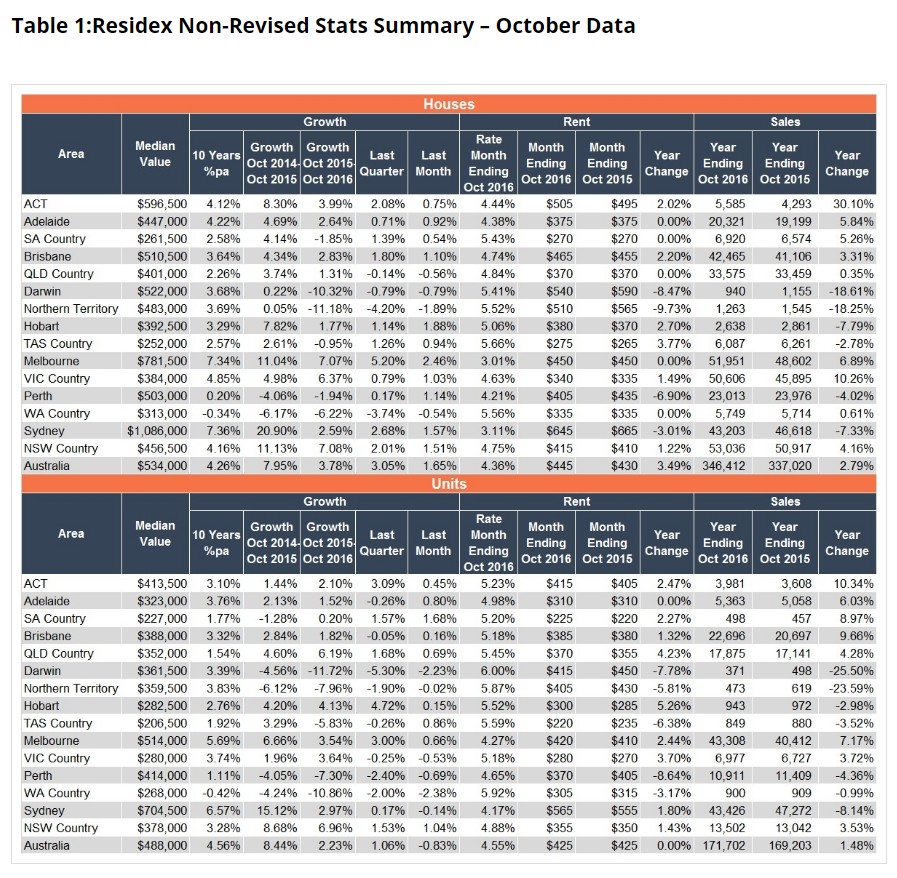

Up until November 2016, Residex’s index results were reported based on the methodology explained above. For example, below is the results table for October 2016 (reported in November):

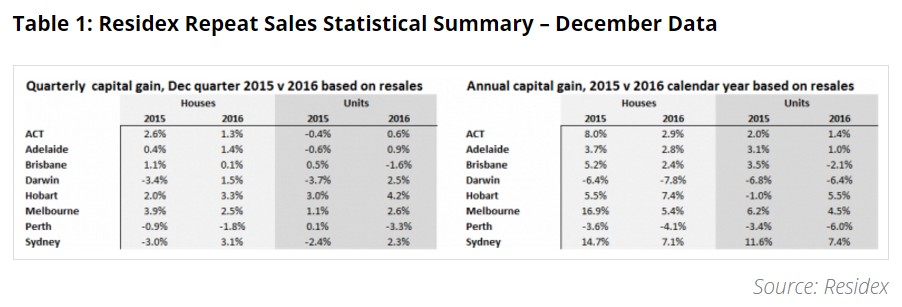

Over the weekend, CoreLogic (the new owner of Residex) released its December results, which not only changed the format and detail of how it reports value changes, but also shifted the methodology from the non-revisionary one explained above to a revisionary repeat sales methodology:

As explained by CoreLogic’s Tim Lawless:

The Residex repeat sales index provides a unique perspective on the housing market, considering the resales methodology is very different to other housing market measurements available in the marketplace, which are typically price based (simple median prices and stratified median prices) or quality adjusted value based measures (hedonic regression index). In simple terms, the Residex repeat sales method examines sale pairs (ie where a property has sold at least twice, the most recent sale price is compared with the previous sale price to measure the extent of capital gain or loss). Inherently, a resale method of measuring housing makret conditions excludes the effect of newly developed properties because they don’t have a previous sale price to compare with. The methodology also excludes those properties that have seen a change in their attributes over time, which controls for the effects of obvious capital works on the property.

Based on the December quarter data, property transactions with a sales pair accounted for approximately 70% of all house sales across the capital cites and 63% of all unit sales. The remaining transactions were either properties that sold for the first time over the quarter (ie new to market) or there were changes to the property attributes such as additional bedrooms or bathrooms or a change to the land area.

Importantly, the Residex repeat sales index is revisionary. As more data flows through, more sale pairs are identifed which may result in some upwards and downwards revisions to the indices.

I pose the following question to CoreLogic: Why has it changed the way that it reports Residex’s figures from a non-revised, comprehensive methodology to a simpler (presumably inferior), revisionary repeat sales methodology that does not capture large chunks of the market?

As a long-time user of Residex’s index, I find this change in methodology incredibly frustrating since I am no longer comparing ‘apples with apples’. This methodological change has also added yet more confusion after CoreLogic abruptly changed its hedonic daily index methodology in April 2016 without explanation and without publishing the backwardly revised data set.

We kindly request that CoreLogic publish the old Residex index methodology for the December quarter of 2016 (as well as going forward) so that industry participants and commentators can make valid comparisons.

The last thing the nation needs is a more confused and less informed housing market.