Yesterday, Houses & Holes penned an open challenge to CoreLogic to “publish as soon as possible an updated chart that compares the changes in the price indexes since May using your new index method versus what they would look like using your old index method”.

Below is the response from Tim Lawless, Research Director – Asia-Pacific:

CoreLogic has previously explained the changes made to our hedonic home value index during April. To refresh, there has been no change to the hedonic model, the only change that was made was how the index method treats outliers. The improved trimming method has provided a higher level of precision by ensuring as many legitimate transactions are available to the model each day and illegitimate transactions are excluded. While the daily index did show volatility over April, we estimate the overall uplift was less than 1% across the combined capitals index.

We have previously outlined our plans to release a revised hedonic index, and we will be focussing our resources on building this index across the recently released ASGS 2016 geographic boundaries. As we have done in the past, the re-release of our hedonic indices will go through an internal and external peer review and audit process and method papers will be available to the public.

The recent divergence from other housing market indicators isn’t unique, there have been periods of divergence previously. Importantly, CoreLogic’s hedonic index tracks value changes across the entire portfolio of housing rather than price movements based on only those properties that are transacting. At a time when year on year transaction numbers are down by approximately 11%, the smaller transactional base and bias from segments of the market that are active or inactive is likely to be influencing price based measures.

Another consideration is how off the plan sales are treated within other methods. Inherently, a repeat sales index wont account for the effect of record levels of new stock in the market as this method relies on sales pairs. Also, growth rates in revisionary median sales indices are likely being revised as extremely lagged off the plan sales data come in (caused by higher prices with earlier contract dates). Median indices that do not revise are not including this segment, which may be an issue for those models. The hedonic model is unchanged in that it includes those sales as they arrive however control for the sale date.

CoreLogic continues to work closely with policy makers and regulators, as well as the private sector. Further, there have been no changes to our subscription base and briefings schedules. We have absolute confidence that our hedonic index readings continue to represent the most timely and accurate measure of value growth across Australia’s housing asset class.

I thank Tim Lawless for the response. We do, however, remain skeptical of the CoreLogic index. Here’s why.

Followers of the CoreLogic Index will know that it has previously reported large seasonal declines in May, as follows:

- -1.41% in May 2012

- -1.19% in May 2013

- -1.91% in May 2014

- -0.94% in May 2015

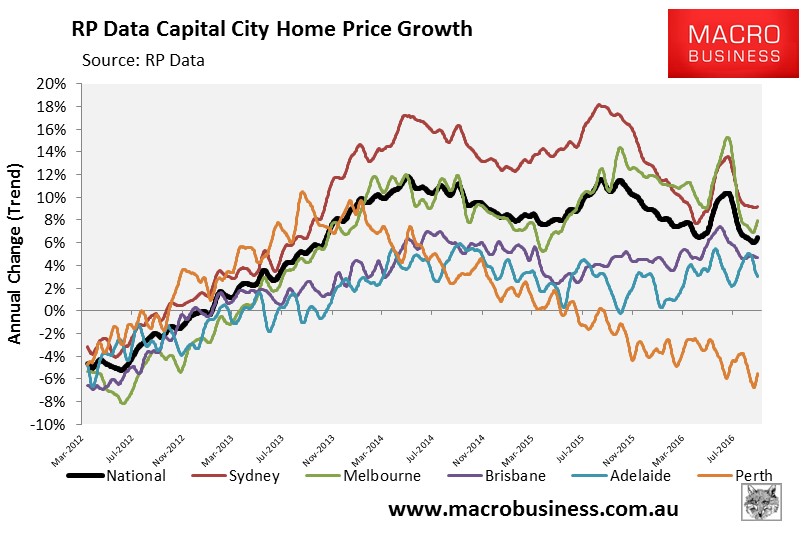

However, this year the index recorded a large 1.54% rise, following the methodology change, which sent year-on-year growth soaring from 6.6% as at the end of March 2016 (i.e. before the methodology change) to 10.7% annual growth by mid-June:

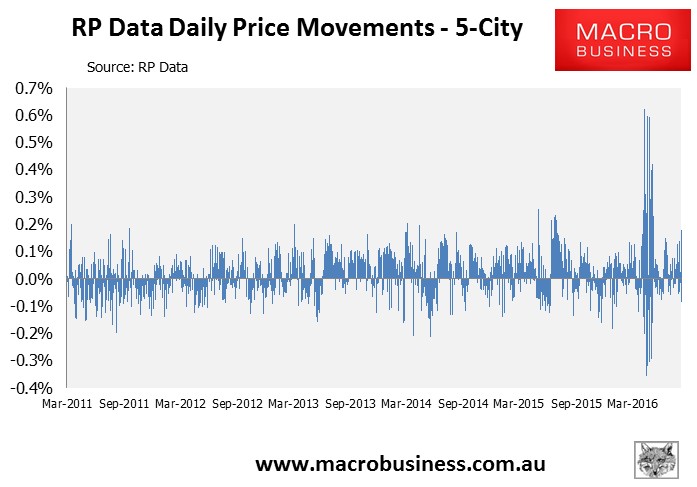

We also witnessed extreme price volatility in the daily index:

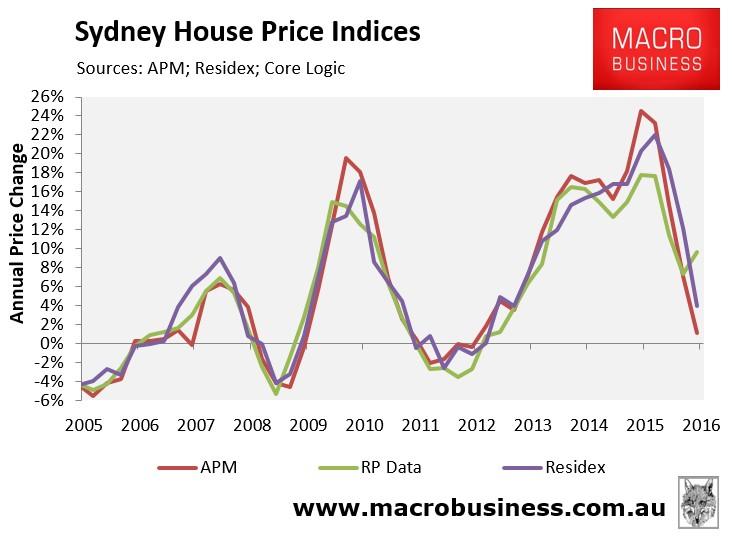

As well as a break-away from the other two private data providers:

While year-on-year growth has begun to trend downwards once more, it remains above the 31 March level of 6.6%, tracking at 7.2% as of 7 September 2016.

This seems an odd result given not just the other indices, but also the weakening fundamentals of falling housing credit, weaker transaction activity, and rising average selling times, partly offset by stronger auction clearances (albeit on much lower listings).

Ultimately, we won’t be able to gauge the full impact of the methodological change, and the true state of the market, until CoreLogic backward adjusts the daily index to its inception (in March 2011) using the new methodology.

We urge haste.