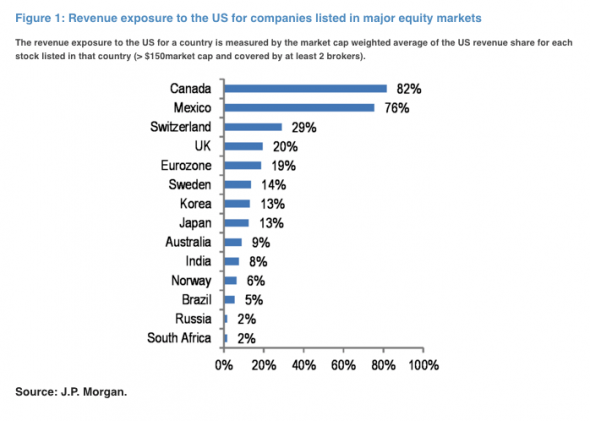

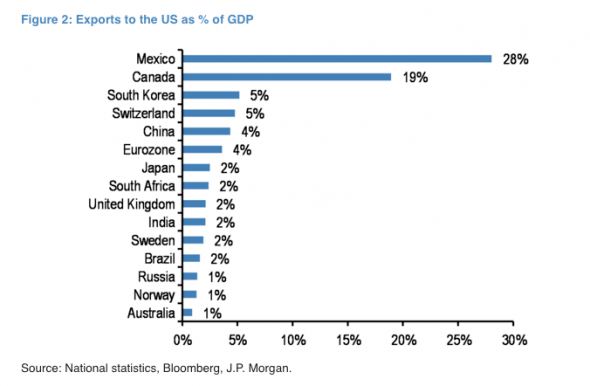

Here’s some more on border taxes from the FT, following up on my rundown yesterday on Trump’s effect on taxes. The FT are invoking JP Morgan (JPM) to show which countries and stock markets are most exposed:

JPM then go on to draw some conclusions based on ETF flows:

It is of course almost certain that investors’ positions across regions and currencies were influenced by factors other than border taxes since the US election. But the big inconsistency seen between the position shifts of [ETF inflows] vs. the border tax vulnerability rankings of Figure 1 and Figure 2 suggest that markets attach low probability of a border tax being implemented.

Conversely, given this low probability being priced in, it also suggests a prospect of more significant dislocations in the event the border tax features prominently on the agenda of the incoming Trump administration.

I’m not a huge fan of using ETF flows the way JPM have, there are any one of a dozen other issues that could explain the differences in ETF flows. However, I do agree with the conclusion that the prospect of border taxes and a global trade war is not priced in.

- From an asset allocation perspective, this is the key decision for 2017.

If there is no global trade war and a big US stimulus through lower taxes then equities look OK at current prices. If there is a trade war then equities are expensive.

I’m leaning towards no trade war, but the level of certainty is low and so I’m keeping two sets of stocks/assets handy: (1) the stocks/bonds to own during the first phase of the Trump boom; and (2) the stocks/bonds to own if a trade war begins.

Damien Klassen is Chief Investment Officer at the MB Fund launching in April 2017. Register your interest now (if you haven’t already):