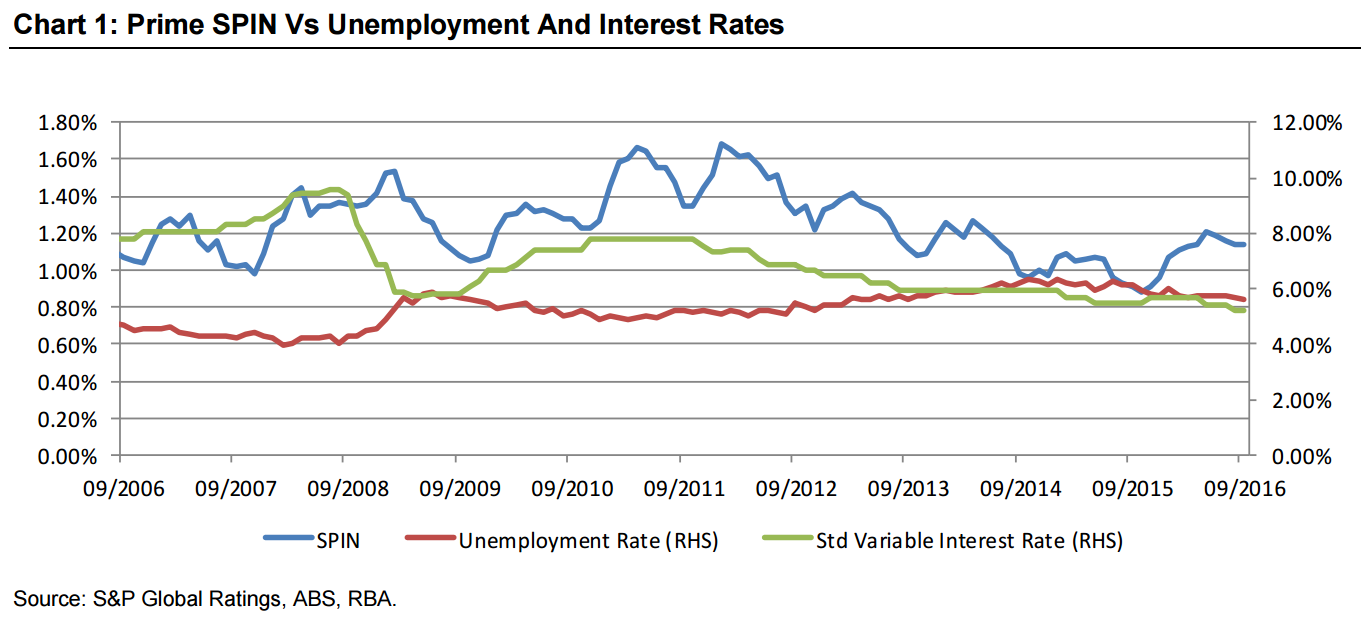

The Standard & Poor’s Performance Index (SPIN) for Australian prime mortgages was 1.14% in September, unchanged from August. It fell 4.5% during the third quarter (Q3) of 2016 from 1.19% in June. We expect arrears to fall between June and September, with Q3 normally being lowest point in the arrears cycle. However, arrears in Q3 2016 were up 25% from the same time last year–a common theme this year. Arrears at this point in the cycle have not been at this level since September 2012, when interest rates were considerably higher than they are now (chart 1). Chart 1: Prime SPIN Vs Unemployment And Interest Rates 0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 0.00% 0.20% 0.40% 0.60% 0.80% 1.00% 1.20% 1.40% 1.60% 1.80% 09/2006 09/2007 09/2008 09/2009 09/2010 09/2011 09/2012 09/2013 09/2014 09/2015 09/2016 SPIN Unemployment Rate (RHS) Std Variable Interest Rate (RHS) Source: S&P Global Ratings, ABS, RBA. Arrears on nonconforming residential mortgage-backed securities (RMBS) decreased by more than 2% during Q3, falling to 4.36% from 4.46% in Q2. While nonconforming arrears were up more than 9% year on year, they remained well below their financial crisis peak of 17.09%. While we consider arrears to be still at relatively low levels, their performance during the past 12 months suggests they have bottomed out. A frequently asked question is, “What is driving this performance when interest rates are low and unemployment relatively stable?” A closer look at employment trends sheds some more light on the issue.

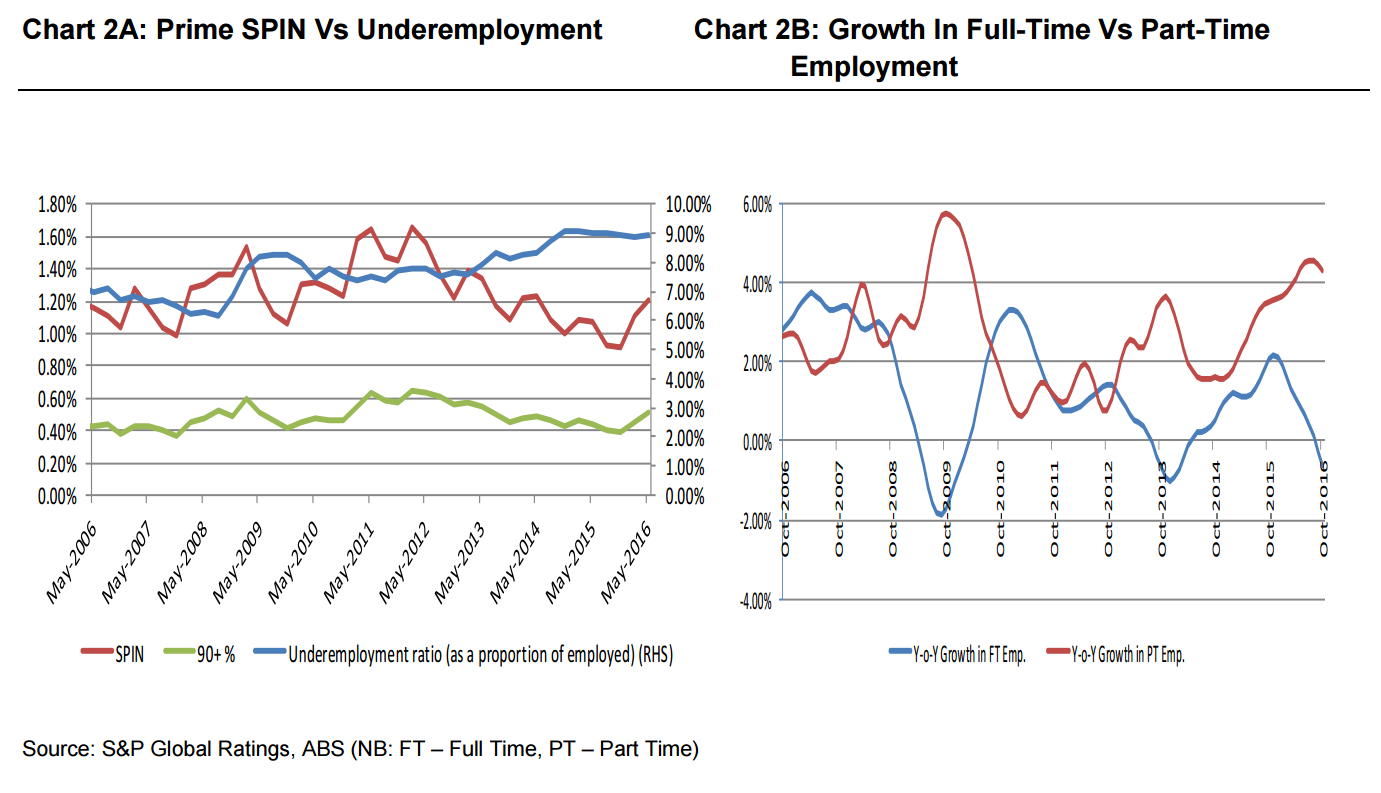

The rate of underemployment started to rise in mid-2014 (chart 2A and chart 2B). Part-time employment has continued to increase since late 2014, while full-time employment growth has been in sharp decline since around November 2015. Interestingly, prime arrears commenced their upward climb in November 2015 and continued to head north until May, when they started to decline as part of the normal cyclical pattern, albeit a bit later in the year then we would normally expect. This trend could be influencing arrears performance if more borrowers have to shift from full-time to part-time employment, given the falling growth in full-time work. The Reserve Bank of Australia (RBA) has attributed the weakness in full-time employment nationwide during the past few years to the subdued demand for labor in the mining states. The arrears performance in the nation’s states and territories provides further evidence of the divergence in economic prospects between the mining and nonmining states as well as metropolitan versus regional areas of Australia.

State Of Play

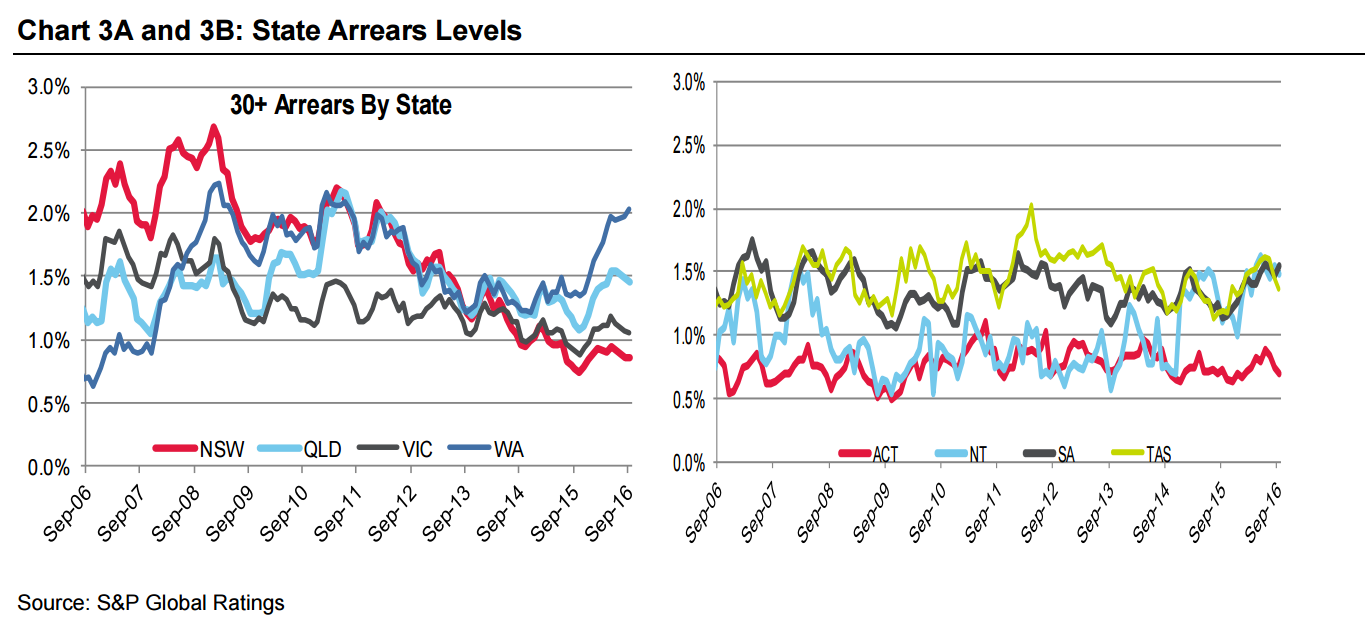

• New South Wales (NSW) arrears were up year on year in Q3, but were the second lowest in the country, behind the ACT. NSW’s strong arrears performance reflects its generally good economic health, evidenced by RMBS Performance Watch | Australia Part 1 – Market Overview As of Sept. 30, 2016 S&P GLOBAL RATINGS 1-5 its relatively low unemployment rate of 4.89%, among the lowest in the country, as well as its strong retail spending and solid population growth. As NSW’s property prices have increased to the nation’s highest levels, mortgage arrears have fallen more rapidly than in other states. Nonmining business investment has grown in NSW during the past three years in response to stronger business conditions in the state. This has created better job prospects and underpinned stronger arrears performance.

• Victoria’s arrears declined in Q3, but are up year on year. However, at 1.05% they are the third lowest in the country. We expect them to remain relatively stable at this level. Like NSW, Victoria has experienced strong population and property price growth and good retail spending. According to recent research from the RBA, Victoria is now the beneficiary of net inward migration from each of the other states. This has helped underpin strong demand for housing and, by extension, housing construction employment, which contributes around 8% to total employment in the state.

• Queensland’s arrears were 1.45% in Q3, up 29% year on year. Arrears and unemployment levels in Queensland are at the higher end of the spectrum. With the most decentralized population and more than 50% of the RMBS exposure to this state outside of Brisbane, higher arrears reflect the greater exposure to regional areas, many of which are facing high unemployment levels and subdued economic growth. As outlined recently by the RBA, the slowdown in mining investment has had a noticeable knock-on effect on nonmining industries in Queensland and Western Australia. The buoyant effects of strong growth in population and household expenditure have been unwound in concert with conditions in the mining industry. Arrears performance in nonmetropolitan areas, outside of Brisbane, shows the impact of these broader economic trends.

• Western Australia (WA) in Q3 again recorded the nation’s highest arrears, up 47% from the same time last year. This was the largest year-on-year increase in arrears. High unemployment and lower wage growth are more pronounced in WA as the economy continues to transition away from jobs in the higher-paying mining sector to lower-paying jobs elsewhere. More subdued employment conditions in WA are also feeding through to property market conditions, with the prices of apartments and detached dwellings in Perth down about 8% from their peaks, according to the RBA. The RBA has said there are a lot of dwellings being completed in Perth relative to the needs of the slower-growing populace. This suggests that dwelling construction and construction employment, which currently contributes around 9.5% to total employment in the state, are likely to remain subdued for some time. Based on these trends, we believe arrears performance in WA is unlikely to improve anytime soon.

• South Australia (SA)’s unemployment rate is the second highest in the country, and this accounts for the state’s higher arrears levels. New manufacturing projects in the ship-building industry are due to come online in coming years, and we expect these to improve employment conditions in SA. However, we do not expect this to filter through to arrears performance anytime soon, given the general decline in manufacturing jobs nationwide and SA’s relatively high exposure to this sector (manufacturing accounts for around 9.5% of employment in this state).

• Tasmania’s arrears are up 14.8% year on year, but its unemployment rate was 6.35% as of Sept. 30, 2016, down from a high of 7.26% in August. Tasmania had the nation’s highest level of arrears until about September 2014, when WA took over the top spot. Tasmania has seen an improvement in its economic condition, as evidenced by its improving unemployment rate and property prices.

• Northern Territory (NT)’s arrears in Q3 were 1.48%, down from 1.53% in Q2 2016. The NT has one of the lowest unemployment rates in the country, which probably reflects the ongoing construction work associated with large-scale gas projects. Given the small exposure in RMBS portfolios to the NT, arrears trends are more volatile in percentage terms.

• Australian Capital Territory (ACT) arrears declined 4.5% year on year to 0.70% in Q3, the lowest in the country. With the public service as a key employer in the nation’s capital, local employment conditions are likely to be more stable than other states and territories, particularly those with a higher exposure to the resources sector. Arrears in the ACT have been below 1% since July 2012, and we expect them to remain below the prime SPIN because the workforce has greater mobility and job security than industries such as manufacturing and mining.

That WA arrears are still only at 2% is incredible. That fact alone tells you that this bust has far yet to run and arrears will push much higher yet.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.